Abstract

This research paper focuses on the various policies used by the International Monetary Fund (IMF) in Southeast Asia (SEA) and the Middle East and North Africa (MENA) since the 1990s. By analysing the policies introduced in the regions, the research evaluates that the policies and methods of the IMF have frequently failed to achieve their aims due to mistakes involving the policies of austerity, fiscal consolidation, currency devaluation and pegging removal. It emphasises that the critical errors made by the organisation led to regions suffering economically, politically or socially. The paper elaborates that the IMF often failed to provide necessary support due to a lack of understanding of the specific circumstances. The paper criticizes the IMF by exploring the power inequality within the organisation. It argues that despite multiple issues that arose from the change in the policies suggested by the IMF, it should not be gotten rid of. Instead, the organisation should focus on preventing the recurrence of past mistakes, such as the use of the “one-size-fits-all” approach and rapid decision-making without consultation with regional leaders. Second, it should consider the long-term sustainability of the decision to promote austerity having seen the policy’s impacts of currency devaluation, overdependence and strained political institutions.

1. Introduction

The International Monetary Fund (IMF) is one of the most significant international financial institutions in the modern global economy. Established in 1944 during the Bretton Woods Conference, the IMF was created to promote global economic cooperation, ensure financial stability and encourage international trade. At its core, the IMF’s mission is to promote sustainable economic growth and reduce poverty across all member countries, whether developed or developing. Today, the IMF comprises 191 member nations and serves as a forum where governments can collaborate to prevent financial crises, mitigate economic shocks and promote development. The IMF provides two primary services: financial assistance and policy advice. When a member country faces a balance of payments crisis, meaning it struggles to meet international payment obligations regarding debt that financed a budget deficit, the IMF can extend loans to stabilise its economy. These loans often come with policy recommendations aimed at reforming the country’s economic structure and restoring fiscal stability. Many such policies can be characterised as promoting austerity or reducing government deficits through decreasing public spending or increasing tax revenue. Beyond lending, the IMF also provides technical assistance and training to governments, enabling them to enhance fiscal management, strengthen financial institutions and establish sustainable economic frameworks. Importantly, the IMF is not only relevant to struggling or developing countries, but also to those that are more stable and developed. Wealthier, more advanced economies also benefit from its oversight and policy guidance. By conducting regular economic surveillance, publishing analytical reports and offering macroeconomic advice, the IMF influences global financial governance. In this sense, the IMF plays a dual role: supporting vulnerable economies in times of crisis and maintaining stability across the international financial system. However, while its mandate is universal, the IMF’s actions and decisions have frequently drawn criticism, especially regarding their fairness and impact on different regions of the world.

While the IMF’s mission is global, its involvement in specific regions has sometimes led to controversy. In the Middle East, countries such as Kuwait, Egypt and Jordan have experienced both benefits and challenges from IMF engagement. Egypt, for instance, received substantial loans in exchange for implementing austerity measures, such as subsidy cuts and tax reforms. While these reforms were designed to stabilise the economy, they typically placed disproportionate pressure on lower-income citizens, sparking unrest and skepticism about whether the IMF’s approach sufficiently accounted for local sociopolitical contexts. Similarly, Jordan saw significant public backlash when IMF-imposed austerity measures increased fuel and food prices, resulting in protests that highlighted tensions between economic reform and social stability. In Kuwait, although a wealthy nation, IMF involvement is primarily centred on policy advice regarding diversification away from oil dependency; however, such recommendations have not always aligned with domestic political priorities. In Southeast Asia, particularly during the 1997 Asian Financial Crisis, IMF interventions in countries such as Indonesia and Thailand were considered heavy-handed, enforcing structural reforms and liberalisation policies that arguably deepened economic hardship in the short term. These cases illustrate recurring issues: while IMF support can stabilise economies, the conditions attached often provoke domestic resistance and highlight a mismatch between global prescriptions and local realities.

A recurring criticism of the IMF is that, despite its global mission, it operates with an inherent Western bias. This stems largely from its governance structure, where voting power is determined by financial contributions, giving advanced economies, especially the United States and European nations, considerable influence. As a result, developing countries regularly perceive IMF recommendations as reflecting Western economic ideologies, prioritising liberalisation, privatisation and fiscal austerity in ways that may not align with their unique needs. This perception of bias is reinforced by the historical dominance of Western-trained economists within the institution, whose frameworks and assumptions frequently stem from neoliberal economic traditions. While the IMF does not explicitly discriminate, its policy prescriptions can reflect a “one-size-fits-all” approach rooted in Western models of economic governance. For example, imposing rapid market liberalisation in economies with weak institutions has sometimes led to social dislocation and political instability. Critics argue that this subconscious bias undermines the IMF’s credibility as a truly global institution. It risks alienating developing nations, many of which view the IMF not as a neutral arbiter, but as a mechanism for extending Western economic influence. Addressing this challenge requires more inclusive decision-making and greater sensitivity to regional contexts.

To understand the IMF’s current role and challenges, it is important to place it within its historical context. Created in the aftermath of the Second World War, the IMF was designed to prevent the kind of financial instability that had contributed to the Great Depression and subsequent global conflict. Initially, its focus was on maintaining fixed exchange rates under the Bretton Woods system, but following the system’s collapse in the 1970s, the IMF evolved into a crisis lender for countries facing balance of payments difficulties.

