Abstract

As financial technology reshapes global investing, Southeast Asia has emerged as a key region for the evolution of robo-advisory platforms, a change driven by rising digital literacy, mobile-first behaviour, and a growing population of millennial and Gen Z investors as well as evolving generational ideals. This paper examines how robo-advisors in Southeast Asia are transforming investment behaviour through the integration of artificial intelligence (AI) and behavioural finance. It explores the psychological principles and factors of investor decisions, identifies common biases such as loss aversion and herding, and analyses how AI-powered “nudges”, advice, personalisation tools and predictive analytics are playing an important role in mitigating these behavioural tendencies. Through detailed case studies of regional platforms like Endowus, Syfe and Ajaib, we show how robo-advisors are not only optimising portfolios but also reshaping emotional responses to financial markets, providing key insights to help users make mindful, rational decisions. It also highlights the importance for the integration of AI to ensure a well-rounded model to ensure that all the different factors and signs are taken into account before giving advice to their users. The study also explores consumer spending patterns, the role of emotional intelligence in fintech design and the ethical implications of algorithmic nudging. As robo-advisors evolve into emotionally aware financial companions, the future of investing in Southeast Asia points toward a hybrid model, one where emotional understanding and data-driven decision-making merge to guide investors to wealth and wisdom.

Introduction

In a world where financial markets never sleep and investment platforms live in our pockets, the very act of investing has become more immediate, personal and psychological complex than ever before. The investor today is not only informed and digitally empowered but also engrossed in an environment whereby financial decisions are shaped by a perpetual flow of information, real-time feedback and elegantly engineered user interfaces. From push notifications to portfolio graphs, every design element has an influence on how investors interpret risk, respond to changes in the market and act on their tendencies.

The concept of behavioural finance, a challenger of the assumption of rational economic actors, has revealed the deep psychology behind investor behaviour. Against this backdrop, artificial intelligence has emerged not just as a tool for automation, but as a partner in decision-making, capable of recognising behavioural patterns and guiding investors toward better outcomes. Robo-advisors, once valued for cost and convenience, are now evolving into intelligent platforms powered by behavioural AI: systems that detect emotional cues, anticipate biases and deliver timely, personalised nudges. In Southeast Asia, where fintech adoption and digital inclusion are accelerating, these developments raise a critical question: Can behavioural AI embedded in robo-advisors meaningfully improve investment decision-making by addressing emotional and cognitive biases? This paper explores that question through theory, regional case studies and empirical insights, examining how AI-driven tools are reshaping not just how people invest, but how they experience investing itself.

Literature Review

The intersection between human behaviour and financial decision-making is something deeply rooted within the documentation of academic literature. In the pioneering work of Kahneman and Tversky (1979), it was found that behavioural finance poses questions to the assumptions of investor rationality while underpinning the classic theory of economics. Rather, it presents the investor as a psychologically complex agent who is not only logically driven but also emotionally and cognitively biased. In parallel, literature on algorithmic advisory platforms has expanded from cost-reduction and efficiency (Sironi, 2016) to include personalised, AI-driven tools designed to influence investor behaviour in real time. Robo-advisors are fintech financial advisors that utilise artificial intelligence data processing (Bhatia et al., 2020; Tao et al., 2021) to give users investment advice with limited or no human intervention (Hodge et al., 2021; Tao et al., 2021).

Understanding the psychology behind investment decisions is essential for effective wealth management, particularly in an environment surrounded by volatility and uncertainty. Behavioural finance, as pioneered by Kahneman and Tversky (1979), identifies systematic deviations from rationality, primarily driven by cognitive biases. These biases help explain why investors often make suboptimal choices, even when provided with sufficient information. Investors experience the pain of loss more acutely than the joy of equivalent gains. This leads to holding on to losing stocks too long or giving away winning positions too quickly (Barberis & Huang, 2001). Herding typically refers to when an investor follows the crowd without conducting individual analysis. In investing, herding can often lead to bubbles or rapid sell-offs, as many investors buy and sell stocks because others are doing the same (Bikhchandani & Sharma, 2001). There is also recency bias to consider, where investors over-emphasise recent events when analysing investments, often extrapolating short-term trends into the future. This bias often results in trend-chasing behaviour, where short-term patterns are mistakenly assumed to be long-term signals (De Bondt & Thaler, 1985), leading to overconfidence. Collectivism, social norms and community influence remain strong, encouraging herding and the rapid spread of investment fads (Hofstede, 2001).

In Southeast Asia, consumer spending patterns are undergoing a dynamic shift, shaped by digitalisation, increased financial literacy, increased financial freedom and changing generational attitudes towards money management and investment. Millennials and Gen Z, who comprise a majority of the region’s population, tend to prioritise convenience, personalisation and digital-first experiences. These attitudes are due to a combination of factors including the influence of technology, a fast-paced lifestyle, the cognitive ease it brings and the psychological desire for instant gratification. In a world where everything is available at our fingertips, convenience is a deal breaker and a highly valued commodity. Unlike previous generations that preferred the conventional methods of investment and saving, leaning towards conservative saving and gold based investment, younger generations are more open to equities, ETFs and digital investment platforms. This shift is particularly pronounced in economies like Singapore, Malaysia, Indonesia and the Philippines, where mobile-first behaviour dominates, especially after the introduction of online payment methods and digital wallets. Furthermore post pandemic consumer sentiment has shown a stronger preference for self-directed financial tools, with increased awareness of personal psychological triggers behind financial decisions.

