Abstract

Artificial intelligence is revolutionising the financial world through robo-advisors promising to democratise investment, reduce costs, secure investments, improve portfolio management, widen credit access and correct behavioural biases. These benefits are accompanied by critical concerns, including irrational investor behaviour, overreliance on algorithmic systems, data and input bias, conflicts of interests and uneven adoption across demographics. Regulatory analysis contrasts EU and US frameworks, discussing MiFID and GDPR oversight, while addressing demands for “robolaws”. Looking forward, the research explores potential directions for the industry, like strengthened data protection standards and hybrid robo-human advisory models. Overall, the paper concludes that while RAs offer substantial promise for the future of financial inclusion and digital wealth management, their long-term success depends on responsible governance, algorithmic accountability and user trust.

1. Introduction

The term “artificial intelligence” (AI) was formally introduced in 1955, when researchers first hypothesised that a machine could be made to learn if a precise description of the mechanisms underlying learning and intelligence could be encoded within it (McCarthy et al., 2006). Companies developing AI technologies are motivated by competitive desires: to establish themselves as industry leaders, gain market dominance and secure control. This strong incentive to innovate outpaces ethical deliberation and regulatory development, resulting in deployment of AI systems that lack sufficient ethical protections.

Robo-advisors (RAs) are referred to as “robo-consultants”, characterised by algorithmic frameworks designed to align investment portfolios with an individual’s financial goals and risk tolerance (Njegovanovie, 2018). Unlike active investing, involving decisions centralised on timing and selection of specific financial instruments, RAs apply passive investing which allocates funds based on pre-established investment decisions and long-term market trends. This study argues that while robo-advisors offer significant rewards in democratising finance, their long-term sustainability is threatened by unaddressed risks from data bias and regulatory gaps, suggesting a hybrid human-AI model is the most viable future.

Data from Statista (2022) reports robo-advisors globally seize approximately US$2.76 trillion Assets Under Management (AUM), with projections of US$4.5 trillion within the next four years. As of 2023, 393 million individuals reported using RA services, indicating far-reaching consumer trust and market penetration. Yet, their rise presents a dilemma: in removing human flaws, are we introducing obscure, unaccountable systems in their place? This paper will explore the following research question: What rewards, risks and regulatory challenges shape the future of AI-driven robo-advice?

The following sections will analyse the rewards, risks and regulatory landscape of robo-advisory platforms, concluding with an assessment of their future trajectory.

2. Literature Review

The 2008 Global Financial Crisis exposed monumental vulnerabilities within traditional banking institutions and human advisory practices. The widespread failures, mismanagement and conflict of interests with conventional financial advisors eroded investor confidence (Sironi, 2016). Consequently, investors shifted toward passive asset management strategies and more transparent, cost-effective solutions (Severino & Thierry, 2022). This catalysed the rise of robo-advisors (RAs), which offered automated, objective and affordable financial advice, appealing to younger, technology-adept investors.

Computational Theory of Mind (CTM) piloted the development of symbolic artificial intelligence, which dominated early AI research (1950s-1980s) by equating intelligence with rule-based inference; for example, expert systems encoding “if-them” rules and semantic networks. Yet, symbolic AI failed to scale to human-like intelligence due to its rigidity and inability to process sensory inputs and navigate complexities of real-world environments, instead reducing intelligence to fixed logical structures.

Limitations of symbolic AI gave rise to connectionist AI (machine learning), enabling systems to improve performance autonomously through experience rather than explicit programming (Bhatia et al., 2021). However, Kaliszyk et al. (2017) contend machine learning (ML) inherits contextual biases and unverifiable assumptions, resulting in skewed interpretations of reality and difficulty in justifying outcomes from theoretical or ethical standpoints. Nevertheless, ML algorithms outperform conventional techniques in detecting nonlinear trends, identifying outliers before price movements and assimilating diverse perspectives through historical market data and current social sentiment from platforms like Twitter or news feeds.

3. Methodology

We conducted a desk-based comparative review of secondary sources (regulator reports, peer-reviewed studies, reputable industry white papers and official disclosures) published between 2019 and 2025. We compiled reported figures (e.g.g, fees, AUM, complaint rates, behaviour outcomes) and triangulated them where possible. We did not run new surveys, interviews or econometric tests.

4. Robo-Advisory Rewards

The advent ofm robo-advisors is and has been revolutionising the financial industry in a plethora of ways. This section explains how; specifically, through widening access to all individuals, reducing startup capital, improving and offering advanced portfolio management, avoiding emotional mistakes, ensuring transparency and even opening credit to individuals with little to no history.

4.1. Democratising Financial Access

Robo-advisors are democratising finance by removing barriers that have historically limited investing to the wealthy. This inclusivity extends beyond simple investing to bridge financial gaps for groups often excluded from traditional systems, such as gig workers and immigrants with limited credit history. Instead of relying solely on formal credit reports, these AI-powered platforms can analyse alternative data like mobile payment histories and utility payments to build fairer, more dynamic financial profiles. A field study by the SME Finance Working Group showed that using this kind of data increased credit approvals for unbanked individuals by 20–30% without raising default risk, and the World Bank estimates that a 10% increase in credit access among underserved groups could lead to a 0.5% increase in GDP and lower poverty rates.