Throughout the 1980s and 1990s, the IMF became particularly active in Latin America, Africa and Asia, promoting structural adjustment programmes that emphasised austerity, privatisation and economic liberalisation. While these programmes aimed to restore growth, their social and political consequences often revealed the limits of such prescriptions. In economic theory, this can be explained through the idea of diminishing returns: the more the same policy approach is applied across diverse contexts, the less effective it becomes. For instance, while liberalisation might initially bring efficiency gains, its continued application without adaptation to local conditions may yield smaller benefits or even harm. This historical pattern suggests that the IMF’s greatest challenge lies not in its mission, but in recalibrating its methods to avoid the diminishing returns of uniform, Western-centric strategies.

2. Global Overview

Since the 1990s, the IMF has played an immense role in the relief of economic shocks as a result of commodity market disruptions globally. Although the IMF’s integration policies initiated the movement towards globalisation and trade liberalisation, it has become apparent that these policies have become increasingly counterproductive, resulting in diminishing returns within the global market. Drawing on the works of Woods (2024), the IMF greatly encouraged codependency within nations post-Cold War. Furthermore, they illustrate the economic crises faced by underdeveloped countries amidst the Russia-Ukraine war, as highly dependent countries found their economies lacking essential commodities due to the trade sanctions. Countries immensely impacted included developing economies such as Georgia, Armenia and Egypt, as they heavily relied on agricultural imports. This, therefore, poses the question: are these policies mutually beneficial to all participating countries?

In accordance with Lipscy and Lee (2019), “countries lacking political influence in the IMF face strong incentives to pursue self-insurance”. In a similar vein, this reiterates the claim that countries that are influential in the IMF’s decision-making process tend to receive more treatment in the event of a geopolitical shock.

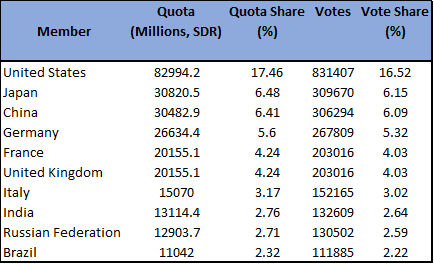

Figure 1: IMF Quota and Voting Share (Gray & Kingsley, 2023).

The table, presented above, shows the economies with the highest voting power within the IMF. It clearly shows the positive correlation between the voting power and quota allocated by the IMF. Hence, it depicts the IMF’s bias towards countries with leading nominal GDP. One may discern the massive issue evident in the approximately 77 countries that are categorised by the UN as developed or underdeveloped. This is rather problematic as these countries are the most vulnerable to supply shocks within the global economy.

Specifically examining economic crises within the previous three decades, the IMF lacks the ability to provide stable long-run aid to nations in desperate need of the funding. For instance, one may observe the Global Financial Crisis, which took place from 2008 to 2009. Examining the genesis of the crisis, the dependency on free trade proposed a negative spillover effect on countries that were not directly involved in the 2007 crash of the mortgage market, due to a negative demand shock within the US and UK. As a result of the IMF’s promotion of interdependence, fragile economies were faced with immense debt as well as austerity issues, which caused long-term economic disturbance. As reported by Novik (2020), the three foremost impacted economies were Estonia, Latvia and Ukraine, which were classified as the top 40–100 economies based on GDP. On the other side of the spectrum, leading economies such as the United States and Japan were found to be further down the ranking of impact, scoring at the 46th and 16th positions, respectively. Such an imbalance demonstrates that IMF integration policies result in less influential economies being overly susceptible to global shocks, whereas dominant nations remain relatively protected.

Delving deeper into the negative effects of interdependence on trading necessities in the economy, nations face the issue of being self-sufficient, relying heavily on imported goods. A striking realisation arose when data clearly emphasised the acknowledgement that only a singular country out of the 186 recognised by the United Nations is considered to be self-sufficient. This presents a significant challenge, as it is evident that globalisation has crippled the majority of nations that neglect the need to strengthen certain sectors domestically. In tandem with this, since the increased incentive of globalisation by the IMF, such as promoting export-led growth, subsequently stunts the growth of domestic economies, it presents a risk to sunset industries (declining industries) that cannot withstand the pressures of a global shock. In the annals of history, one may observe that rapidly there has been an uphill trend of strategically importing certain goods rather than producing said goods domestically. Not only is this of great hazard to the economy, but also to the working class, and as a country becomes more dependent on imports, labour will eventually be irrelevant to the economy. However, during the post-Cold War era, organisations such as the World Bank and the IMF have encouraged a global movement towards complete globalisation and liberal trade, creating a paradoxical effect.

A primary role of the IMF since the 1990s is to impose austerity measures as an ultimatum for financial aid. This system may appear rather controversial, as it obligates nations to have higher taxes and international tariffs, therefore decreasing their competitive edge in the international market. Reflecting on the remarks above, the IMF incentivises free trade but subsequently makes nations’ goods less desirable due to austerity measures. It could be suggested that the IMF’s policies may be rather contradictory, as the said policies have opposing consequences.