AI based robo-advisors are increasingly leveraging these evolving patterns through advanced behavioural modelling. By integrating transactional data, demographic insights and psychographic profiles, AI algorithms can now detect emotional and cognitive biases such as overconfidence, loss aversion and herding behaviour. For instance, if a user tends to panic-sell during market dips, the robo-advisor can identify this trend and send nudges, such as educational prompts or rebalancing suggestions, based on behavioural finance frameworks.

There are multiple leading examples in Southeast Asia, including StashAway (Singapore), Syfe (Singapore) and GAX MD (Malaysia), where robo-advisors embed machine learning models to adapt in real time. These models are designed to evolve with user behaviour, learning from spending and investment triggers. Some tools now integrate Natural Language Processing (NLP), a field of artificial intelligence that focuses on enabling computers to understand and generate human language, to interpret investor sentiment through inputs or chatbot interactions, allowing hyper-personalised portfolio management. Along with that, predictive analytics tools are enabling robo-advisors to shift from reactive to proactive strategies, customising asset allocations before a user makes a bias-driven decision.

Moreover, the blend of AI automation and behavioural finance has allowed robo-advisors to categorise users more accurately, not just by income and age but rather by personality traits and risk tolerance that are inferred through a consumer’s financial behaviours. These AI tools reduce emotional-driven decision-making, acting as behavioural buffers by reminding users of long term goals and helping to mitigate herd behaviour during market crashes or hype cycles. This, in turn, allows for smarter goal-based investing, reducing the conflict between impulsive consumer spending and long-term wealth accumulation. As Southeast Asia continues to digitise, AI-enhanced robo-advisors are poised to become key instruments in mitigating emotional decision-making, fostering more resilient investor behaviours and allowing realistic goal setting.

How Robo-Advisors Use AI to Shape Behaviour

Robo-advisors are digital platforms that provide automated, AI driven financial planning and investment services, with minimal human intervention. They collect information on the user such as financial backing, investment goals and risk appetite and then create personalised investment portfolios through various different algorithms. Most of the platforms prioritise and advertise low fees, easy access and inclusivity. These robots are making wealth management available to the wider public, which is a promising shift from when wealth management was mainly available to affluent customers.

The Stages of Robo-Advisors

i. Web or mobile apps are set up for account management through the input of financial data etc.

ii. Data collection and risk profiling occurs through questions to assess the user’s risk tolerance

iii. Algorithms generate investment plans, often using ETFs

iv. Executes re-investment, rebalancing and sometime tax optimisation, often without human intervention

v. Monitors performance and ensures regulatory compliance

We will now explore how AI powered robo-advisors work, specifically by looking at three distinct but related areas:

- Machine Learning: This concept allows robo-advisors to constantly refine predictions and investment choices by analysing vast amounts of market data and user activity. Machine learning models also recognise portfolio drifts, predict asset returns using old data and optimise consumer portfolios in response to the changing market.

- Natural Language Processing: NLP enables conversational interfaces, where users can interact with chatbots to ask for advice, clarify investment options or set new goals. This helps novice investors by facilitating jargon-free communication.

- Algorithm Risk Profiling: AI models assess risk by evaluating questionnaire responses and transaction patterns. This ensures that the portfolio matches how much the consumers want to risk and adapt to changing circumstances, increasing both investor trust and regulatory compliance.

Furthermore, there exists a branch of behavioural AI comprised of the following:

- Personalisation: AI checks transaction history, saving patterns and financial goals to recommend investment paths. Essentially no two users will receive the same investment paths or “nudges”.

- Prediction: By processing real time and historical data, predictive models anticipate actions or events and recommend possible strategies to tackle them before they become issues.

- Nudging: Personalised communications supported by behavioural economics and AI subtly prompt users to take actions, like increasing savings or rebalancing portfolios, without any compulsion. Some nudges have demonstrated increased client engagement and better financial outcomes.

Case Studies: Behavioural AI Platforms in Southeast Asia

This section looks at how three leading digital investment platforms in Southeast Asia (Endowus, Syfe and Ajaib) are reshaping the way people invest. By blending AI with insights from behavioural finance, these platforms are helping investors make smarter, more informed choices for the long term.

Endowus: Rewiring investment behaviours through AI

A prominent Singapore-based digital wealth management advisor, Endowus offers holistic, evidence-based investment guidance. Many other robo-advisors focus on short-term return approaches while Endowus has a different approach. Endowus adopts a “Strategic Passive Asset Allocation” approach. This involves portfolio recommendations centred around global diversifications, passive investing and long-term approaches. Endowus’ architecture mainly involves investors inputting financial goals, risk appetite, time horizon and other factors through digital interfaces. The company’s algorithms then interpret these inputs, recommend diversified portfolios and automate regular rebalancing to maintain optimal risk-return balance. Endowus’ system allows Singaporeans to invest not just cash but also CPF (retirement) and SRS (tax-advantaged) funds in curated global portfolios.

One of the main tactics Endowus uses is the use of AI driven, evidence-based plans to counter common investment propaganda. Cognitive biases such as loss aversion, recency bias and confirmation bias often lead investors to make emotionally-driven decisions, like panic-selling during downturns or chasing recent winners. The platform’s rules-based balancing algorithm helps take the emotion out of investing, buying undervalued assets and selling overvalued assets without any human bias intervening. Through articles, reports and direct client communication, Endowus constantly emphasises the dangers of cognitive short cuts like “market timing” and encourages evidence based long-term decision-making.

