Abstract

ESG investment was regarded as an important tool for addressing climate change after the 2015 Paris Agreement set a 1.5℃ global warming limit. However, there is still more fossil-fuel investment over ESG investment in the US market. In this study, we explore why US investors still choose to allocate funds to fossil fuel assets. We focus on analysing the economic drivers, psychological factors and institutional barriers that drive this decision. We use a qualitative multi-method design to find answers, combining a structured literature review, case analysis and content analysis. The data covers Morningstar Direct fund-level data from January 2014 to March 2025, which includes 640 sustainable funds and 198 fossil fuel-focused funds. The data shows that US ESG funds experienced a net outflow for the tenth consecutive quarter in the first quarter of 2025. In contrast, fossil energy funds recorded positive inflows from 2022 to 2025, and their annualised return rate was higher than the ESG funds. Investors are preferring fossil-fuel investment because of their financial stability and strong historical performance. This study suggests that in order to revitalise ESG investment, we must address uncertainties and enhance the transparency of the ESG rating framework.

Introduction

Over recent decades, climate change has become a trending topic in the world market. First recognised as an intercontinental issue in 1988 with the creation of the Intergovernmental Panel on Climate Change (IPCC), it has since become a top priority after the 2015 UN Climate Change Conference (COP21), in which the Paris Agreement was first settled. This established the global warming limit of 1.5℃ above pre-industrial levels, creating a global framework for global temperature maintenance and aiming to reduce greenhouse gas emissions by 43% by 2030.

The following years were marked by ESG (Environmental, Social and Governance) market participation. ESG, first introduced in 2004 (World Bank, 2004), is a set of criteria used by investors and organisations to measure a company’s sustainability, ethical impact and risk management. It goes beyond financial profit to assess how a company manages its environmental footprint, relationships with stakeholders and internal governance, often determining long-term viability and investment attractiveness (UN, 2023).

The term ‘green asset’ refers to financial or real assets allocated to activities that substantially contribute to recognised environmental objectives, particularly climate mitigation and sustainability (European Parliament & Council, 2020). In contrast, ‘brown assets’ refer to assets linked to economic activities with high carbon intensity or significant negative environmental externalities, exposing them to climate transition risks and regulatory constraints (Bank of International Settlements, 2020).

As the popularity of ESG ideals grew, diverse companies capitalised on the structural transition. ESG ratings were created as assessments that measure a company’s long-term exposure to and management of environmental, social and governance risks and opportunities.

By 2020, the ESG ETF market had reportedly risen by over 318%, indicating significant optimism among investors in the US (Bloomberg, 2021). According to Morningstar, global net inflow in mutual funds and exchange-traded products was about $649.1 billion by 2021. Annual ESG fund inflow in the US increased from $5.4 billion in 2018 to $69.8 billion in 2021, yet dramatically decreased the following year, hitting $3 billion (USD) by 2022 (Morningstar, 2023). Simultaneously, the US’s largest ESG funds’ assets were hit with losses ranging from 26% to 18% (Investopedia, 2023). In the first quarter of 2025, the US reached its tenth consecutive quarter of net outflow, with withdrawals reaching $6.1 billion in Q1 2025 (Morningstar, 2025).

This article will cover the factors that led investors to disengage from ‘green assets’ and migrate back to ‘brown assets’, including: (I) how ESG ratings cause hesitancy in investors due to specific ESG metrics for companies such as employee safety and anti-corruption rating dissonance; (II) implications with funds’ fiduciary duties; and (III) public knowledge.

We approach the problem in three steps. First, we present our methods. The study employed a structured research design appropriate to the research question, using either a quantitative, qualitative or mixed-methods approach depending on the objectives of the investigation. Data was collected from a defined sample selected through appropriate sampling techniques to ensure representativeness and reliability. Data analysis was conducted using suitable statistical or thematic analysis techniques, ensuring validity, reliability and replicability of the findings. Second, we move forward to results: the key findings derived from the data analysis without interpretation. Statistical tests, descriptive measures, tables and figures were used to summarise the outcomes of the study. The findings indicate patterns, relationships or differences among variables, depending on the research design. Third, we present our discussion, in which we examine how financial performance solely does not present significant weight on green investing in the US. Alongside, economic performance, we analyse comprehensively how fiduciary duties, market sentiment, psychological and personal factors, as well as political backlash, influence investors’ decision-making.

Aims

This study aims to investigate why investors continue to allocate capital to fossil-fuel assets despite increasing awareness of climate change and the rapid growth of sustainable investing.

Over the past decade, ESG investing has expanded significantly and has been promoted as a more responsible alternative to traditional investing. However, fossil-fuel companies continue to receive large amounts of investment. This suggests that financial and psychological factors play an important role in investor decision-making.

This study focuses on four main objectives.

DATA SOURCES AND SEARCH STRATEGY

Primary data for this study was sourced from academic and professional databases, with a focus on Google Scholar to ensure comprehensive coverage across disciplines. The corpus of analysed material includes:

- Peer-reviewed journal articles in finance, economics, environmental policy and sustainability studies;

- Academic working papers and scholarly book chapters;

- Authoritative industry reports from financial institutions, non-partisan think tanks and regulatory bodies.