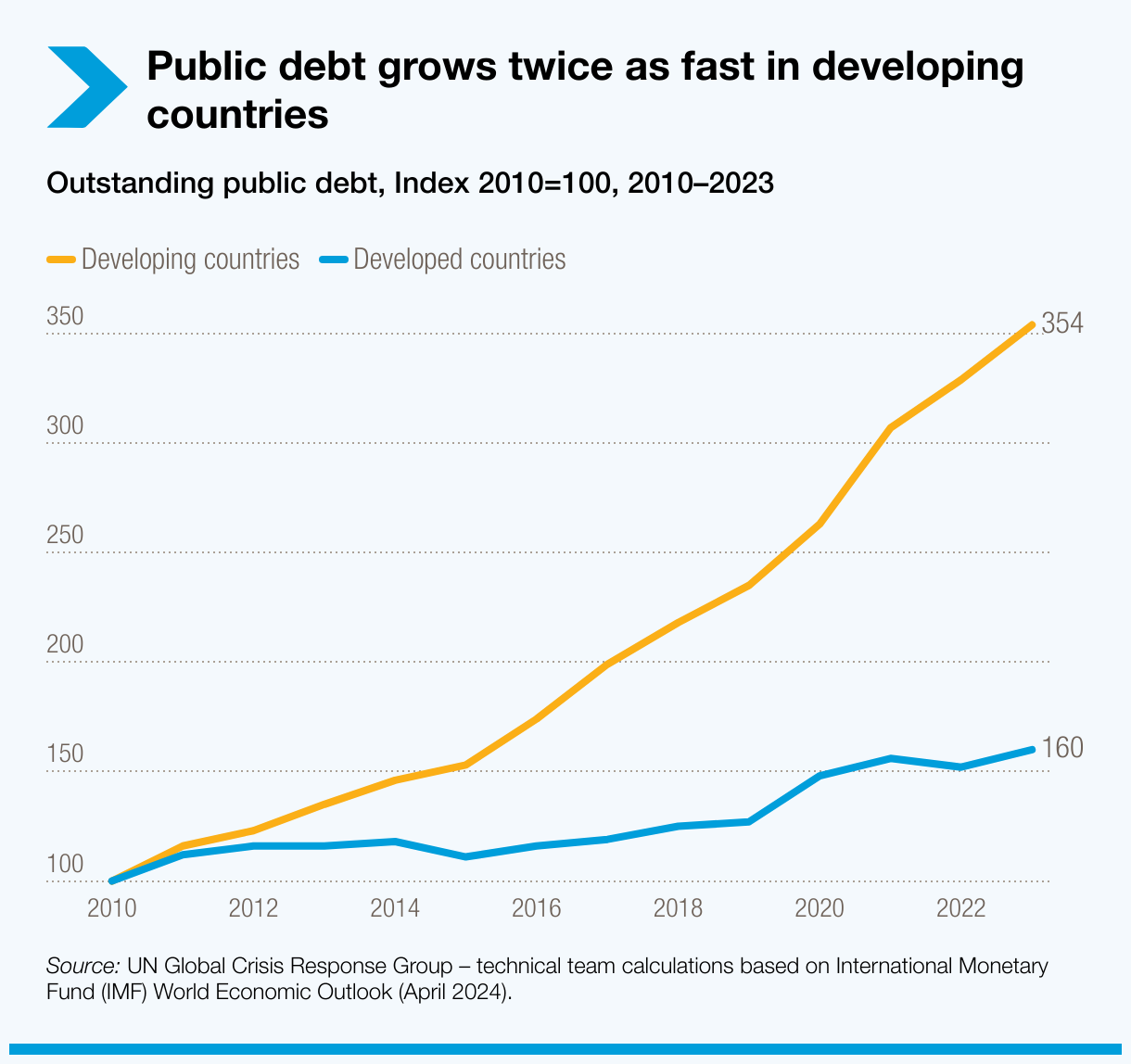

Figure 2: UN Trade and Development (UNCTAD, 2025).

As can be observed from the chart above, developing countries have been shown to have an increasing trend of higher debt compounding faster than that of developed countries, which emphasises their need for financial relief. This, therefore, reveals a challenge as countries that require immense debt aid are faced with austerity policies when receiving a loan; hence, loans received by these nations do not have a positive outcome but rather a tremendous drawback in the economy as they become internationally incompetent. A profound case of the self-defeating nature of austerity can be exemplified in the 2018 Argentina case. In 2018, due to the depreciation of the Argentinian peso by 50%, Argentina found its economy to be burdened with a $50 billion debt. Although the debt was covered by the IMF, it had implemented a 60% interest rate, which further pressured the economy. As this was the largest sovereign loan granted, diminishing returns were apparent. Inflation was said to rise by approximately 50% and unemployment by 40%. This triggered larger consequences for the economy, far more relevant to the debt. In the words of Castillo-Ponce & Lai (2020), “sadly, the crisis finds its root in the country’s prolonged severe economic mismanagement”, which emphasises how the austerity measures can be the primary contributing factor to negative externalities.

Although the IMF’s policies are shown to have diminishing returns towards developing economies, at times, their integration policies may prove to be beneficial. For example, their ability to provide a bailout may be suitable in the event of a substantially smaller debt. In a similar sense, as a contributing member of the IMF, a vast global market is available for participating countries to freely trade, which serves as an engine for economic growth, particularly for countries experiencing instability in their balance of trade. Furthermore, the IMF is not composed of a single voter who can veto any resolution while encouraging liberalisation. Nevertheless, the IMF’s integration policies tend to have drawbacks that far outweigh the merits, becoming a hazard of diminishing returns to fragile economies.