Despite 61% of Singapore investors citing retirement as a primary goal, less than half make investment decisions that help facilitate these goals. The company nudges clients toward more consistent, goal-focused behaviour. Trust is paramount in a digital and regulatory landscape, and Endowus leverages AI for transparent advice while maintaining compliance with Singapore’s strict MAS standards. Automated portfolio management and educational nudges particularly benefit new or less experienced investors, reducing common mistakes and lowering barriers to wealth creation in a region marked by diverse digital literacy levels.

Syfe: Embedding emotional intelligence into robo-advisors

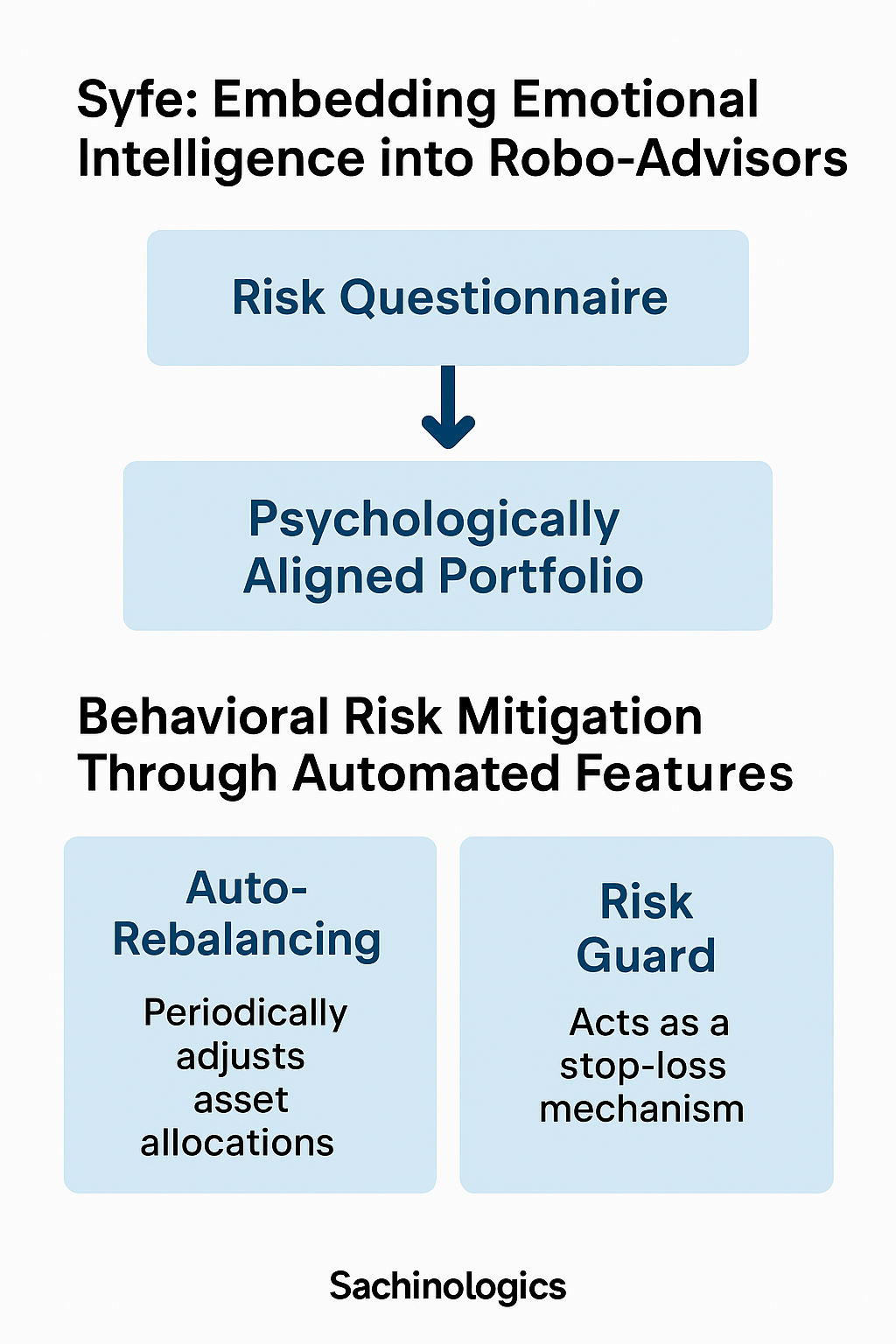

Syfe is one of Singapore’s leading robo-advisors, which exemplifies how behavioural profiling and emotionally-aware design can shape investor decision-making. The main feature of its onboarding process is a “Risk Questionnaire” which does more than assess financial capacity – it also subtly highlights the behavioural finance principles. By being able to gauge user reactions to hypothetical market events, Syfe classifies and categorises emotional resilience and risk tolerance, which creates psychologically aligned portfolios.

Two notable features of Syfe are “Auto-Rebalancing” and “Risk Guard” which serve as behavioural stabilisers. The auto-rebalancing prevents emotional interference by periodically adjusting asset allocations, ensuring discipline amid volatility. Risk-guard, available in REIT+ portfolios, acts as a stop-loss mechanism, shielding users from extreme downside and reducing panic-based withdrawals. Syfe’s user interface and in-app messaging are deliberately designed to reduce panic-selling during market downturns and collapses. Instead of triggering alerts that cause fear, the platform will send reassuring updates with long-term context. This subtle behavioural “nudge” supports rational decision-making even during crises.