The search strategy utilised an iterative keyword approach to ensure both breadth and relevance. Core search terms included: “ESG investment”, “public ESG perception”, “fossil fuel investment vs. ESG”, “investor attitudes toward sustainability risk” and “energy transition finance”. Furthermore, citation chaining (backward and forward reference tracking) was employed to identify seminal works and recent developments within the field.

ELIGIBILITY CRITERIA

To maintain the rigour and focus of the analysis, specific inclusion and exclusion criteria were applied to all potential sources.

Inclusion Criteria

Sources were included in the final synthesis if they met the following parameters:

- Direct relevance: Addressed ESG investing, fossil fuel finance or sustainable asset allocation as a primary theme.

- Thematic depth: Examined investor behaviour, market incentives, financial performance or policy influences pertinent to investment decision-making.

- Source credibility: Consisted of peer-reviewed academic publications, scholarly working papers or verified institutional/industry reports.

- Language: Published in English.

Exclusion Criteria

Sources were excluded if they fell into the following categories:

- Lack of rigour: Opinion pieces, non-academic blogs or commentary lacking empirical grounding or methodological transparency.

- Scope mismatch: Focused exclusively on general sustainability topics without a clear nexus to investment or financial markets.

Results

This study analyses mutual funds and exchange trade funds over the course of January 2014 to March 2025. Fund-level data was obtained from Morningstar Direct, which classifies sustainable investment products using its Sustainable-Investing Framework. Aggregate sustainable asset data was cross-referenced with reports published by US SIF and the Global Sustainable Investment Alliance.

The study consists of 640 US sustainable (ESG-labelled) funds, 198 fossil-fuel focused US energy sector funds and 7,884 fund-year observations.

Sustainable funds are defined as those identified by Morningstar as incorporating explicit ESG integration, sustainable themes or impact mandates. Fossil-driven funds are defined as funds categorised under US energy equity sectors with primary exposure to oil, gas and coal industries.

AGGREGATE SUSTAINABLE ASSETS UNDER MANAGEMENT (AUM)

According to the GSIA (2022), US sustainable investments declined from $17.1 trillion in 2020 to $8.4 trillion in 2022, representing a 50.9% reduction under revised classification standards. More recent data from US SIF (2025) indicated that sustainable assets totalled $6.6 trillion in 2024, representing approximately 11% of the $61.7 trillion US professionally managed asset market.

FUND-LEVEL DESCRIPTIVE STATISTICS

Table 1 presents summary statistics for the full sample.

| Variable | ESG Fund (Mean) | Fossil Funds (Mean) |

|

Total Net Assets (USD Millions) |

512.4 |

438.7 |

|

Annual Return (%) |

8.3 | 11.9 |

|

Volatility (%) |

19.7 | 28.4 |

|

Net Flow (2022-2025) |

-$0.42B | +$0.91B |

|

Expense Ratio (%) |

0.58 | 0.72 |

Table 1.

Between 2022 and 2025, ESG funds experienced persistent negative net flows, averaging $13 to $19 billion annually at the aggregate level (Morningstar, 2025). Meanwhile fossil energy funds recorded positive inflows, particularly during 2022 and 2023, coinciding with energy sector outperformance.

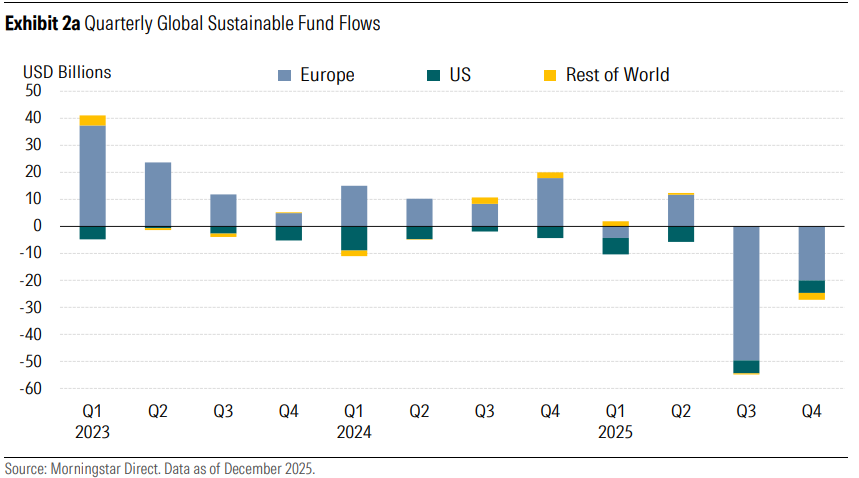

QUARTERLY U.S. SUSTAINABLE FUND FLOWS

Figure 1 presents quarterly net flows into US sustainable funds from Q1 2023 through Q4 2025. The US component (green bars) reveals a clearly persistent pattern of capital withdrawal from ESG vehicles.