3. Economic Effects of IMF Policies in Southeast Asia

The IMF’s integration policies during the 1990s have had both positive and negative economic effects on Southeast Asian nations. Still, the negative consequences, notably austerity, financial vulnerability and reduced policy sovereignty, have now become more pronounced in the short to medium term for many member states, especially during crises such as the 1997 Asian Financial Crisis.

During the 1997 Asian Financial Crisis, a number of countries in Southeast Asia faced a collapse in currencies. The crisis occurred due to several industrial, financial and monetary government policies, as well as investment trends that were created. At the beginning of the crisis, the markets began to immediately react, causing multiple currency crashes and lowered economic growth. Many macroeconomic problems formed as a result of government policies that were used to promote export-led economic growth. Some of these concerns that arose were excessive short-term foreign debt, current account deficits, imbalanced capital inflows and outflows, and fixed exchange rates. To help the economies, the IMF bailed them out with packages totalling over $100 billion. The IMF provided the necessary financial assistance needed for the economies to recover; however, in exchange, it required countries to implement strict economic policies, often called “structural adjustment programmes”. These policies include sharp fiscal austerity, high-interest rates and liberalisation measures, which were enforced with the intended effect of restoring economic stability. These policies had an opposite effect and worsened recessions and deepened economic contractions in countries such as Indonesia and Thailand.

In Indonesia, IMF-mandated closures of insolvent banks and hiked interest rates – which peaked at around 70% – triggered severe credit crunches and a collapse in confidence. In contrast, Thailand experienced cuts in the budget for education and environmental protection spending. This caused the school dropout numbers to soar, with over 676,000 children dropping out between 1998 and 1999, and ecological budgets to be significantly cut. The IMF instructed economies in a recession to cut spending, a policy that deepened the economic slowdown. In contrast to Indonesia and Thailand, Malaysia refused the IMF’s prescriptions and implemented capital controls, which were initially derided but later proved comparatively successful in limiting economic damage. While in Cambodia, the IMF’s first arrangement during 1994-1997, just before the Asian Financial Crisis, under the Extended Credit Facility (ECF) fell short, causing economic growth projections to be stalled and disbursements to be mostly blocked due to governance and corruption concerns.

3.1 Indonesia

Before the Asian Financial Crisis, Indonesia experienced strong growth, averaging ~7% annually in the early 1990s. The country had low inflation due to robust macroeconomic policies, strong economic fundamentals and significant foreign investment. They also had a stable exchange rate, with the Indonesian rupiah (IDR) pegged to a managed float against the USD. Indonesia also attracted large foreign capital inflows, especially short-term loans, as a developing nation. Despite the economic fundamentals being more stable, there were multiple underlying vulnerabilities. Indonesia, during the period before the Asian Financial Crisis, had active crony capitalism due to the close ties between business elites and President Suharto’s government, which led to corruption and inefficiency. Alongside this, Indonesia had a weak banking system, which resulted in poor oversight and heavy borrowing in USD, creating high corporate foreign debt with over $80 billion by 1997, mostly unhedged. Additionally, there was a lack of transparency and regulation in the financial sector, which caused problems with maintaining trust in banking.

During the Asian Financial Crisis, Indonesia implemented the IMF’s policy to be able to recover its economy. As a result, the IMF provided a $43 billion bailout package; however, it came with strict conditions, including austerity measures that resulted in cutting public spending. Subsidies on food, fuel and electricity were reduced or removed, causing the prices of these goods to surge and increase drastically. Indonesia also needed to raise interest rates. This was intended to stabilise the currency, but it worsened the credit crunch from banks. This, in turn, increased unemployment and poverty rates, as well as violent protests and riots, especially in 1998. The protests were often held due to the widespread ideas of corruption, economic issues, including food shortages, and mass unemployment. These issues resulted in the prices of essentials skyrocketing, hurting the poor the most.

After the peak of the Asian Financial Crisis in 1998, Indonesia began a slow process of stabilisation, with help from international partners, internal reforms and a political transition. Indonesia began with the restructuring of the banking sector, with the Indonesian Bank Restructuring Agency (IBRA) recapitalising banks and closing over 60 insolvent banks. This caused bank governance and supervision to be strengthened and allowed for non-performing loans (NPLs) to be reduced from over 50% in 1998 to under 10% by 2003. Debt restructuring took place and allowed corporate debt to be renegotiated through the Jakarta Initiative Task Force (JITF). In 1998, the Paris Club came to a consensus and created an agreement for Indonesia, allowing it to reschedule its debts and spread its repayments by 18-20 years with a 3-5 year grace period. By then, Indonesia’s official debt was restructured, easing fiscal pressure and allowing it to focus on economic recovery and stabilisation. Macroeconomic management played a large role in settling inflation and allowing the economy to stabilise. With it, inflation was brought under control: from 77% in 1998 to single digits by 2001. Due to this, fiscal discipline was restored with the help of a new fiscal law in 2003, with the reduction of expenditure and promotion of more responsible spending, capping the deficit at 3% of GDP. Since then, the rupiah has stabilised at around 8,000-9,000 per USD. As for political reform, there was a transition to democracy post-Suharto, which increased policy credibility. It ended with decentralisation and giving more power to the local governments; however, the results were mixed.