Syfe could evolve by integrating real time sentiment data to increase accuracy, possibly by voice or biometric data. This would also allow the platform to respond more proactively to investor anxiety. As the retail investors in Southeast Asia continue to grow more tech-savvy, Syfe’s emotionally-aware design could serve as a foundation for combining artificial intelligence, user experience and behavioural finance to promote smarter investing.

Ajaib: Advancing financial inclusion

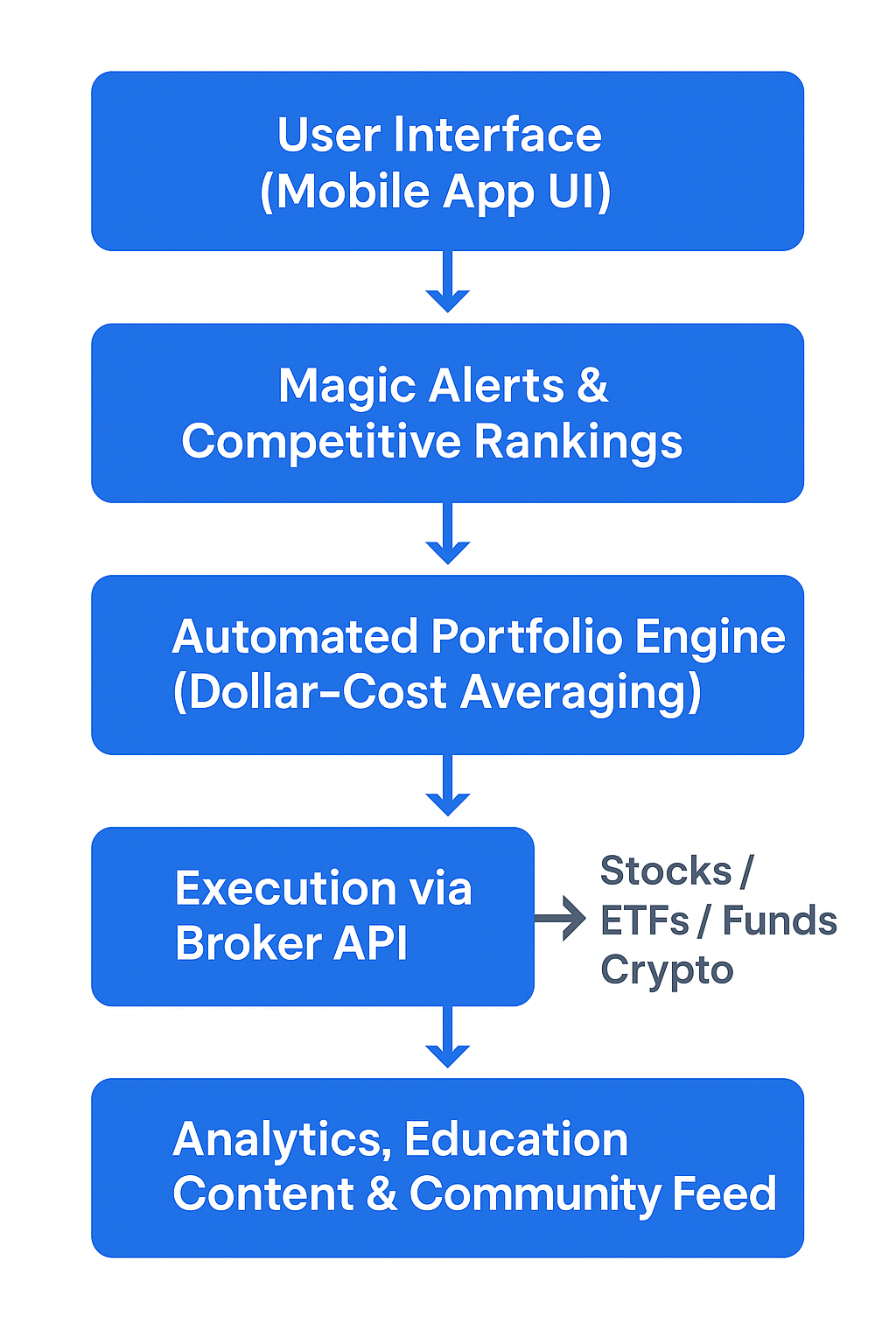

Founded in 2019 and headquartered in Jakarta, Ajaib is a mobile-first investment platform that provides access to stock, mutual funds and crypto investing in Indonesia. It makes use of smart alerts and competitive ranking to help users make informed decisions by summarising fundamentals and news highlights. Ajaib also uses cloud-based infrastructure like Google Cloud to keep scalability and security intact.