In Q1 2023, US sustainable funds already exhibited net outflows (approximately $5 billion), marking the continuation of redemptions that began in 2022. While outflows moderated temporarily during mid-2023 and early 2024, the US never returned to positive inflows during the observed period.

The retraction flows intensified noticeably in 2025. After modest outflows in Q1 and Q2 2025 (approximately $7 to $9 billion per quarter), US sustainable funds experienced a drastic acceleration of capital in Q3 2025, with net outflows approaching $55 billion. Although Q4 2025 showed partial stabilisation, flows remained decisively negative (approximately $20 to $25 billion).

Figure 1 (Morningstar Direct, 2025).

U.S. SUSTAINABLE FUND ANNUAL OUTFLOWS

As previously stated, 2021 presented a promising future for ESG, but had its vision contrarian factors (as seen in Figure 1). Both active and passive investors had a drastic capital withdrawal, with 2024’s fund outflows topping approximately $19.6 billion. Compared with the previous year (2023), whose annual fund outflows were $13.3 billion, 2024 presented substantial outflows, increasing by 47.4% (Morningstar, 2024).

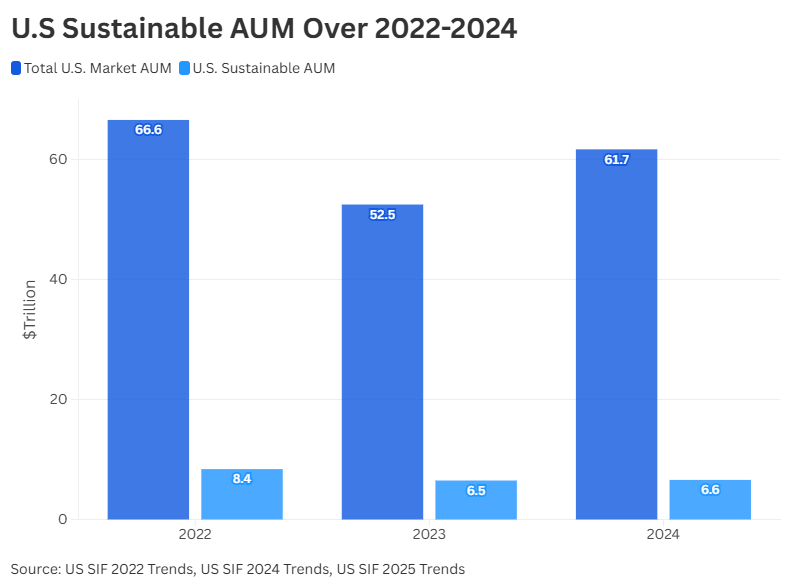

US sustainable assets under management (Figure 2) declined from $8.4 trillion in 2022 to $6.5 trillion in 2023 (-22.6%), with only a recovery to $6.6 trillion in 2024. While total US market AUM recovered from $52.5 trillion in 2023 to $61.7 trillion in 2024, sustainable assets did not recover proportionally. As a result, ESG assets’ share of total US AUM fell from approximately 12.6% in 2022 to 10.7% in 2024, indicating both absolute contraction and relative market share loss.

Figure 2 (Morningstar Direct, 2025).

Figure 3 (US SIF, 2025).

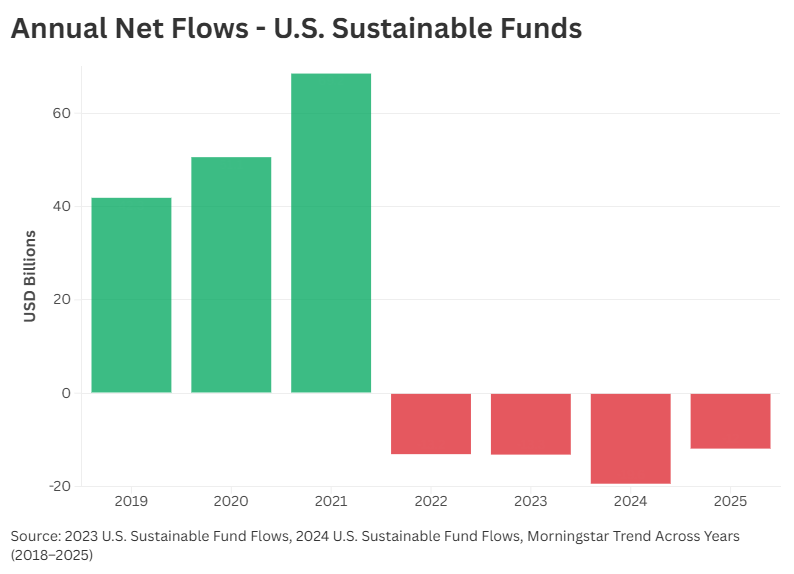

Figure 4 (Morningstar Direct, 2025).

As seen in Figure 4, US sustainable funds experienced strong positive net inflows between 2019 and 2021, rising from approximately $41 billion in 2019 to nearly $69 billion in 2021. However, this reversed drastically in 2022, when flows turned negative (around $13 billion), marking the beginning of sustained capital withdrawals. Outflows continued through 2023 ($13 billion) and deepened in 2024 to approximately $19 billion (Morningstar Report, 2024). Preliminary 2025 data indicates ongoing negative flows.