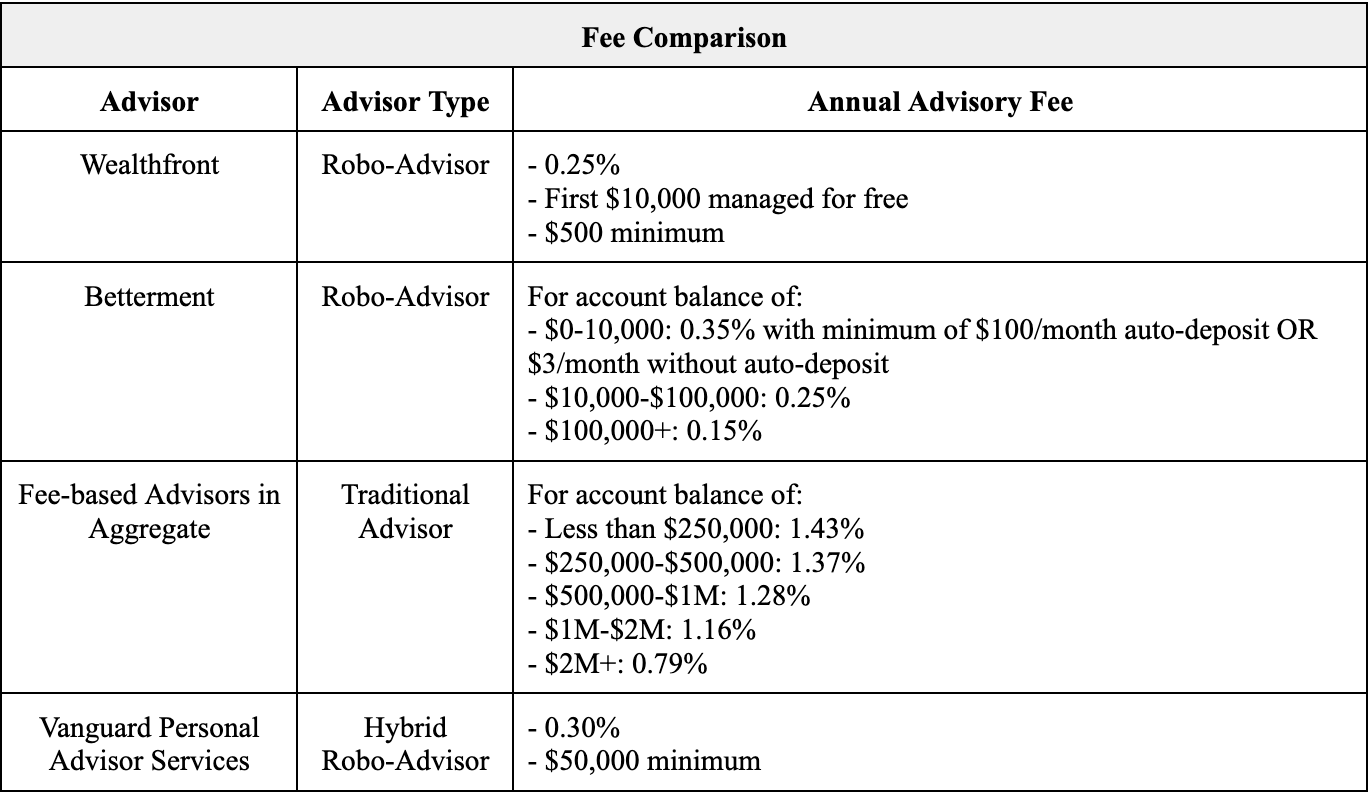

The low entry requirements of robo-advisors, some requiring no minimum at all, transforms the mindset of “I’ll invest when I have more money” into a habit that starts now. For example, Betterment charges just 0.25% annually, meaning a $100,000 portfolio would cost only $250 per year, compared to $1,430 with a human advisor charging 1.43%. Lower costs reduce hesitation, encouraging more people to start saving, investing and learning early. Over time, this builds stronger financial habits and more resilient households. This expansion of credit access is particularly impactful in developing economies, where many find themselves locked out of the financial system not because of their mismanagement of money, but because no data about them is recorded. Traditional banks rely heavily on formal credit reports or income proofs, which are requirements that many cannot meet.

By lowering rates and extending credit access, robo-advisory systems support not only individual borrowers but also economic inclusion. A young adult in the United Kingdom or the Middle East with no credit card but consistent mobile payment behaviour can now be evaluated with a much fairer, dynamic lens. This means more people can start small businesses, invest in education, cover emergencies or purchase any good or service the person desires.

In this way, robo-advisors are not just investment platforms, they are tools for increasing financial participation, reducing inequality and giving more people a chance to secure their financial future.

Source: Walter Lam, 2016.

RAs require only a small initial investment, lowering the entry barrier for individuals with limited capital. This high level of accessibility contributes to increased financial literacy as more individuals are able to engage with investment platforms and gain practical experience in managing their finances. Financial advisors usually charge 1% to 2% of the assets they manage, additionally accounting for a one-time service fee and commission. On the contrary, most robo-advisors charge 0.2% to 0.7% of the assets they manage, leaving funds to be used for other investments or savings. For example, if a financial advisor takes 2% from an investor with a $40,000 portfolio, the investor would be charged $800 per year, excluding commission and service fees. However, with a robo-advisor that charges 0.7%, the individual would only pay $280 per year. After 6 years, robo-advisors could save an investor up to $3120. Consequently, the remaining money could be used for other investments or other wants and needs.

This investment requirement allows individuals with limited savings to begin as soon as possible and with a low risk. When some robo-advisor platforms lowered their minimum account start-up to $500 about 3-5 years ago, they saw a 107% increase of individuals participating, therefore increasing investments and consumption of individuals, which then contributes to the overall GDP of a country and its economic activity, signalling economic growth. Tertilt and Scholz (2017) observe that the entry of robo-advisors has forced traditional investment firms to innovate and reconsider their fee structures, ultimately making the financial industry more competitive and cost-efficient. This establishes robo-advisors’ integration as an option for individuals and countries, both regarding money and management efficiency. When more people gain access to investment tools, their financial status improves, they participate in financial activities more frequently and, consequently, the economy prospers even further: unemployment rates decrease, poverty dwindles, advancements in healthcare and technological innovation emerge, and living standards improve. This accessibility is critical in places with financial inequality or limited infrastructure.

Moreover, robo-advisory platforms like Sarwa allow individuals to start with $5. Operating without the need for physical branches or large advisory teams, RAs can expand rapidly while maintaining low overhead costs. This has enabled platforms such as Nutmeg and Wealthsimple to expand their services across multiple countries with ease. Their use of AI-driven systems allows them not only to scale efficiently but also customise their offerings in accordance with cultural preferences. Thus, ensuring relevance of robo-advisors across diverse financial markets while continuing to offer low-cost solutions.