3.2 Thailand

In July 1997, the Thai baht was devalued, acting as the main catalyst for and the beginning of the Asian Financial Crisis. The main cause of this sudden plunge in value was the government’s abandonment of its peg to the US dollar, which caused the Thai baht to float freely, leading to a significant decline in its value. This devaluation was triggered by speculative attacks on the currency and depleted foreign exchange reserves. Currency traders, including figures such as George Soros, bet against the baht, anticipating its devaluation. This massive sell-off of baht put downward pressure on the currency. To defend the baht’s peg to the dollar, the Bank of Thailand spent its foreign exchange reserves; however, these reserves were insufficient to withstand the speculative attack, causing them to deplete all of their foreign reserves. In the face of dwindling reserves and intense pressure, the Thai government decided to abandon the peg and allowed the baht to float freely. This resulted in an immediate and substantial drop in the value of the baht. However, due to the devaluation of the baht, similar currency crises were triggered in many other Asian countries, including Malaysia, the Philippines, Indonesia and South Korea. This led to widespread financial instability and economic downturns across the region. Additional contributing factors included excessive borrowing, risky lending practices and unsustainable economic growth policies within the region, which, when combined, contributed to the vulnerability of the economies to speculative attacks. It was then, after the decline of the Thai baht, that the International Monetary Fund (IMF) provided financial assistance and implemented economic reforms in the affected countries.

The IMF provided Thailand with a $17.2 billion bailout package, which was approved in August 1997. However, similar to Indonesia, the package came with stringent conditions centred on rapid liberalisation, financial-sector restructuring and fiscal austerity. This included a tight monetary policy, an increase in interest rates to stabilise the baht and attract inbound capital, and fiscal contraction, with cuts to public spending and an increase in value added tax (VAT) from 7% to 10%, aimed at generating a 1% of GDP public-sector surplus. Privatisation and closure or recapitalisation of numerous financial institutions were another condition that needed to be fulfilled. This, in turn, caused 56 finance companies to be permanently shut and led to banks being either nationalised or restructured. The IMF wished to lift capital controls to invite short-term speculative flows; however, the domestic financial system remained fragile.

Despite the IMF providing a base for Thailand to recover, the newly-introduced policies caused multiple negative effects. Due to the austerity measures in place, Thailand’s GDP fell sharply by 10.5% in 1998 alone, and the baht lost over half its value. This came as a result of the measures that exacerbated the recession in the short term by reducing domestic demand. High-interest rates and austerity measures hastened the insolvency of firms, especially small and medium-sized enterprises, which led to rising unemployment and worsening labour conditions. Unemployment also rose from approximately 0.9% to 3.4% between 1997 and 1998, with rural communities being hit the hardest, with agricultural employment dropping around 3.2%. Due to an increase in unemployment, poverty grew and the number of people in extreme poverty increased from 6.8 million to 7.9 million. Budget cuts reduced vital spending on health, education and welfare, affecting vulnerable populations the most. Further issues arose with the attempt to sequence the reforms and when the capital account liberalisation occurred before adequate financial regulation and institutional infrastructure were in place, amplifying vulnerability.

IMF programmes were perceived as “one-size-fits-all”, administered without adequate regard for the social impact or local context. Thai negotiations sidelined democratic oversight, transferring the decision-making power from functional ministries to the Finance and Commerce departments. The IMF’s insistence on austerity during an economic contraction, particularly in countries that were already running surpluses, such as Thailand, was criticised as being counterproductive. In Thailand, the government was running such large surpluses that it was ultimately starving the economy of much‑needed investments in education and infrastructure.

4. Economic Effects of IMF Policies in the Middle East

The International Monetary Fund also plays a significant role in shaping economic policy across the Middle East, often intervening when countries face balance-of-payments crises, currency instability or spiralling debt. These interventions are designed to promote macroeconomic stability, restore investor confidence and support structural reform. However, their outcomes are far from uniform. In states with strong institutions and public safety nets, IMF programmes may succeed in stabilising economies without major social disruption, but in countries where political fragility, economic inequality and institutional weakness prevail, the IMF’s approach can trigger unintended and deeply destabilising consequences.

The following case studies explore how these dynamics have played out in practice, highlighting the IMF’s role not just as a lender, but as a powerful force that can reshape, and sometimes destabilise, entire political economies.

4.1 Tunisia

Tunisia offers a particularly illuminating case where the IMF imposed fiscal compression, currency weakening and tax hikes intersected with political fragility and public protest.

Following the 2011 revolution, Tunisia found itself in an economic hole. The fiscal deficits, rising public debt and sluggish growth rate pushed Tunisia into taking a $2.9 billion Extended Fund Facility with the IMF. According to an IMF press release, the fund’s conditions emphasised fiscal consolidation, subsidy reform, public wage restraint and currency flexibility: standard macroeconomic tools, but ones that proved socially costly. By 2018, the Tunisian dinar had lost nearly 50% of its value compared to 2013 levels. The IMF played a direct role in this trend by encouraging the Central Bank of Tunisia to reduce its intervention and allow the currency to float more freely. This was intended to improve export competitiveness and reduce the persistent trade deficit, as outlined in the IMF’s 2017 Article IV Consultation Report. However, this liberalisation contributed to a 10% depreciation in 2017, followed by a further 20% drop in 2018. Despite the intended macroeconomic benefits, the resulting devaluation triggered sharp increases in the price of imports, particularly fuel, food and consumer goods, significantly raising the cost of living for households across all income levels.