Overall, the empirical evidence indicates a considerable reversal in the US sustainable investment dynamics after 2021. Annual net flows shifted from sustained positive inflows (2019-2021) to persistent outflows beginning in 2022. Currently, sustainable assets under management declined in absolute terms and lost market share within total US professionally managed assets. Quarterly flow data confirms continued withdrawal pressure throughout 2023-2025.

Taken together, the results documented a shift in capital allocation patterns, characterised by a decline in ESG-labelled investment vehicles within the US market during the post-2021 period.

Discussion

The findings suggest that investment decisions favouring brown assets cannot be explained solely by financial performance; instead, they emerge from a combination of economic incentives, psychological biases and structural challenges within ESG investing.

1. ECONOMIC AND PERFORMANCE CONSIDERATIONS

One important explanation for continued investment in fossil-fuel assets is the perception that they offer stronger and more predictable financial returns (Ilhan et al., 2023). Especially during periods of market volatility, investors tend to favour sectors that have historically demonstrated resilience. The energy sector, particularly oil and gas, has often benefitted from geopolitical tensions, supply disruptions and inflationary pressures, reinforcing its reputation as a financially stable industry. As a result, many investors may view fossil-fuel assets as a safer option compared to ESG – focused funds, which are sometimes perceived as more sensitive to regulatory shifts or technological uncertainty. The sustained outflows from sustainable funds after 2021 suggest that performance expectations remain central to allocation decisions (Morningstar, 2025).

Institutional incentives further strengthen this pattern. Portfolio managers are frequently evaluated based on short-term performance benchmarks and quarterly returns. In such an environment, strategies that prioritise risk-adjusted returns may appear more prudent than those centred on long-term sustainability goals (Eccles & Klimenko, 2019). Although ESG integration is increasingly framed as financially material, uncertainty about how sustainability factors translate into measurable performance can discourage large reallocations of capital. This reflects the continued dominance of traditional financial frameworks in which fiduciary responsibility is often interpreted primarily in terms of financial outcomes.

At the same time, economic reasoning alone does not fully explain investor behaviour. Research in behavioural finance shows that investment decisions are shaped by values, social identity and psychological biases (Riedl & Smeets, 2017). Some investors choose ESG funds even when they expect slightly lower returns, indicating that ethical considerations and personal beliefs can influence financial decision-making. However, this relationship is not stable. When ESG funds underperform or when sustainability outcomes become less visible, investors may quickly revert to conventional assets.

Psychological factors such as familiarity bias and loss aversion may also explain this shift. Fossil-fuel companies have long established performance records, making them appear more reliable during uncertainty, while ESG strategies are sometimes seen as newer or riskier.

Perception and credibility also affect capital flows. Sustainability labels can attract investors (Riedl & Smeets, 2017) but doubts about ESG performance or greenwashing may reduce confidence and push investors back toward brown assets.

2. ESG RATING UNCERTAINTY AND TRUST PROBLEMS

A major barrier to ESG investors is the inconsistency between ESG rating agencies. There were over 4,827 signatories to the UN-supported initiative, Principles for Responsible Investment (PRI), whose AUM reached $128.4 trillion by 2024 (PRI, 2024). According to Jonsdottir et al. (2022), to effectively incorporate ESG factors into investment decisions, institutional investors need access to substantial volumes of high-quality ESG data to assess companies’ performance across environmental, social and governance dimensions. As a result, companies must publish their sustainability performance reports. The drawback here is that multiple standards and frameworks can be used by different companies for ESG reporting. The most widely adopted of these is the Global Reporting Initiative (GRI) (Delmas et al., 2010). Despite the volume and variety of ESG data, institutional investors, asset managers and hedge funds seem reluctant to pursue ESG assets as part of their portfolio management (Belkhir et al., 2017). Some of that outflow can be attributed to how challenging it is to efficiently determine the quality of an ESG dataset (Monk et al., 2021). As companies can choose which reporting standard they use, this can result in a disjuncture in other ESG areas (GRI, 2019). To provide clearance, consistency and coherence, the GRI principles originated as a set of internationally recognised guidelines that ensure sustainability reporting is transparent, comparable, accurate and stakeholder-oriented (GRI, 2021a; GRI, 2021b). However, studies show that despite companies acknowledging the strategic importance of ESG disclosure and ESG reporting growth, the information provided is often broad and non-specific, reducing its material relevance and practical utility for investment decision-making (Jonsdottier et al., 2022; Khan et al., 2015; Amel-Zadeh et al., 2017).

The GRI establishes that ESG disclosures must achieve a level of precision that allows stakeholders to reliably evaluate organisational performance. Yet, as highlighted by George Kotsantonis et al. (2019), the coexistence of multiple, fragmented classes creates significant procedural burdens. This institutional fragmentation intensifies administrative complexity and cost pressures, likely discouraging clear transparency. Under such limitations, firms may strategically reduce the range of disclosure or release information of limited depth and reliability, generating a lack of data across critical ESG categories.