4.2. Efficient Portfolio Management

Robo-advisors have the ability to manage portfolios efficiently: they function as socio-technical systems that translate financial theories into algorithm investment advice. They are built upon Modern Portfolio Theory (MPT) (Markowitz, 1952), which aims to maximise return for a given level of risk by diversifying investments across asset classes. Financial advisors may be susceptible to bias or emotions. However, robo-advisors are not, as they are machines programmed to follow an algorithm to manage portfolios effectively. Robo-advisors work all day, at all hours, monitoring the market while analysing it. If a change in the market trend happens, then robo-advisors are the first to know, and all this is done to align with the interests of investors.

As robo-advisors operate constantly without breaks and can interpret massive datasets quickly, they can automatically adjust portfolios in real time, reacting faster than humans (Kyle, 2022). There are two techniques or models that are used for managing investments in robo-advisors. MPT provides the mathematical basis for creating a diversified portfolio by spreading investments across different assets to reduce risk. However, MPT assumes that asset relationships, such as how two investments move together, stay constant over time. This can be unrealistic during unstable markets. The Black-Litterman model builds on MPT by allowing users to include their own views or expectations about future asset performance. It adjusts the standard model by combining those views with market data, making portfolio construction more flexible and better suited to real-world uncertainty (Lam & Swensen, 2016).

The Black-Litterman model allows for the incorporation of market views and confidence levels in expected returns, while factor analysis is used to narrow down relationships between the performances of different asset classes, improving the stability of portfolio arrangement. Additionally, RAs use tax-loss harvesting strategies: selling underperforming assets to realise capital losses, which offset taxable gains and consequently reduce investors’ tax liabilities. In simpler terms, when certain values of investments decline, they will immediately sell them and buy similar investments. The losses are then used to compensate for any profits from other investments. For example, Betterment’s implementation of automated tax-loss harvesting has been shown to improve net returns, especially for cost-sensitive investors. By integrating such features, RAs transform sophisticated investment methods into accessible tools for everyday investors, removing traditional barriers of wealth, knowledge and advisor access.

Passive investing has appeared as a dominant strategy in modern portfolio management, persuaded by Burton Malkiel’s A Random Walk Down Wall Street and Charles Ellis’ Winning the Loser’s Game. Malkiel contends that because markets efficiently incorporate available information, investors face significant challenges in outperforming benchmarks. His Random Walk Hypothesis affirms future stock prices are independent of past movements, undermining the validity of market-timing and speculative trading strategies. RAs engage passive investing, mainly through index funds aiming to match rather than beat the market. Charles Ellis argues that as markets filled with skilled professionals, beating the index became harder and costs ate away any small gains. He concludes that passive indexing is now the real “winner’s game” that ordinary investors can actually win.

In addition, robo-advisors also promote overall tax-efficiency by encouraging long-term investment strategies. These strategies avoid frequent buying and selling, which can trigger short-term capital gains – profits that are usually taxed at higher rates than long-term gains. By holding investments for longer periods, robo-advisors help users minimise these tax costs and retain more of their earnings over time (Hayes, 2020). Moreover, robo-advisors automatically adjust portfolios with the goal of diversifying investments based on risk, even in unstable market conditions. They spread investments across different assets such as stocks, bonds, commodities and real estate, and avoid making sudden changes during market drops. This helps investors stay calm and stick to their long-term plans, even when the market is unstable.

Sharpe ratios measure an investment’s performance by taking risk into account, providing signals and insights into the expected returns. Robo-portfolios have a Sharpe ratio of 0.75 compared to 0.45 for self-managed portfolios. This means that robo-advisors are more secure when managing risky investments and also have higher expected returns and lower volatility. Moreover, robo-advisors help correct psychological investment mistakes. For example, they reduce the disposition effect, where users sell winning assets too early and hold onto losing ones too long, through rule-based decision-making (Back et al., 2023). They also discourage trend-chasing and rank bias, which are common behaviours where investors focus only on high-performing or low-performing assets rather than maintaining balance (Loos et al., 2020; Merkle, 2020). According to Dual Process Theory, these platforms promote System 2 thinking: low, deliberate and rational over impulsive emotional reactions (Jung & Weinhardt, 2018).

4.3. Mitigating Behavioural Biases

Despite their technical advantage, RAs usually face scepticism due to what Dietvorst et al. (2015) term “algorithmic aversion”, a bias in human reasoning that leads people to distrust machine-generated decisions. Lisauskiene and Darskuviene (2021) establish a typology of behavioural biases in the investment process: disposition effect, the tendency to sell profitable assets too soon while holding onto underperforming ones; trend-chasing, the mistaken belief that past performance reliability predicts future returns; and the rank effect, a tendency to overly focus on either extremely high-performing or low-performing assets.

Dual Process Theory differentiates between two cognitive systems: System 1 operates automatically, rapidly and is controlled by emotion, while System 2 is slower, more analytical and reflective. In high-stress financial environments, System 1 dominates, leading to impulsive and irrational behaviour. This model explains why individuals frequently make poor financial decisions under emotional pressure, such as reacting to short-term market noise rather than adhering to long-term strategy. RAs use behavioural “nudging” to guide users toward more stable and less emotional decisions, aligning with System 2 thinking. This technology reduces mental pressure and allows rational investment by simplifying complex financial tasks.

Prospect Theory, introduced by Tversky and Kahneman (1992), is a foundational concept in behavioural finance that redefines how individuals are understood to make decisions under conditions of risk and uncertainty. Contrary to traditional economic models that assume rational agents, Prospect Theory alleges individuals overestimate small risks and underestimates large ones. A key idea in this theory is the concept of loss aversion where investors experience greater psychological discomfort from financial losses than satisfaction from equivalent gains. This imbalance results in an aversion to high-risk, high-reward investments, with individuals preferring lower-risk, lower-return assets even when those choices don’t provide the maximum possible returns. Robo-advisors are specifically designed to counteract these cognitive biases through automated, rule-based strategies.

Source: Andy Rachleff and Roberto Medri (September 18, 2014) ‘Passive Investors Need Less Hand Holding’, Wealthfront Blog.