Simultaneously, the 2018 Finance Law introduced sweeping tax increases, also in line with IMF policy advice. VAT was increased by one percentage point across all brackets, and new customs duties were imposed on imported goods, notably cars, electronics and cosmetics. This led to noticeable price hikes. As INSEE reported in February 2018, even fuel, services and certain food items became pricier under the new tax regime. The combined impact of the tax hikes and currency depreciation was sharply felt by consumers; for example, a middle-income household spending 200 TND/month on imported goods would have seen its monthly bill rise to around 260 TND due to a 30% price increase. Moreover, a 1% VAT hike on a monthly expenditure of 1,000 TND adds another 10 TND. This results in an annual additional cost of roughly 840 TND, a significant burden in a country where GDP per capita was under $3,800 at the time (World Bank, 2018).

These pressures drove inflation up to 7.1% by early 2018, as recorded in the IMF’s 2018 Tunisia Country Report. Although the IMF claimed that targeted subsidies shielded the poorest households, the middle class, who consume a mix of subsidised and unsubsidised goods, were hit the hardest. The same IMF report noted that inflation for upper-income deciles reached as high as 8-9%. Public response was explosive. In January 2018, protests under the slogan “Fech Nestanew?” (“What Are We Waiting For?”) erupted nationwide. According to the BBC News, more than 800 people were arrested, and at least one person died during clashes with police. Demonstrators explicitly blamed the IMF and austerity policies for rising prices and declining living standards.

Tunisia’s experience demonstrates the political limits of externally imposed stabilisation. Though the IMF’s macroeconomic logic may have been sound, the speed, structure and social consequences of its reforms, particularly in a transitioning democracy, triggered unrest that ultimately undermined the success of the programme itself.

4.2 Jordan

Before the IMF’s involvement in 1996, Jordan faced high unemployment, growing public debt and a reliance on foreign aid and subsidies to maintain social stability. The country’s economy was strained by regional instability and an influx of refugees, which overwhelmed public services. Corruption and weak governance further eroded trust in institutions.

Jordan’s 1996 unrest over bread subsidies highlights how IMF-backed austerity, when delivered abruptly and without social cushioning, can escalate into full-blown social uproar. The story starts with deeper roots, Jordan’s financial crisis in 1989, when IMF-mandated subsidy cuts fuelled violent protests, ultimately forcing political reforms. This broader pattern is discussed in the International Review of Social History’s piece “Privatizing the Commons”, which links the 1996 unrest directly to the structural adjustment pressures first introduced in the late 1980s.

By 1996, macroeconomic conditions had stabilised. Jordan had implemented several IMF-required reforms: a 5% sales tax (later doubled), lifting the economic boycott of Israel and trimming deficits. Yet, one major IMF demand remained unfulfilled: ending long-standing wheat subsidies. In August 1996, Prime Minister Abdul-Karim Kabariti complied, lifting these subsidies abruptly. Bread prices immediately doubled, rising from approximately 0.075 JD/kg to 0.16 JD/kg for standard local flour bread (Martínez, 2018).

Jordan’s government attempted to cushion the blow with a cash transfer of $1.80 per person per month via the National Aid Fund (Ufheil-Somers, 1996). The insufficiency of this amount can be illuminated by a simple thought experiment. Assume a household of six receives $10.80 USD/month. Against a price increase where a family consuming 5 kg of bread/week (≈20 kg/month) saw costs rise from 1.5 JD to 3.2 JD (an increase of 34 USD/month at the 1996 conversion rate), the transfer covered only ~32% of the extra burden. The rest fell on already-strained budgets, with dairy and fodder prices rising too, undermining any compensation.

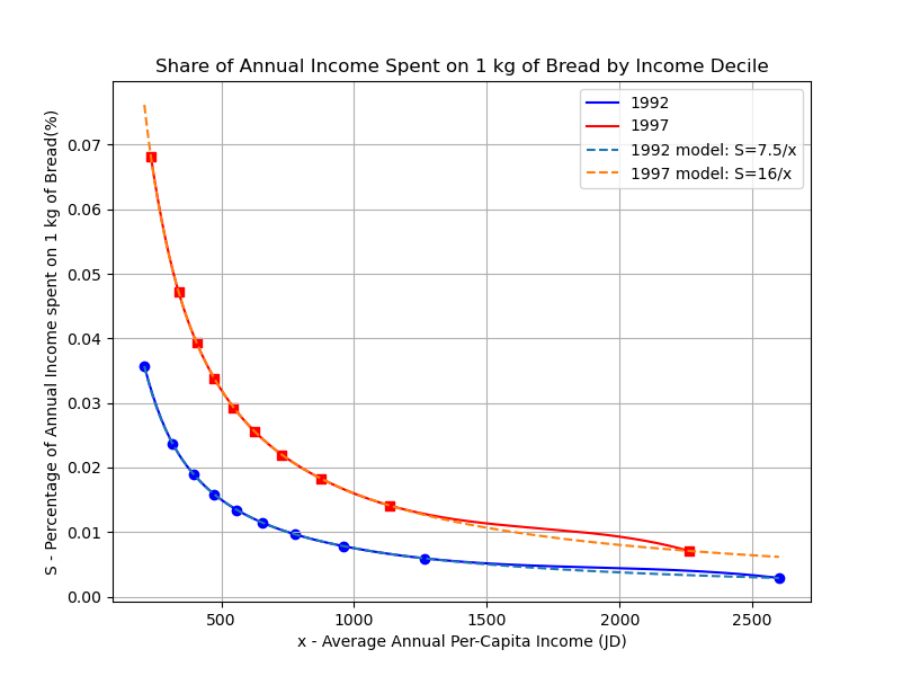

This issue also led to an increase in inequality. The following graph measures the percentage of income spent on 1 kg of bread against the average annual per capita income (x). The blue line represents the relationship before the subsidies were cut and the red line represents the relationship after they were cut. The annual income per capita data used were 1992 and 1997, as it was the closest available years before and after the subsidy cut, sourced from the “Jordan Poverty Assessment Report” from the World Bank (2004). Ceteris paribus, the following graph accounts solely for the increase in bread prices due to the subsidy cut.