The self-assessment of ESG performance is considered largely unreliable by institutional investors, to the extent that companies may have an ‘optimistic’ approach in their report, not corresponding to how they conduct actions (Pagano et al., 2018; Cho, 2014). Firms with weaker performance frequently engage in impression management by framing ESG reports in vague, but still positively-toned, language, obscuring underlying deficiencies (Michelon, 2014). At the same time, companies exposed to higher operational risk often expand the volume of ESG disclosures as a reputational defensive strategy. While such reports may serve symbolic purposes, increased transparency can mitigate informational disparities and, in turn, contribute to a reduction in perceived firm risk (Lueg, 2019).

The Directive 2014/95/EU marked the shift from voluntary to mandatory non-financial disclosure in the EU, aiming to increase transparency and comparability (European Parliament and Council, 2014). Empirical studies find that mandatory ESG reporting increases disclosure levels and standardisation, particularly among previously low-disclosing firms (Caputo et al., 2020; Mion & Adaui, 2020). However, evidence also shows persistent data gaps, limited comparability and reliability concerns due to weak internal controls and heterogeneous reporting practices (Venturelli et al., 2017; Gatti et al., 2019).

3. FIDUCIARY DUTIES AND INSTITUTIONAL CONSTRAINTS

A major barrier identified for ESG investors relates to fiduciary duties and institutional constraints governing portfolio management. Institutional investors operate under legal obligations to act in the best financial interests of beneficiaries, traditionally interpreted as prioritising risk-adjusted returns (Freshfields Bruckhaus Deringer, 2005). According to the PRI, fiduciary duty does not prevent ESG integration; rather, ESG factors can be financially material and therefore consistent with fiduciary responsibility (PRI, 2019). Nevertheless, ambiguity surrounding how ESG considerations align with prudence and loyalty standards continues to create uncertainty among asset owners and managers.

In the United States, regulatory interpretations of fiduciary obligations under the US Department of Labor have fluctuated, particularly regarding ESG integration in ERISA-governed retirement plans (US Department of Labor, 2020; US Department of Labor, 2022). Such regulatory shifts contribute to institutional hesitancy, as fiduciaries may fear litigation or regulatory scrutiny if ESG investments underperform relative to conventional benchmarks (Krueger, Sautner & Starks, 2020). Consequently, even when ESG risks are financially relevant, institutional constraints may limit portfolio reallocation toward sustainable assets.

Furthermore, short-term performance evaluation metrics and benchmarking practices reinforce conservative investment behaviour. As highlighted by Eccles and Klimenko (2019), institutional investors often face agency pressures that incentivise short-term returns over long-term sustainability considerations. Similarly, Bebchuk and Tallarita (2020) argue that stakeholder-oriented commitments may conflict with shareholder primacy norms embedded in corporate governance frameworks. These structural constraints reduce flexibility in integrating ESG considerations, particularly where financial materiality is contested or difficult to quantify.

Empirical evidence suggests that fiduciary uncertainty and institutional rigidities contribute to slower ESG adoption in pension funds and mutual funds compared to voluntary commitments publicly endorsed by asset managers (Renneboog, Ter Horst & Zhang, 2008; Dyck et al., 2019). Thus, while ESG integration is increasingly framed as compatible with fiduciary duty, legal ambiguity, regulatory variability and performance pressures continue to constrain its systematic implementation.

4. CHANGING MARKET SENTIMENT

Recent trends suggest that ESG investing faces a period of reevaluation (Eccles & Klimenko, 2019). Global sustainable fundamentals experienced notable outflows in early 2025, reflecting regulatory debates, political pressures and performance concerns.

These developments illustrate how external narratives and market sentiment can rapidly influence investor behaviour. Rather than a rejection of sustainability itself, this shift may represent investor uncertainty about how ESG frameworks should be applied in practice.

5. GOVERNMENT PUSHBACK AGAINST ESG

The governments of the United States, both federal and state, play an important role in the economy as regulators and policy-setters. This proves especially important in the application of ESG as past governments – mainly under the Biden administration – have introduced legislation curbing unsustainable investment and encouraging ESG through policies (EPA, 2022) such as the Inflation Reduction Act, which aimed to cut down national carbon emissions by roughly 40% from 2005 levels through subsidised sustainable energy and hundreds of billions of dollars in clean energy tax credits (US 117th Congress, 2021). Under the Trump administration, however, this policy of encouraging ESG has been halted and even reversed.

Donald Trump’s administration has overseen a vast American pullback in domestic and international sustainability projects and agreements. Notably, the United States withdrew from the Paris Climate Agreement (US Department of State, 2019), signalling an end to government concern regarding the climate crisis and any major efforts to support the growth of ESG. This withdrawal from the Paris Agreement also shows investors that the largest economy on the planet is no longer interested in combatting climate change, which may lead to significant consequences for the nature of ESG in the American economy. Trump’s administration has also reduced government regulation on the energy sector, announcing that it planned to ‘streamline’ the energy sector by removing anything deemed as ‘red tape’ (Alhamis, 2025). The reduced regulatory powers of the government affect ESG the strongest because it was these regulations which allowed ESG to become a safe option for investment; without these regulations, investors are now even more inclined to invest in unsustainable energies over ESG. These developments in the government show that the American economy is highly likely to shift towards unsustainable energies away from ESG, as the government continues to discourage ESG in favour of fossil fuels.