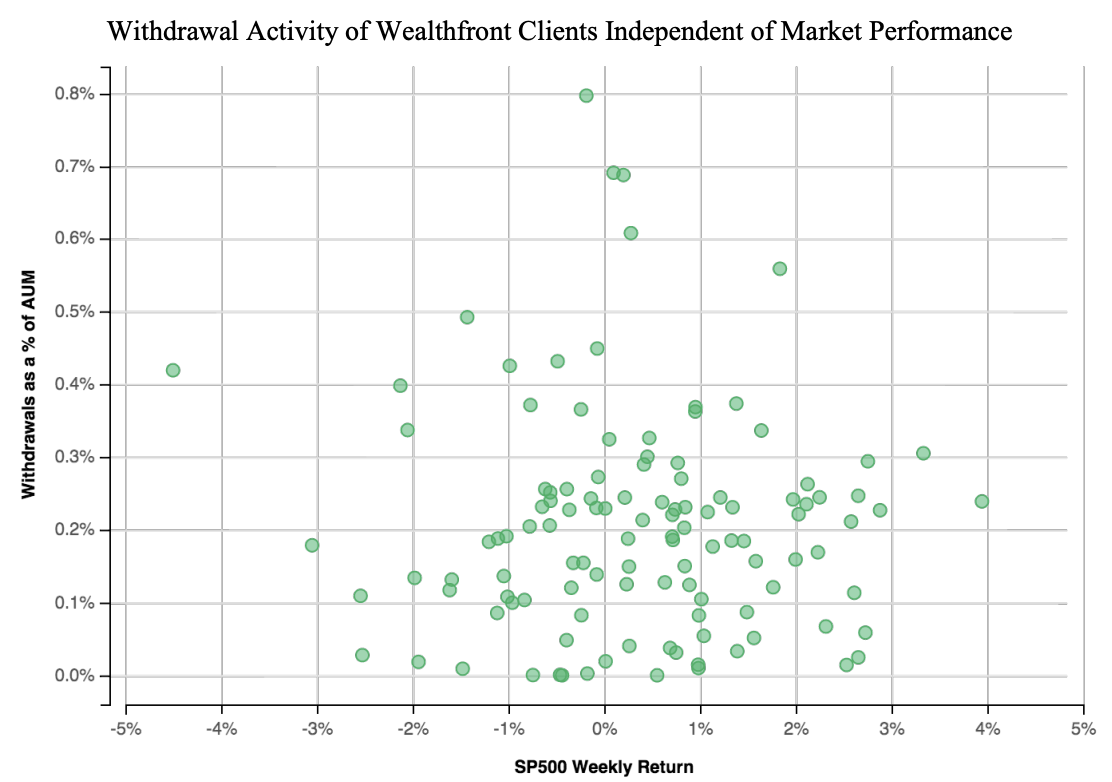

During periods of market volatility, investors often try to “time the market” by making quick withdrawals or changing their portfolios based on short-term price drops. However, data from Wealthfront shows that robo-advisors help reduce this behaviour by encouraging steady, long-term investing. Wealthfront reports R² = 0.002 (p = 0.662) between client withdrawals and weekly S&P 500 returns – consistent with limited panic-selling.

Even when the market saw sharp declines, like -3.0% on January 20, 2014, and -2.5% on August 12, 2013, clients didn’t significantly change their behaviour. This supports the idea that robo-advisors help prevent emotional, panic-driven decisions by keeping users focused on long-term goals, even during downturns.

Source: Andy Rachleff and Roberto Medri (September 18, 2014) ‘Passive Investors Need Less Hand Holding’, Wealthfront Blog.

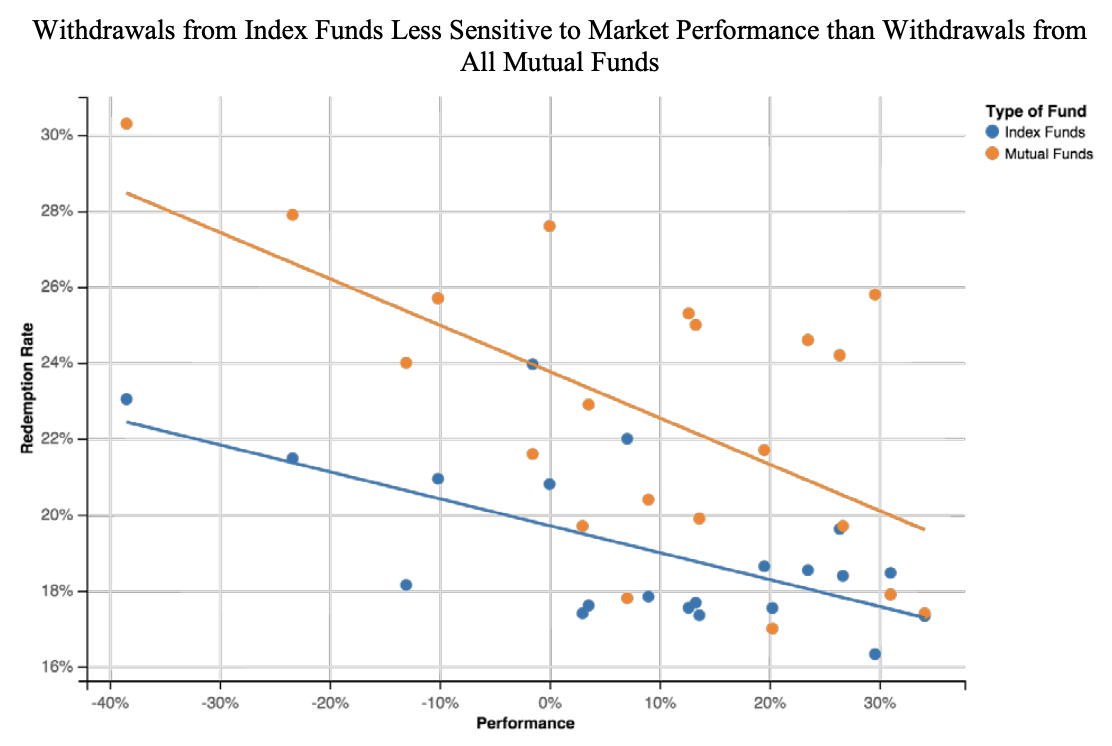

A primary critique of RAs is that clients may engage in panic-driven behaviour, such as withdrawing funds during market downturns due to a lack of human reassurance. However, Rachleff and Medri’s 20 year study (1993-2013) refutes this assumption by showing passive investors (index funds) are actually less reactive during periods of market volatility compared to active investors (mutual funds). Specifically, a 1% decline in S&P 500 triggers a 0.12% increase in redemptions from all mutual funds, but only a 0.07% increase from index funds. This behavioural difference is statistically significant at the 99% confidence level. Given that index funds constitute approximately 20% of total mutual fund assets, and thus included in the aggregated mutual fund data, the actual disparity between purely active and passive investors may be even greater than reported. Hence, evidence declares RA users, who are passive investors by design, are less susceptible to panic-selling during downturns, falsifying the narrative that automated financial services lack the psychological support to prevent poor investor decisions.