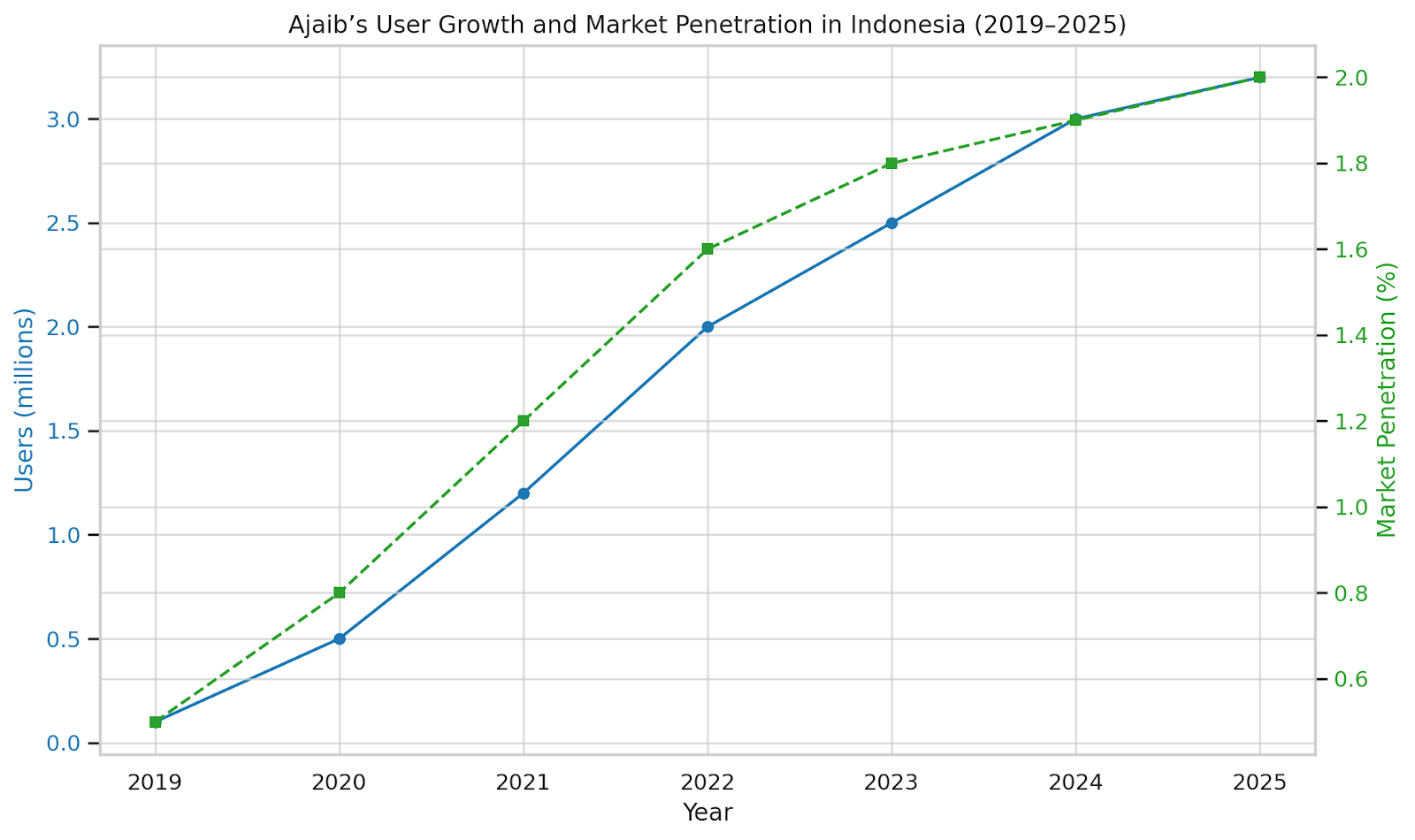

Serving more than three billion users, Aijab stands as the third-largest brokerage by trade count in the country. It achieved a unicorn status with valuations exceeding USD $1 billion after raising rounds led by Y Combinator, DST Global, Horizons Ventures, Alpha JWC Ventures and others. It has undoubtedly played a transformative role in advancing financial inclusion within the historically underpenetrated market of Indonesia, in which only less than 2% of the population actively invests in capital markets (International Adviser, 2021; Vizologi, 2023). Through elimination of entry barriers and leveraging a mobile approach, this company was able to quickly gain attraction among consumers, specifically first-time investors. After its initial launch in 2021, it reached over 1 million users shortly after. This was also a notable achievement through its entrance into the Times Square’s digital billboard as a symbol of its momentum and impact (Insignia Review, 2021).

Through its positioning as the fastest-growing investment platform in Indonesia, Ajaib strategically targets millennial and Gen-Z demographics, areas historically underserved by formal financial institutions (Highperformr, 2023; TechCrunch, 2021). The generational focus, intuitive design and education-driven features made Ajaib the cornerstone of Indonesia’s digital financial transformation.

Evaluating the Effectiveness

Advisors such as StashAway and Syfe often mention their solid client engagement and retention rates along with multiple apps used during periods of financial and market volatility. In 2022, Syfe’s internal data claimed a 70% retention rate for clients in 2022 as global markets decreased due to consumer fear of inflation and financial volatility (Syfe, 2022). Upon recent interviews, Syfe credited their success to targeting emotional, personalised notifications and in-app educational features. These features are intended to remind and encourage users to stay invested and to avoid panic-selling, a behavioural bias called loss aversion. Through identifying these issues, robo-advisors ensure that client retention by assistance, as well as adherence to investment plans, are met.

In the area of analysing consumer behaviour, several platforms have demonstrated that the use of AI in these programs can reduce irrational investor behaviour. Such is the case for StashAway, which uses its ERAA (Economic Regime Based Asset Allocation) to personalise portfolios based on varying past user risk preference and economic regime. During the COVID-19 downturn in the markets, users that received automated reassurance were 32% less likely to liquidate their portfolios compared to users receiving no messaging (StashAway, 2021). This data suggests that emotional autonomous messaging is as important as financial advice.