Conclusion

This study investigated the economic and psychological factors that explain continued investment in fossil-fuel assets despite the growth of sustainable investing. The findings suggest that fossil-fuel investments remain attractive primarily because of their financial stability and strong historical performance. Many investors prioritise reliable returns and lower perceived risks, which fossil-fuel companies often provide.

The data analysed in this study shows that sustainable investments have faced significant challenges in recent years. Investment flows into ESG funds declined after 2021, and sustainable assets under management fell before only partially recovering. At the same time, traditional investment markets continued to grow. This indicates that sustainable investments have struggled to compete with traditional energy investments. Psychological factors also play an important role. Investors often prefer familiar industries and may be reluctant to change established investment strategies. Fear of financial loss and uncertainty about ESG investments further discourage investors from shifting away from fossil fuels.

These results suggest that increasing sustainable investment will require more than environmental awareness. Investors must also have confidence that sustainable investments can provide stable and competitive financial returns. Future research could examine how government policies, technological advances and market developments may influence investment behaviour. Understanding these factors may help explain whether sustainable investing will become more competitive in the future.

Bibliography

Alhamis, I. (2025) “The Resurgence of Trumponomics: Implications for the Future of ESG Investments in a Changing Political Landscape”, arXiv:2502.02627 [pdf]. <https://arxiv.org/pdf/2502.02627>

Amel-Zadeh, A. & Serafeim, G. (2017) “Why and How Investors Use ESG Information: Evidence from a Global Survey”, Harvard Business School Working Paper, 17-079 [pdf]. <https://dash.harvard.edu/server/api/core/bitstreams/7312037e-191e-6bd4-e053-0100007fdf3b/content>

Avramov, D., Cheng, S., Lioui, A. & Tarelli, A. (2022) “Sustainable investing with ESG rating uncertainty”, Journal of Financial Economics, 145(2B), pp. 642–664.

Bebchuk, L.A. & Tallarita, R. (2020) “The Illusory Promise of Stakeholder Governance”, Cornell Law Review, 106, pp. 91–178.

Belkhir, L., Bernard, S. & Abdelgadir, S. (2017) “Does GRI reporting impact environmental sustainability? A cross-industry analysis of CO₂ emissions performance between GRI-reporting and non-reporting companies”, Management of Environmental Quality: An International Journal, 28(2), pp. 138–155.

Berg, F., Koelbel, J.F. & Rigobon, R. (2022) “Aggregate Confusion: The Divergence of ESG Ratings”, Review of Finance, 26(6), pp. 1315–1344.

Besel, R.D. (2013) “Accommodating Climate Change Science: James Hansen and the Rhetorical/Political Emergence of Global Warming”, Science in Context, 26(1), pp. 137–152.

Bioy, H., Wang, B., Lennkvist, A., Mitchell, L., Popat, S., Beaudoin, H., Yanagi, J. (2026) “Global Sustainable Fund Flows: Q4 and Full-Year 2025 in Review”, Morningstar [pdf]. <https://www.morningstar.com/content/cs-assets/v3/assets/blt9415ea4cc4157833/blt1d54e64f88b82b3b/Global_ESG_Flows_Q4_2025_Report.pdf>

Bolton, P., Despres, M., Pereira Da Silva, L.A., Samama, F. & Svartzman, R. (2020) “The green swan: Central banking and financial stability in the age of climate change”, Bank for International Settlements [pdf]. <https://www.bis.org/publ/othp31.pdf>

Carmo, C. & Ribeiro, C. (2022) “Mandatory Non-Financial Information Disclosure under European Directive 95/2014/EU: Evidence from Portuguese Listed Companies’, Sustainability, 14(8), 4860.

Cesarone, F., Martino,, M.L., Ricca, F. & Scozzari, A. (2023) “Managing ESG Ratings Disagreement in Sustainable Portfolio Selection”, arXiv.2312.10739v1 [pdf]. <https://arxiv.org/pdf/2312.10739>

Cho, C.H., Laine, M., Roberts, R.W. & Rodrigue, M. (2015) “Organized hypocrisy, organizational façades, and sustainability reporting”, Accounting, Organizations and Society, 40, pp. 78–94.

Congress.gov (2021) “H.R.5376 – An act to provide for reconciliation pursuant to title II of S. Con. Res. 14”, 117th Congress (2021-2022) [online]. <https://www.congress.gov/bill/117th-congress/house-bill/5376>

Delmas, M. & Blass, V.D. (2010) “Measuring corporate environmental performance: the trade-offs of sustainability ratings”, Business Strategy and the Environment, 19(4), pp. 245–260.