Figure 3: Share of Annual Income Spent on 1 kg of Bread by Income Decile (World Bank, 2004).

The dashed lines represent the theoretical counterparts of the real data plotted (represented by the solid lines).

S_1992 (x) = 7.5 / x

Function (1)

S_1997 (x) = 16 / x

Function (2)

Functions (1) and (2) are equations that most closely model the lines produced when plotting the data, which were derived by directly taking the price of bread/kg before and after the subsidy cut and multiplying this by the inverse of x. This was done because the percentage of Annual Income spent on 1 kg of bread would be inversely proportional to the average income per capita.

Using functions (1) and (2), we can differentiate x to form the following two equations:

(dS_1992 (x) / dx) = -7.5 / x^2

(dS_1997 (x) / dx) = -16 / x^2

These equations represent the rate of change in the burden of bread costs, which shows that after the subsidy cut, a small change in the income of a person (some value x) caused a larger change in the burden of bread on income. This can be interpreted as an increase in inequality.

Unsurprisingly, protests erupted. Three days after the launch of the policy, mass demonstrations began in Karak and quickly spread across southern towns Ma’an, Tafilah and Zarqa, and eventually reached Amman. These events were covered extensively by the Christian Science Monitor, which reported rioters setting fire to government buildings and banks, while the government responded with tear gas, armoured vehicles and curfews. Security forces cracked down.

The UPI Archives also document that prices of bread in the south rose from 85 fils to 250 fils per kg, a +200% increase, which triggered immediate unrest across the south. The Washington Post noted that the riots spread through the king’s traditional power base, especially in the south, where unrest was most intense and politically threatening. The riots lasted for several weeks. Eventually, the government offered modest concessions, lowering some food prices and releasing detainees. Still, the shock signals from August 1996 contributed to Kabariti’s dismissal in early 1997.

The IMF’s involvement in the Middle East does not represent a failure of intent, but rather a failure of sensitivity to local conditions. The cases of Tunisia and Jordan illustrate how well-meaning economic prescriptions – fiscal consolidation, market liberalisation and subsidy removal – can spark backlash when applied in contexts where political legitimacy is fragile and citizens rely heavily on state subsidies to survive. These examples do not suggest that IMF integration policies are universally harmful, but they reveal the circumstances under which these policies become most volatile. Understanding the interaction between global financial institutions and domestic vulnerabilities is essential to assessing the IMF’s real-world impact and to preventing economic reform from becoming a trigger for social unrest.

5. Policy Discussion and Evaluation

The International Monetary Fund’s policies are often applied to different countries to resolve similar situations. This helps address large-scale issues that could lead to rapid economic downturns. By studying the policies of the IMF and examining the positive and negative outcomes, we can propose an optimal approach to address economic struggles in any country. Current policies of the IMF usually benefit countries in the short term by decreasing inflation rates or boosting countries’ competitiveness in world trade. Despite that, the IMF could simultaneously disregard the long-term wellbeing of the local populations and include possible economic issues around declining GDPs and over-dependency on other countries. The greatest criticism of the IMF is the “one-size-fits-all” approach, which does not consider countries’ local circumstances. Hence, to evaluate the aspects of the best approach that would prevent economic distress and collapse, this paper provides a synthesis of the most frequently used policies and their pros and cons, which can be adopted or omitted in the future.

5.1 Fiscal Consolidation

The IMF attempted fiscal consolidation in Southeast Asia during the 1997-98 Asian Financial Crisis, aiming to reduce deficits and restore investor confidence. In reality, these measures, even though often helpful, have also produced dramatic social and economic consequences for the region.

Thailand and Indonesia have pursued austerity by reducing spending in public spending sectors, primarily in education. This helped in reducing the overall spending. On the other hand, it caused an increase in school dropout rates, promoting a decline in national wellbeing and the overall standard of living. Additionally, the IMF increased VAT and reduced subsidies, which aimed at restoring fiscal discipline. This promoted efficiency and long-term commitment from the authorities. However, the alteration of the fiscal policies also worsened the recession, creating social unrest and riots in Indonesia and the falling GDP in Thailand.

Simultaneously, the IMF took the same policy approach in the MENA countries. Aiming to tackle the economic recession of the Middle Eastern countries by introducing subsidy cuts on certain common goods, such as bread in Jordan in 1996 and fuel in Tunisia from 2016 to 2018. Advantageously, the fiscal policies introduced by the IMF succeeded in reducing the government debt and the overall economic deficit. However, it almost caused famine and resulted in rioting across both Tunisia and Jordan. Furthermore, the newly imposed VAT on basic goods and further wage restraint led to middle-class poverty. Cost of living in the region also skyrocketed, leading to rising protests and even more riots as the compensational schemes failed to offset the burden of national debt.