4.4. Blockchain and Convenience

Crypto-focused robo tools sometimes integrate wallets or smart contracts to automate rebalancing and settlement. Mainstream robo-advisers for equities and bonds remain off-chain, using conventional brokers/custodians while focusing AI on portfolio construction and client communication.

5. Robo-Advisory Risks

Although RAs are celebrated for their accessibility, efficiency and democratisation, the integrity of RAs is eroded by their inability to account for irrational consumer behaviour, data biases, opaque algorithmic decision-making, conflicts of interest and unequal adoption across social groups, inhibiting RAs long-term viability in the financial ecosystem.

5.1. Irrational Investor Behaviour

Investor behaviour is not solely governed by objective data and rational calculation, but manipulated by subjective perceptions, emotions and psychological tendencies. Capital markets are founded upon the perception of reality rather than reality itself: a bandwagon effect where individuals follow market trends without verification and self-cancelling patterns where market trends perish once ordinarily adopted. Lisauskiene and Darskuviene (2021) insist real-world financial decisions are moulded by cognitive biases, emotional reactions and psychological heuristics, which contradict economic models that assume agents behave rationally and efficiently. While RAs are highly effective at processing structured data and executing predefined strategies, they cannot narrate irrational or emotional investor actions. Poor investor behaviour, such as panic selling, impulsive withdrawals or inconsistent adherence to long-term plans, undermines the logic of RA algorithms, compromising their validity.

Moreover, the predictive power of AI is inherently constrained by its reliance on historical data. RAs are not purely deterministic; they attempt to anticipate future events yet cannot fully accommodate unexpected market shocks or black swan events. Dzhusov and Apalkov (2017) contend RAs require regular recalibration, typically every six months, to remain responsive to evolving market conditions. Without this ongoing adjustment, platforms become obsolete, depreciating performance when markets symbolise unforeseen geopolitical events, regulatory changes or investor panic-epidemic.

5.2. Overreliance on AI

Magnuson (2020) proclaims the primary limitation of AI does not stem from the technology itself, but rather from misplaced confidence users place in its outputs. Blind trust in AI forecasts inhibits users from actively questioning or validating recommendations. Lisauskiene and Darskuviene (2021) caution that deferring excessively to algorithmic authority alienates investors from their assets, hindering financial literacy. Furthermore, RAs appeal to less confident investors who are drawn to the convenience of automated financial guidance. While this inclusivity is a strength, users are unable to cultivate the skills to manage their finances independently. Tertilit and Scholz (2017) stress the proliferation of RAs could cannibalise traditional advisory services, disrupting the harmony between human judgement and machine automation in the financial ecosystem.

5.3. Data Bias

RAs, marketed as objective and rational tools are dependent on human-coded AI algorithms, which inevitably carry biases. Rules determining how investment decisions are made also dictate the extent to which biases are either mitigated or perpetuated. Ji (2017) criticises RAs for relying heavily on user-provided questionnaires to assess risk tolerance, investment goals and time horizons – variables forming the basis of asset allocation decisions. When these inputs are inaccurate, incomplete or self-contradictory, resulting strategies are misaligned, exposing users to risks or suboptimal performance. This defect is particularly dangerous for novice investors who may not recognise consequences of their own input errors or limitations of the algorithm interpreting them. Breener and Meyll (2020) warn social biases, such as discriminatory credit scoring systems or socioeconomic stereotypes, can be inadvertently absorbed into ML models, raising concerns about systemic inequality in digital finance. Furthermore, because RAs aim to build trust through personalisation, they may validate consumers’ preconceptions and overconfidence, endorsing flawed financial behaviours under the guise of algorithmic authority.

The commercial profitability impetus incentivises RAs to utilise unauthorised sources, such as media activity, banking records or legal documents, to generate comprehensive financial profiles. Such data harvesting without explicit user consent instigates significant ethical and privacy concerns. Ultimately, Hayes (2020) asserts the purpose of financial technology is to facilitate rational decision-making, yet the algorithm underpinning these systems remains deeply human in their constructions, projecting the assumptions, limitations and biases of their designers.

5.4. Conflict of Interest

Digital platforms are advertised as objective, client-centric alternatives to traditional financial advisors; however, they are not always motivated to act solely in the best interest of users. Instead, many RAs are rewarded for promoting certain financial products or services that maximise revenue, rather than optimising financial outcomes for clients. Abraham et al. (2019) highlight RAs prioritising recommendations from specific brokers offering higher commissions, even when this option is not suitable for investors. Similarly, Gurrea-Martinez and Wan (2021) bring attention to the manipulative cycle where RAs advise users to initially hold cash, only to later recommend reinvesting through the same platform. This strategy increases likelihood of user dependency and elevates the platform’s revenue without advancing the client’s financial goals. Lack of algorithm transparency further entrenches the power imbalance between platform developers and consumers. Users are negligent to underlying logic or data sources driving investment suggestions, preventing them from distinguishing between genuine neutral advice and fabrication for firm interests. This asymmetry of knowledge, rooted in technical complexity and proprietary data ownership, heightens exploitation and diminishes accountability.