Dyck, A., Lins, K.V., Roth, L. & Wagner, H.F. (2019) “Do institutional investors drive corporate social responsibility? International evidence”, Journal of Financial Economics, 131(3), pp. 693–714.

Eccles, R.G. & Klimenko, S. (2019) “The Investor Revolution: Shareholders are getting serious about sustainability”, Harvard Business Review [online]. <https://hbr.org/2019/05/the-investor-revolution>

Employee Benefits Security Administration, U.S. Department of Labor (2020) “Financial Factors in Selecting Plan Investments”, Federal Register of the United States Government [online]. <https://www.federalregister.gov/documents/2020/11/13/2020-24515/financial-factors-in-selecting-plan-investments>

Employee Benefits Security Administration, U.S. Department of Labor (2022) “Final Rule on Prudence and Loyalty in Selecting Plan Investments and Exercising Shareholder Rights”, Employee Benefits Security Administration [online]. <https://www.dol.gov/agencies/ebsa/about-ebsa/our-activities/resource-center/fact-sheets/final-rule-on-prudence-and-loyalty-in-selecting-plan-investments-and-exercising-shareholder-rights>

EUR-Lex (2014) “Directive 2014/95/EU of the European Parliament and of the Council of 22 October 2014 amending Directive 2013/34/EU as regards disclosure of non-financial and diversity information by certain large undertakings and groups” European Union [online]. <https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32014L0095>

EUR-Lex (2020) “Regulation (EU) 2020/852 of the European Parliament and of the Council of 18 June 2020 on the establishment of a framework to facilitate sustainable investment, and amending Regulation (EU) 2019/2088”, European Union [online]. <https://eur-lex.europa.eu/eli/reg/2020/852/oj/eng>

Gatti, L., Seele, P. & Rademacher, L. (2019) “Grey zone in – greenwash out. A review of greenwashing research and implications for the voluntary-mandatory transition of CSR”, International Journal of Corporate Social Responsibility, 4(6).

Gelfand, A. (2025) “Young people are losing interest in sustainable investing, survey shows”, Stanford Report [online]. <https://news.stanford.edu/stories/2025/01/young-investors-support-esg-dropped-dramatically-2024>

Global Compact (2004) “Who Cares Wins: Connecting Financial Markets to a Changing World”, The Global Compact [pdf]. <https://documents1.worldbank.org/curated/en/280911488968799581/pdf/113237-WP-WhoCaresWins-2004.pdf>

GRI (n.d.) “The global standards for sustainability impact”, Global Reporting Initiative [online]. <https://www.globalreporting.org/standards>

GRI (2019) “Driving Alignment in Climate-related Reporting”, Global Reporting Initiative [online]. <https://www.globalreporting.org/news/news-center/2019-09-24-driving-alignment-in-climate-related-reporting/>

GRI (2021a) “GRI 1: Foundation 2021”, BeCause [online]. <https://help.because.eco/en/articles/6183296-gri-1-foundation-2021>

GRI (2021b) “GRI 2: General Disclosures 2021”, BeCause [online]. <https://help.because.eco/en/articles/6114339-gri-2-general-disclosures-2021>

Ignatius, A. (2019) “ESG Comes of Age”, Harvard Business Review [online]. <https://hbr.org/2019/05/esg-comes-of-age>

Jonsdottir, B., Sigurjonsson, T.O., Johannsdottir, L. & Wendt, S. (2022) “Barriers to Using ESG Data for Investment Decisions”, Sustainability, 14(9), 5157.

Khan, M., Serafeim, G. & Yoon, A. (2015) “Corporate Sustainability: First Evidence on Materiality”, The Accounting Review, 91(6), pp. 1697–1724.

Knobloch, F. & Mercure, J.-F. (2016) “The behavioural aspect of green technology investments: A general positive model in the context of heterogeneous agents”, Environmental Innovation and Societal Transitions, 21, pp. 39–55.

Kotsantonis, S. & Serafeim, G. (2019) “Four Things No One Will Tell You About ESG Data”, Journal of Applied Corporate Finance, 31(2), pp. 50–58.

Krueger, P., Sautner, Z. & Starks, L.T. (2019) “The Importance of Climate Risks for Institutional Investors”, ECGI Finance Working Paper No. 610/2019 [pdf]. <https://www.ecgi.global/sites/default/files/working_papers/documents/finalkruegersautnerstarks_0.pdf>

Lueg, K., Krastev, B. & Lueg, R. (2019) “Bidirectional effects between organizational sustainability disclosure and risk”, Journal of Cleaner Production, 229, pp. 268–277.

McCahery, J.A., Pudschedl, P.C. & Steindl, M. (2022) “Institutional Investors, Alternative Asset Managers, and ESG Preferences”, European Business Organization Law Review, 23, pp. 821–868.

Melloni, G., Caglio, A. & Perego, P. (2017) “Saying more with less? Disclosure conciseness, completeness, and balance in Integrated Reports”, Journal of Accounting and Public Policy, 36(3), pp. 220–238.

Michelon, G., Pilonato, S. & Ricceri, F. (2015) “CSR reporting practices and the quality of disclosure: An empirical analysis”, Critical Perspectives on Accounting, 33, pp. 59–78.