Although these platforms seem effective, some question the psychological implications brought on by robo-advisors. Do users experience greater confidence in their decisions or will users risk becoming dependent on AI? A study conducted by the Journal Behavioural Finance surveyed 730 investors across Singapore and Malaysia, with 61% of surveyed investors reporting feeling more confident in finance after using a robo-advisor, with 28% admitting that they did not comprehend how the algorithm made decisions (Tan and Goh, 2023). A survey conducted by the CFA Institute also saw a similar response. A member survey by the CFA saw over 70% of participants report that the use of robo-advisors has a positive impact on users, highlighting its use of algorithmic decision-making, improved access and reduced costs (CFA Institute, 2016).

Global Landscape vs. Southeast Asian Adoption

Globally, the robo-advisory market is experiencing a great surge in user numbers. In 2024, the market was valued at $8.39 billion and is predicted to cross $69 billion by 2032. This growth is caused by digitalisation, shifting consumer preferences for low-cost, more inclusive investing and heightened trust in algorithmic advice. In Southeast Asia, use is accelerating but has different characteristics. Singapore, for example, is a market with assets under management in robo-advisory, expected to reach $136.7 thousand in 2025 due to high financial literacy, established trust in digital banking and proactive regulatory frameworks.

The Future of Investing: Ethics and Emotionally-Intelligent Tools

As artificial intelligence becomes largely embedded within the bigger scheme of investments, it brings the world to a powerful promise which encompasses the optimisation of decision-making, reduction of human error and making wealth-building more accessible. On the contrary, this exact promise comes with a large responsibility: the fine line between empowerment and manipulation.

Empowerment arises when AI systems help provide access to more information, provide investment education, enhance financial literacy and provide better risk assessments. Regulators like SEBI in India employ AI to protect investors from fraud and market manipulation, improving market trust and investor confidence. On the other hand, through algorithmic nudges, robo-advisors are able to subtly guide the investor’s behaviour. These nudges stem from behavioural economics (Thaler & Sunstein, 2008) and are designed to counteract impulsivity, reinforce rational investor habits and promote long-term thinking. Yet, as they continue to develop, they also pose several ethical challenges.

The main ethical challenges that are prevalent are:

1. If investors are nudged without complete awareness or understanding of influential tactics, there is a risk of undermining individual agency.

2. If the logic or intent behind AI-powered nudges is not clear, it becomes difficult for investors to make fully-informed choices.

3. If nudges are based on poorly analysed data or driven by biased training, discrimination can be reinforced.

4. If AI nudging is designed to maximise platform engagement or profits, not investor welfare, then ethical responsibility is placed upon system designers and regulators.

As Southeast Asia enters a new era of digital transformation and financial inclusion, the next development in personal finance lies in the merging of emotional intelligence and AI-driven automation. While the current robo-advisors focus more on optimising returns and risks through data-driven insights, the wealth tools of the future will technologically evolve into emotionally-intelligent companions and advisors who understand both the market and the mind.

One major leap forward will come from the integration of emotional-recognition technologies into wearable devices and voice-activated financial platforms. As smartwatches and mobile devices increasingly track biometric signals like heart rate, speech tone or facial expressions, future robo-advisors could detect emotional states like anxiety, impulsiveness and overconfidence. A user showing signs of stress before a large withdrawal could be gently guided through calming content, reminders of long-term goals or insights into past financial decisions. This represents a shift from reactive to pre-emptive advising, where the system intervenes before a poor decision is made, based not just on financial data but on human emotion. This will be an integral and important development in the field of behavioural finance, AI automation, financial literacy and awareness.

Along with this development, AI-driven coaching tools may be embedded within the robo-advisors platforms, teaching users to develop their own financial awareness. Instead of simply being told what to invest in or what the risks and benefits are, they can engage in gamified learning models which can help them to recognise emotional triggers, set better habits and reflect on their financial choices. These tools could be merged with personal development and portfolio management which could foster a generation of emotionally-resilient investors who not only build wealth but also wisdom related to financial literacy. Importantly, for emotionally-intelligent systems to be truly impactful in Southeast Asia, they must be culturally responsive. The region is not monolithic – investment behaviour in Singapore is influenced by different norms, values and family dynamics compared to Indonesia, Vietnam or the Philippines. For instance, more collectivist cultures would prioritise family consensus over their individual desire for risk which can also be influenced more strongly by community sentiment and social proof. Emotionally-aware AI tools of the future must go beyond language translation; they must also incorporate cultural patterns of decision-making, familial obligation, risk tolerance and even local religious or ethical frameworks. Customisation and personalisation of these factors will be essential for trust and adoption in diverse markets.

At the same time, AI systems will continue to adapt to changing consumer behaviour. As Gen Z and the rising Alpha generation grow up with embedded financial technologies and hyper-personalised content feeds, their expectations from financial tools will shift towards on-demand, intuitive and even emotionally-responsive interfaces. Nowadays, spending patterns are becoming increasingly more fluid, increasing the need for AI models to evolve with these constantly shifting landscapes to be capable of predicting not only “what” users might do, but “why” they are likely to act a certain way, mainly based on emotional and cognitive patterns that are unique to their digital upbringing.

Looking ahead, one huge development will lie in integrating behavioural education into financial platforms themselves. Future robo-advisors may not be built solely to guide decisions, but to also teach users how to think long term, navigate uncertainty and build psychological resilience. Much like health apps promote a holistic wellness mindset, emotionally-intelligent investing tools could promote a long-term wealth mindset, emphasising patience, discipline and adaptability over quick gains or speculative hype, balancing modern ideals with conventional thoughts and habits to ensure complete financial understanding and awareness.