5.5. Uneven Usage

Despite global propagation of robo-advisory platforms, usage remains disproportionate among varying demographic and socioeconomic groups. Isaia and Oggero (2022) conducted a survey of 1300 young adults in Italy, revealing individuals with postgraduate education and high levels of financial literacy are significantly more likely to adopt RAs. Satisfaction levels are higher among users under the age of 44, implying younger investors tend to perceive greater value in digital financial services. Additionally, the study determines a gender gap: women are consistently less likely to use RAs, regardless of age, education or risk appetite.

Ross and Utkus (2024) note users who initially had low equity exposure, paid high advisory fees or held poorly diversified portfolios gain the most from RA services. These individuals are predisposed to seeking financial automation and favourably positioned to reap the benefits of RAs’ cost efficiencies. Similarly, Shen et al. (2024) found middle-income users during periods of economic stress like the COVID-19 crisis, tend to prosper more from RAs, explained by the positive correlation between wealth and financial literacy.

In India, for instance, RAs penetration is depressed. Nain and Rajan (2023) attribute this to several barriers: cultural preference for human interaction, low financial literacy, enigmatic government guidelines and incompetent risk assessment models. These impediments are both institutional and behavioural obstacles that hinder RA adoption in emerging markets. Baulkaran and Jain (2023) provide additional demographic insights from a comparative study of 185,950 RA users and 93,484 non-users. Their findings indicate RA users are likely to be young, male, married and managing humble investment portfolios. In contrast, students and retirees are significantly underrepresented among RA adopters, suggesting life stages are a defining factor.

6. Robo-Advisory Regulations

Veale and Borgesius (2021) observe a substantial absence of standardised conceptual models to evaluate AI ethics, inhibiting developers and regulators to align robo-advisors with normative ethical expectations. Stahl (2021) contend that internationally recognised ethical frameworks, such as the United Nations Sustainable Development Goals (SDGs) and the Universal Declaration of Human Rights (UDHR), should become primary references as these documents represent global consensus on core human values. Floridi (2019) introduces “infosphere”, a digital environment that, like the biosphere, must be governed with principles of sustainability. He proposes “normative cascade”, where values and norms are transmitted through legal statutes to public policy to business practices and finally to consumer behaviour. Within this framework, ethical governance is divided into “hard ethics” – enforceable legislations grounded in universal standards like the UDHR – and “soft ethics” – promoting ethical conduct beyond legal obligations, particularly in contested regions. Maume (2021) notes RAs are currently regulated under financial services law rather than AI-specific legislation. Classified as “low-risk” under the European Union’s AI Act, RAs do not attract the regulatory scrutiny applied to high-risk applications. As a result, there is no cohesive framework that integrates financial compliance with ethical AI principles, further inciting divergent practices across jurisdictions.

6.1. Markets in Financial Instruments Directive

The Markets in Financial Instruments Directive (MiFID), established across the European Union in 2017, is a cornerstone of EU financial regulation directing investor protection and market transparency. Rather than prescribing a rigid legal framework, MiFID integrates within existing national legal systems, making compliance achievable through regulatory alignment instead of direct legislative enforcement (Maume, 2018). RAs’ compliance with MiFID necessitates adhering to transparent data disclosure, execution of decorum assessments, accurate client categorisation, best administration of trades, conflict of interest management and robust record-keeping practices (Directive 2015/65/EU).

However, several scholars have questioned the adequacy of MiFID in addressing the unique challenges posed by RAs. Sanz Bayon and Garvia (2018) call for the creation of more technically tailored legal frameworks, referred to as “robolaws”, to reflect the operational complexities of algorithmic advisory systems. A significant flaw is MiFID’s conceptual distinction between “advising” and “asset management”. RAs do not fit neatly into either category; they are not legally recognised as traditional financial advisors, nor are they entitled to manage assets on behalf of third parties under current regulatory definitions. Additionally, MiFID stipulates that a “personal recommendation” must be sufficiently tailored and persuasive to prompt an investment decision, but it does not provide clear criteria for what constitutes “persuasive” advice. This vagueness announces regulatory uncertainty and weakens reliable investor protection.

6.2. Regulation in the European Union and United States

The regulatory landscape for RAs in the European Union and United States reflects contrasting approaches rooted in differing legal traditions, cultural values and institutional priorities. In the EU, RAs are primarily regulated under MiFID and the General Data Protection Regulation (GDPR). GDPR introduces strong ethical requirements regarding data transparency, user consent and algorithmic accountability, coinciding with the EU’s broader commitment to rights-based governance.

On an international level, the International Organisation of Securities Commissions (IOSCO) observed there is no immediate need for new regulatory frameworks beyond existing standards. However, Back and Dellaert (2018) contend RAs should be held to the same standards as human financial advisors, especially in terms of fiduciary responsibility, transparency and accountability. Yet, they acknowledge the limitations of using human advisors as a benchmark for fairness, reliability or consistency, given their own susceptibility to cognitive biases and conflicts of interest.

In the United States, the regulatory ecosystem is more sector-specific, mainly conducted by the Securities and Exchange Commission (SEC), Financial Industry Regulatory Authority (FINRA) and Investment Advisers Act of 1940. The SEC mandates that firms employing RAs must meet fiduciary standards, obtain proper licencing and disclose algorithms used to generate investment recommendations. Despite these measures or ways, FINRA criticised RAs for their limited capacity to fulfil responsibilities in the same manner as human advisors. These concerns involve RAs’ inability to provide comprehensive financial advice or account for complex, non-quantifiable client needs. Moreover, strict enforcement is made problematic by powerful financial firms and accelerated evolution of fintech models. Additionally, enforcement faces challenges due to rapid fintech development and the policy influence of large financial firms.

As a result, differences between EU and US regulatory models shadow broader cultural and governmental attitudes. The EU uses an ethics-driven and consistent approach centred on human rights, privacy and algorithmic accountability. In contrast, the US prioritises investor protection and innovation, showing a more market-oriented philosophy.

6.3. Lack of Transparency

Many RA firms decline to publish their ML algorithms to regulators, independent auditors or consumers. The most common justification for this opacity is the protection of intellectual property, as the proprietary nature of these algorithms are considered sources of competitive advantage. However, this protective stance threatens accountability, fairness and user protection. Even if RA firms disclosed their ML algorithms, the architectures are intrinsically arcane, termed as “black boxes”; their logic difficult to explain even by developers themselves. This exacerbates the regulatory lag – a discrepancy between pace of technological innovation and speed at which regulatory frameworks adapt. Consequently, existing legal standards are underqualified to supervise modern ML financial advisory systems.