Monk, A. & Rook, D. (2021) “Resilience as an Analytical Filter for ESG Data”, SSRN [pdf]. <https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3968081>

Morningstar Manager Research (2024) “What Are Sustainable Funds, and How Have They Performed?”, Morningstar [online]. <https://www.morningstar.com/business/insights/blog/us-sustainable-funds-performance>

Ortez, M.A., Smith, M.L. & Widmar, N.O. (2026) “U.S. Public Perceptions of “Environmental, Social and Governance (ESG)” Investments”, Journal of Consumer Policy, 49(5).

Pagano, M. S., Sinclair, G. & Yang, T. (2018) “Understanding ESG ratings and ESG indexes” in Boubaker, S., Cumming, D. & Nguyen, D. K. (eds.) Research Handbook of Finance and Sustainability (Cheltenham: Edward Elgar Publishing), pp. 339–371.

Pelster, M., Horn, M. & Oehler, A. (2024) “Who cares about ESG?”, Journal of Climate Finance, 8(100045).

PRI Association (2020) “Principles for Responsible Investment 2020 Signatory General Meeting Minutes”, Principles for Responsible Investment Association [pdf]. <https://dwtyzx6upklss.cloudfront.net/Uploads/a/x/e/2020_10_21_pri_signatory_general_meeting_minutes_2020_793014.pdf>

PRI Association (2024) “Annual Report 2024”, Principles for Responsible Investment [pdf]. <https://dwtyzx6upklss.cloudfront.net/Uploads/v/y/x/annualreport2024_final_98918.pdf>

Renneboog, L., Ter Horst, J. & Zhang, C. (2008) “Socially responsible investments: Institutional aspects, performance, and investor behavior”, Journal of Banking & Finance, 32(9), pp. 1723–1742.

Riedl, A. & Smeets, P. (2017) “Why Do Investors Hold Socially Responsible Mutual Funds?”, Journal of Finance, 72(6), pp. 2505–2550.

Sabban, A. & Jackson, R. (2023) “U.S. Fund Flows: Investors Bail in 2022”, Morningstar [online]. <https://www.morningstar.com/funds/us-fund-flows-investors-bail-2022>

Sahin, Ö., Bax, K., Czado, C. & Paterlini, S. (2022) “Environmental, Social, Governance scores and the Missing pillar — Why does missing information matter?”, Corporate Social Responsibility and Environmental Management, 29(5), pp. 1782–1798.

Six Group (2024) “ESG Ratings: Who Assigns Them? How Do They Originate? And Why Are They Important?”, Six Group [online]. <https://www.six-group.com/en/blog/esg-ratings-explained.html>

Stankiewicz, A. & Roy, M. (2024) “U.S. Sustainable Funds Landscape 2024 in Review”, Morningstar. [pdf] <https://www.morningstar.com/business/insights/research/sustainable-funds-landscape-report>

Tyndall, J. (1861) “I. The Bakerian Lecture.—On the absorption and radiation of heat by gases and vapours, and on the physical connexion of radiation, absorption, and conduction”, Phil. Trans. R. Soc, 151, pp. 1–36.

United Nations (n.d.) “The Paris Agreement”, United Nations [online]. <https://www.un.org/en/climatechange/paris-agreement>

United Nations (n.d.) “The Paris Agreement”, United Nations Framework Convention on Climate Change [online]. <https://unfccc.int/process-and-meetings/the-paris-agreement>

United Nations (2005) “A legal framework for the integration of environmental, social and governance issues into institutional investment”, United Nations Environment Programme Finance Initiative [pdf]. <https://www.unepfi.org/wordpress/wp-content/uploads/2022/07/Freshfields-A-legal-framework-for-the-integration-of-ESG-issues-into-institutional-investment.pdf>

United Nations (2019) “Fiduciary Duty in the 21st Century: Final Report”, United Nations Environment Programme Finance Initiative [pdf]. <https://www.unepfi.org/wordpress/wp-content/uploads/2019/10/Fiduciary-duty-21st-century-final-report.pdf>

United Nations (2023) “The Short Guide to ESG”, United Nations Development Programme [online]. <https://www.undp.org/serbia/publications/short-guide-esg>

US Sustainable Investment Forum (2025) “US SIF’s 30th Anniversary “Trends Report” Finds Sustainable Investing Asset Base Holding Amid Political Headwinds, US SIF [online]. <https://www.ussif.org/news/press-releases/us-sifs-30th-anniversary-trends-report-finds-sustainable-investing-asset>

Zhang, C. & Hsu, W.-L. (2025) “ESG rating divergence and stock price crash risk”, International Journal of Financial Studies, 13(3), 147.

Zubizarreta, H.V. & Aquino, D.T. (2026) “Understanding ESG Ratings: A Systematic Literature Review of Methodologies, Divergences, Impact, Standardization, Disclosure Quality, Technology, and Global Financial Implications (2020–2025)”, preprint [online]. <https://www.preprints.org/manuscript/202601.0203>

{kind=link}