The long-term vision is more profound: an emotionally-aware investing world where financial tools are as attuned to human psychology as they are to the market metrics and numerical data. In this world, technology doesn’t replace human judgement, it enhances it. By aligning emotional understanding with financial decision-making, such tools help to close the gap between what people intend and wish to do with their income and money and what they actually do, thereby reducing regret and improving long-term outcomes. These tools will not only help users to generate wealth but to grow their financial wisdom, creating a lasting impact for the current and future generations in Southeast Asia.

Conclusion: Rational Returns in an Irrational World

Robo-advisors are changing the way people invest in Southeast Asia by using artificial intelligence to understand not just market trends, but investor behaviour. These platforms go beyond simple automation. By applying the core principles of behavioural finance, they help users manage emotional reactions like fear, overconfidence and herd behaviour. Through personalised nudges, risk assessments and data-driven recommendations, robo-advisors support investors in staying consistent with their long-term goals, bettering their financial literacy, wisdom and wealth through their investments and expenditure.

This paper explored how platforms such as Endowus, Syfe and Ajaib are making financial tools more accessible and emotionally-intelligent. Their success shows that AI can reduce the impact of impulsive decision-making, especially in a region where digital habits, cultural values and financial literacy levels are rapidly evolving. While the question remains whether AI understands investors better than investors understand themselves, this analysis shows it can certainly identify and mitigate behavioural patterns that investors often miss. By tracking patterns that investors might not even notice, like panic-selling during market dips or chasing short-term gains, AI can offer timely reminders, education and guidance that improve financial outcomes. However, this also raises concerns about over-reliance, data privacy and transparency. The challenge is to establish a balance and a boundary while using these tools to ensure they empower rather than replace human judgement.

In Southeast Asia’s diverse and fast-changing environment, behavioural AI is not just a tool – it may become a financial guide for the emotionally driven investor. As these platforms continue to evolve, their true impact will not only be measured in returns, but in how confidently and wisely people make decisions about their financial futures.

Bibliography

Adwen Publications (n.d.) AI-Driven Innovations in Financial Planning. International Journal of Management Studies and Research (IJOMSR). Retrieved from: https://www.adwenpub.com/index.php/ijomsr/article/view/539

Barberis, N. & Huang, M. (2001) Mental accounting, loss aversion, and individual stock returns. The Journal of Finance (56:4) pp. 1247–1292. Retrieved from: https://doi.org/10.1111/0022-1082.00367

Barberis, N. & Thaler, R. (2003) ‘A survey of behavioral finance’ in Constantinides, G., Harris, M. & Stulz, R. Handbook of the Economics of Finance Vol. 1B (Elsevier) pp. 1053–1128. Retrieved from: https://doi.org/10.1016/S1574-0102(03)01027-6

Bhatia, M., Jain, D. & Meena, R. (2020) Artificial intelligence and robo-advisors in fintech: A review. International Journal of Management, IT & Engineering (10:1) pp. 124–133. Retrieved from: http://www.ijmra.us/project%20doc/2020/IJMIE_JANUARY2020/IJMRA-18243.pdf

Bikhchandani, S. & Sharma, S. (2001) Herd behavior in financial markets. IMF Staff Papers. (47:3) pp. 279–310. Retrieved from: https://doi.org/10.5089/9781451972031.024

Chen, W., Dey, D. & Lee, W. (2020) Fintech platforms and the future of investing in emerging markets. Journal of Emerging Financial Markets (12:2) pp. 87–101. Retrieved from: https://doi.org/10.1177/0972652720935554

Corporate Finance Institute (n.d.) Robo-Advisors. Retrieved from: https://corporatefinanceinstitute.com/resources/wealth-management/robo-advisors/

CFA Institute (2016) CFA Institute Survey Indicates Substantial Impact of Robo-Advisers on Investment Management. Retrieved from: https://www.cfainstitute.org/about/press-room/2016/cfa-institute-survey-indicates-substantial-impact-of-robo-advisers-on-investment-management

DBS Bank (n.d.) Artificial Intelligence and Machine Learning. Retrieved from: https://www.dbs.com/artificial-intelligence-machine-learning/index.html

De Bondt, W.F.M. & Thaler, R.H. (1985) Does the stock market overreact? The Journal of Finance (40:3) pp. 793–805. Retrieved from: https://doi.org/10.1111/j.1540-6261.1985.tb05004.x

Fidelity (n.d.) What is a Robo-Advisor? Retrieved from: https://www.fidelity.com/learning-center/smart-money/what-is-a-robo-advisor

Financial Planning Association (2024) Customer trust and satisfaction in robo-adviser technology. Journal of Financial Planning. Retrieved from: https://www.financialplanningassociation.org/learning/publications/journal/AUG24-customer-trust-and-satisfaction-robo-adviser-technology-OPEN

Fintech News Singapore (2024) 10 Robo-Advisors in Singapore for Digital Investing & Financial Planning. Retrieved from: https://fintechnews.sg/94670/wealthtech/10-robo-advisors-singapore-digital-investing-financial-planning/

Grand View Research (n.d.) Robo-Advisory Market Report. Retrieved from: https://www.grandviewresearch.com/industry-analysis/robo-advisory-market-report

HashStudioz (n.d.) How AI Is Transforming Financial Planning Through Robo-Advisors. Retrieved from: https://www.hashstudioz.com/blog/how-ai-is-transforming-financial-planning-through-robo-advisors/

Highperformr (2023) How Ajaib captured Indonesia’s Gen Z investors. Retrieved from: https://www.highperformr.com/ajaib-genz-indonesia

Hodge, F., Rajgopal, S. & Shevlin, T. (2021) Robo-advisors and investor decision making: Evidence from digital advice platforms. Journal of Financial Economics (139:2) pp. 393–414. Retrieved from: https://doi.org/10.1016/j.jfineco.2020.08.005

Hofstede, G. (2001) Culture’s consequences: Comparing values, behaviors, institutions and organizations across nations, 2nd ed (SAGE Publications).