A radical proposal to address the accountability gap has emerged in Australia, where Lee et al. (2008) have suggested granting legal personhood to robo-advisors. RAs are held legally accountable for delivering biased, misleading or unsuitable investment advice, in the same way a corporate entity is liable for financial misconduct. However, legal personhood harbours excessive regulatory burdens, convoluted litigation processes and discourages innovation by increasing firms’ exposure to liability and compliance costs.

7. The Future of Robo-Advisors

As robo-advisory platforms continue to scale globally, their future is not determined by advances in AI but by the ethical, legal and human dimensions of financial automation. The General Data Protection Regulation sets a fundamental precedent for consent, transparency and data protection. Equally pivotal are hybrid advisory models that unite algorithmic efficiency with human judgement.

7.1. GDPR for Data and Privacy Protection

The proliferation of AI financial services exposes vast volumes of sensitive investor data, heightening risk of breaches, cyberattacks and unauthorised processing. Looking ahead, the challenge will lie in establishing interoperable, adaptive legislative frameworks that anticipate emerging threats and uphold digital rights.

The General Data Protection Regulation (GDPR) becomes a leading model for the future regulation of RAs. Under Recital 51, GDPR mandates that organisations establish formal procedures for rectifying data breaches, including end-to-end encryption and two-factor authentication for employees (Wealthfront, 2019). Such technical safeguards must be continuously updated to rival the sophistication of cyber threats.

Crucially, GDPR’s requirement for explicit consent, defined as “freely given, specific, informed and unambiguous”, prior to automated decision-making will become pivotal to ethical AI deployment. Future designs must adhere to Article 22(2) of GDPR by either securing user consent or establishing a legal basis through contract. Comparable standards exist in other jurisdictions, such as China’s Personal Information Protection Law (PIPL), signalling a global convergence, though notable gaps in legislative clarity remain, particularly in emerging markets such as Nigeria (Harris et al., n.d.).

Transparency is also defining the future regulatory landscape. GDPR mandates clear communication of data usage, rights and breaches to users and authorities. In contrast, Hong Kong merely “recommends” such practices (Liu, 2023). As RAs become custodians of financial life planning, mandatory breach notification and transparent governance protocols are pivotal for global acceptance and long-term viability of RA services. Hence, GDPR is a blueprint for achieving privacy, transparency and user autonomy into platform design, but global harmonisation, continuous oversight and adaptive legal standards is paramount.

7.2. Hybrid Robo-Advisory Models

Rather than replacing human advisors, RAs should be positioned as complementary tools that enhance, rather than substitute, traditional financial advisory services. Waliszewski and Zieba-Szlarska (2020) argue that RAs are best understood as augmentative systems, capable of automating routine tasks while leaving complex, emotionally-nuanced decisions to human professionals. For example, Vanguard’s hybrid advisory system integrates RAs to construct and manage diversified portfolios, while human advisors offer strategic counsel on issues, such as retirement planning, tax optimisation and estate management – domains where personalised judgement remains imperative (Vanguard, n.d.). This dual-channel structure enables financial plans to remain aligned with short- and long-term objectives, blending the precision of algorithms with the emotional reassurance of human advice. Thus, envisioning the future, robo-advisory platforms emulate hybrid systems that synthesise automation and human judgement, promising to deliver scalable, cost-effective services without sacrificing trust nor empathy.

8. Conclusion

Our review has confirmed that robo-advisors effectively lower costs and mitigate some behavioural biases. However, these benefits are countered by significant risks, including algorithmic bias, conflicts of interest and inconsistent global regulation. The central tension identified in this paper suggests that a fully automated approach is insufficient. The most sustainable path forward lies in hybrid models, which combine the efficiency of AI with the nuanced judgement of human advisors, particularly for complex financial planning.

Ultimately, the success of robo-advisors will depend less on technological innovation and more on building trust through algorithmic transparency, robust ethical governance and a commitment to genuine financial inclusion.

Bibliography

Betterment (2025). Betterment: The Smart Money Manager. Betterment. Available online: https://www.betterment.com/.

Columbia Law Review (2024). Are Robots Good Fiduciaries? Regulating Robo-Advisors Under the Investment Advisers Act of 1940. Columbia Law Review. Available online: https://www.columbialawreview.org/content/are-robots-good-fiduciaries-regulating-robo-advisors-under-the-investment-advisers-act-of-1940-2/.

Dietvorst, B.J., Simmons, J.P. & Massey, C. (2015). APA PsycNet. psycnet.apa.org. Available online: https://psycnet.apa.org/record/2014-48748-001.

Dietzmann, C., Jaeggi, T. & Alt, R. (2023). Implications of AI-based robo-advisory for private banking investment advisory. Journal of Electronic Business & Digital Economics, 2(1). doi:https://doi.org/10.1108/jebde-09-2022-0037.

Engler, A. (2023). The EU and U.S. diverge on AI regulation: A transatlantic comparison and steps to alignment. Brookings. Available online: https://www.brookings.edu/articles/the-eu-and-us-diverge-on-ai-regulation-a-transatlantic-comparison-and-steps-to-alignment/.

Euaiact.com. (2016). Key Issue 5: Transparency Obligations. EU AI Act. Available online: https://www.euaiact.com/key-issue/5?.com.

Floridi, L. (2019). Translating Principles into Practices of Digital Ethics: Five Risks of Being Unethical. Philosophy & Technology, 32(2), pp.185–193. doi:https://doi.org/10.1007/s13347-019-00354-x.

GDPR (2013). Art. 22 GDPR – Automated individual decision-making, including profiling. General Data Protection Regulation (GDPR). Available online: https://gdpr-info.eu/art-22-gdpr/.

Gurrea-Martinez, A., Yee, W., Zhiren, S., Xiang, Y. & Xin, K. (2021). The Promises and Perils of Robo-Advisers: Challenges and Regulatory Responses.