Hubbis (2023) Transforming Asia’s Private Wealth Management Landscape with Fintech and AI. Retrieved from: https://www.hubbis.com/article/transforming-asia-s-private-wealth-management-landscape-with-fintech-and-ai

IJRASET (n.d.) Role of Artificial Intelligence in SEBI Protection of Investors. Retrieved from: https://www.ijraset.com/best-journal/role-of-artificial-intelligence-in-sebi-protection-of-investors

Insignia Review (2021) Ajaib enters Times Square: The rise of Indonesian fintech. Retrieved from: https://review.insignia.vc/ajaib-times-square-fintech/

International Adviser (2021) Indonesia’s Ajaib aims to boost investor inclusion. Retrieved from: https://international-adviser.com/indonesias-ajaib-aims-to-boost-investor-inclusion/

Kahneman, D. & Tversky, A. (1979) Prospect theory: An analysis of decision under risk. Econometrica (47:2) pp. 263–291. Retrieved from: https://doi.org/10.2307/1914185

More Than Digital (n.d.) The State of WealthTech in Southeast Asia. Retrieved from: https://morethandigital.info/en/the-state-of-wealthtech-in-southeast-asia/

Morgan Stanley (n.d.) What Is a Robo-Advisor? Retrieved from: https://www.morganstanley.com/atwork/employees/learning-center/articles/what-is-robo-advisor

National Center for Biotechnology Information (2020) Digital Finance and the Future of Investing. PubMed Central (PMC). Retrieved from: https://pmc.ncbi.nlm.nih.gov/articles/PMC7508018/

Roongruangsee, R. & Patterson, P. (2024) Modelling client adoption of robo‑advisors in Thailand: The impact of trust and situational factors. Journal of Financial Services Marketing. Retrieved from: https://doi.org/10.1080/13602381.2024.2405696

Singapore Management University (SMU) Centre for Consciousness and Cognition (CCX) (n.d.) Ethics of AI Nudges: How AI Influences Decision-Making. Academic Mind (12:1). Retrieved from: https://ccx.smu.edu.sg/ami/issues/volume-12-issue-1/parting-shot/ethics-ai-nudges-how-ai-influences-decision-making

Sironi, P. (2016) FinTech innovation: From robo-advisors to goal-based investing and gamification (Wiley). Retrieved from: https://doi.org/10.1002/9781119226885

StashAway (2023) How to use AI for investment: StashAway’s ERAA strategy. Retrieved from: https://www.stashaway.sg/r/how-to-use-ai-for-investment

StashAway (2025) Best Robo‑Advisors in Singapore (2025). Retrieved from: https://www.stashaway.sg/r/best-robo-advisors-singapore

StashAway (2025) AI-Driven investing: How to use artificial intelligence in investment. Retrieved from: https://www.stashaway.sg/r/how-to-use-ai-for-investment

Statista (2025) Robo-Advisors – Singapore. Retrieved from: https://www.statista.com/outlook/fmo/wealth-management/digital-investment/robo-advisors/singapore

Syfe (2021) Downside risk explained: Why we use it and what it means. Retrieved from: https://www.syfe.com/magazine/downside-risk-explained/

Syfe (2022) How to protect your portfolio when markets fall. Retrieved from: https://www.syfe.com/magazine/how-to-protect-your-portfolio-when-markets-fall/

Syfe (2022) Why rebalancing is the quiet superpower of long-term investors. Retrieved from: https://www.syfe.com/magazine/why-rebalancing-is-the-quiet-superpower-of-long-term-investors/

Tan, J.K. & Lim, E. (2024) Do robo-advisors improve behavioral financial outcomes? A mini-review. Frontiers in Behavioral Economics (1:1489159). Retrieved from: https://www.frontiersin.org/articles/10.3389/frbhe.2024.1489159/full

Tao, R., Wang, Y. & Li, J. (2021) Robo-advisors and AI in wealth management: A review of recent advances. Financial Innovation (7:41). Retrieved from: https://doi.org/10.1186/s40854-021-00251-3

TechCrunch (2021) Indonesia’s Ajaib becomes unicorn with $153M funding round. Retrieved from: https://techcrunch.com/2021/10/04/ajaib-unicorn-funding/

Thaler, R.H. & Sunstein, C.R. (2008) Nudge: Improving decisions about health, wealth, and happiness (Yale University Press).

Vizologi (2023) Ajaib business model | How Ajaib makes money. Retrieved from: https://vizologi.com/business-model-canvas/ajaib/

Yi, T.Z., Rom, N.A.M., Hassan, N.M., Samsurijan, M.S. & Ebekozien, A. (2023) The adoption of robo‑advisory among millennials in the 21st century: Trust, usability and knowledge perception. Sustainability (15:7). Retrieved from: https://doi.org/10.3390/su15076016

{kind=link}