Kaliszyk, C., Urban, J. & Vyskocil, J. (2017). Automating Formalization by Statistical and Semantic Parsing of Mathematics. Research Gate. Available online: https://www.researchgate.net/publication/319203018_Automating_Formalization_by_Statistical_and_Semantic_Parsing_of_Mathematics.

Kamarun, N. & Kabethi, L. (2021). Alternative Data for Credit Scoring Special Report Introduction. Available online: https://www.afi-global.org/wp-content/uploads/2025/02/Alternative-Data-for-Credit-Scoring.pdf.

Kern, D.-R. & Dethier, E. (2022). Trust in Robo-Advisor Usage – Implications Concerning Trust in High-Risk Environments. Appropriate Trust in Human-AI Interations (ECSCW Workshop 2022). doi:https://doi.org/10.21428/35500350.62fb0059.

Lassegue, J. (1996). What Kind of Turing Test Did Turing Have in Mind? Research Gate. Available online: https://www.researchgate.net/publication/265007809_What_Kind_of_Turing_Test_Did_Turing_Have_in_Mind.

Lee, N. (2021). Why robo-advisors are striving toward a ‘hybrid model,’ as the industry passes the $460 billion mark. CNBC. Available online: https://www.cnbc.com/2021/04/12/why-robo-advisors-may-never-replace-human-financial-advisors.html.

Lightbourne, J. (2017). Algorithms & Fiduciaries: Existing and Proposed Regulatory Approaches to Artificially Intelligent Financial Planners. Jstor.org. Available at: https://www.jstor.org/stable/26674645.

Lisauskiene, N. & Darskuviene, V. (2021). Linking the Robo-advisors Phenomenon and Behavioural Biases in Investment Management: An Interdisciplinary Literature Review and Research Agenda. Organizations and Markets in Emerging Economies, 12(2), pp.459–477. doi:https://doi.org/10.15388/omee.2021.12.65.

Markowitz, H. (1952). Portfolio Selection. The Journal of Finance, 7(1), pp.77–91. doi:https://doi.org/10.2307/2975974.

Maume, Prof.Dr.P. (2021). Robo-advisors. Available at: https://www.europarl.europa.eu/RegData/etudes/STUD/2021/662928/IPOL_STU(2021)662928_EN.pdf.

McCarthy, J., Minsky, M.L., Rochester, N. & Shannon, C.E. (2006). 2 AI Magazine.

McCulloch, W.S. & Pitts, W. (1943). A logical calculus of the ideas immanent in nervous activity. Bulletin of Mathematical Biology, 52(1-2), pp.99–115. doi:https://doi.org/10.1016/s0092-8240(05)80006-0.

Nasr, T., CFA & FRM (2023). Wealthfront Statistics (2023): AUM, Users, Revenue, & More. Available online: https://investingintheweb.com/brokers/wealthfront-statistics/.

NextSprints. (2025). Scalable Capital Product Strategy Guide. Available online: https://nextsprints.com/guide/scalable-capital-product-strategy-guide.

Njegovanović, A. (2018). Artificial Intelligence: Financial Trading and Neurology of Decision. Financial Markets, Institutions and Risks, pp.58–68. doi:https://doi.org/10.21272/fmir.2(2).58-68.2018.

Nourallah, M., Öhman, P., Walther, T. & Nguyen, D. (2025). Financial Robo-Advisors: A Comprehensive Review and Future Directions.

Oreoluwa Onabowale (2025). The Rise of AI and Robo-Advisors: Redefining Financial Strategies in the Digital Age. International Journal of Research Publication and Reviews, 6(6), pp.4832–4832. doi:https://doi.org/10.55248/gengpi.6.0125.0640.

Paolo Sironi (2016). FinTech innovation: from robo-advisors to goals based investing and gamification. Chichester, West Sussex, UK: Wiley.

Pokholkova, M. & Kriebitz, A. (2023). The Phenomena of Robo-Advisors: Analysis of Challenges. ResearchGate. doi:https://doi.org/10.13140/RG.2.2.12800.03840.

Searle, J.R. (1980). Minds, brains, and programs. Behavioral and Brain Sciences, 3(3), pp.417–457. doi:https://doi.org/10.1017/s0140525x00005756.

Severino, F. & Thierry, S. (2022). Big Data in Finance. Springer Nature.

Stahl, B.C. (2021). Artificial Intelligence for a Better Future. SpringerBriefs in Research and Innovation Governance. Cham: Springer International Publishing. doi:https://doi.org/10.1007/978-3-030-69978-9.

Statista (2023). Robo-Advisors – Worldwide Statista Market Forecast. Statista. Available online: https://www.statista.com/outlook/fmo/wealth-management/digital-investment/robo-advisors/worldwide.

Tertilt, M. & Scholz, P. (2017). To Advise, or Not to Advise — How Robo-Advisors Evaluate the Risk Preferences of Private Investors. papers.ssrn.com. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2913178.

Tversky, A. and Kahneman, D. (1992). Advances in Prospect Theory: Cumulative Representation of Uncertainty. Journal of Risk and Uncertainty, 5(4), pp.297–323. Available online: https://www.jstor.org/stable/41755005.

Veale, M. & Zuiderveen Borgesius, F. (2021). Demystifying the Draft EU Artificial Intelligence Act. papers.ssrn.com. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3896852.

Walter Lam, J. (2016). Robo-Advisors: A Portfolio Management Perspective. Yale Department of Economics. Available online: https://economics.yale.edu/sites/default/files/2023-01/Jonathan_Lam_Senior%20Essay%20Revised.pdf.

Wealthfront (2019). Wealthfront: High-Interest Cash, Free Financial Planning & Robo-Investing for Millennials. Wealthfront.com. Available online: https://www.wealthfront.com/.

Wolford, B. (2025). What is GDPR, the eu’s new data protection law? GDPR.EU. Available online: https://gdpr.eu/what-is-gdpr/.

World Bank Group (2024). The Use of Alternative Data in Credit Risk Assessment: Opportunities, Risks, and Challenges. World Bank. Available online: https://openknowledge.worldbank.org/server/api/core/bitstreams/dde85d69-37ac-415e-bc9d-9d6990189da2/content.

{kind=link}