Although the fiscal policies introduced by the IMF helped achieve fiscal stability, social cohesion and poverty reduction were sacrificed. Therefore, fiscal consolidation policies such as austerity and subsidy removal were unable to improve economic situations in the region. The long-term trade-offs were the societal outcomes, while the short-term trade-offs were temporary improvements in fiscal stability. Additionally, fiscal reforms often benefitted financial and business elites while worsening the situation for the poorer working class, creating instability within the economies and resulting in declining national confidence and independence, causing long-term dependency on the IMF aid and international financial support.

5.2 Monetary Tightening and Exchange Rate Policy

In the SEA countries, the IMF encouraged abandonment of currency pegs and floating currencies, taking the “laissez-faire” approach. This resulted in a reduction of currency reserves and prevented world currencies from circulating within the SEA countries. For instance, in Indonesia, the IMF ordered sharp interest-rate hikes (up to 70%) to defend the rupiah, which was prior pegged to the USD, ultimately leading to the critical credit crunch and bankruptcies of businesses and industries.

Furthermore, the nation faced a collapse in confidence in both the government and the IMF due to their failure to achieve the promised economic results. Similarly, Thailand saw the devaluation of the baht caused by high foreign debt and over-investment in certain industries. This resulted in an imbalance in the economy, loss of confidence from the investors due to the outbreak of the Asian Financial Crisis and failure of the IMF to adjust its policies according to the situation in Thailand. The economy endorsed depreciation and ended up highly dependent on external aid, such as that provided by the IMF.

Meanwhile, the Middle East experienced the implication of similar policies. In Tunisia, the IMF’s policy of promoting exchange-rate flexibility resulted in a 50% decline in the overall economy. Instead of prioritising structural reforms of the Tunisian economy, the IMF also made the country reliant on external borrowings, resulting in a national debt of $5.5 billion USD in 2024, making up 110% of the current GDP. The inflation crisis severely affected the economic stability of the Tunisian middle class. As the cost of living surged, driven by rising prices of goods and services, the purchasing power of citizens diminished. Deterioration was increased by cuts in subsidies and the privatisation of essential public services, including healthcare and education, further reduced the financial wellbeing of the population. The IMF aimed to improve trade quality and narrow its deficit by strengthening the local currency. These policies, aimed at fiscal consolidation, led to widespread public discontent, riots and a massive drop in the national wellbeing.

Similar to Tunisia and the SEA, the IMF supported the peg stability of the dinar since the 1990s, which proved to be beneficial in the trade deals, improving investor confidence. However, the rigidity of the social and fiscal policies bore the adjustment burden, which prevented Jordan from developing its economy rapidly enough to keep up with the changing world economy and resulted in the loss of GDP and inflation rising as high as 25%.

The IMF’s monetary strategies in both Southeast Asia (SEA) and the Middle East reveal a consistent effort in stabilising currencies and attracting investor confidence, however, often at the expense of domestic social stability.

5.3 Overall recommendation

The overall recommended policy summarises the ways to address the issues outlined in the existing policies. It should aim to preserve the original objectives of the IMF, which include the mitigation of financial crises, economic downturns and inflation in the countries.

Our recommended policy encourages some of the current IMF approaches, such as certain kinds of privatisation and encouragement of interconnection with other nations or unions. However, the recommended policy also encourages the steadiness and softness of the policies as they are introduced. Furthermore, it insists on the adjustability of every approach to the ongoing situation in the country, disproving the “one-size-fits-all” recommendations, which can be seen as more effective in the long run.

Furthermore, our recommended policy suggests that the gradual implementation of reforms is superior to rapid change, as it does not destabilise the country and leave it to deal with the long-term consequences. A gradual VAT subsidy removal, combined with targeted safety nets, would avoid sudden price spikes or destabilisations. Additionally, currency liberalisation should allow countries to adopt hybrid systems that will protect them against excessive volatility and improve global competitiveness.

Arguably, future IMF policies should be tailored to domestic governments and societies to prevent harsh criticisms, increase legitimacy, and reduce the risk of riots. Additionally, the recommendation on sequencing the reforms, such as privatisation, will allow the economies to reach stabilisation. Otherwise, as shown in the examples of SEA and the Middle East, shocks from the unstable environment will deepen recession and social unrest.

Bibliography

Abdallah, S. (1996) ‘Jordan raises its bread price’, UPI [Internet]. Available at: https://www.upi.com/Archives/1996/08/13/Jordan-raises-its-bread-price/8908038819005/ (Accessed: 13 August 2025)

Adams, B.C. & Chadha, C. (2016) Growth, productivity, and the rate of return on capital. Washington, DC: International Monetary Fund [Working Paper]. Available at: https://www.imf.org/en/Publications/WP/Issues/2016/12/30/Growth-Productivity-and-the-Rate-of-Returnon-Capital-785 (Accessed: 14 August 2025)

Andoni, L. & Schwedler, J. (1996) ‘Bread riots in Jordan’, Middle East Report, 201.

Atlantic Council (2017) ‘Why inflation is so high in Egypt’, Atlantic Council [Internet]. Available at: https://www.atlanticcouncil.org/blogs/menasource/why-inflation-is-so-high-in-egypt/ (Accessed: 14 August 2025).

Basri, M.C. (2018) ‘Twenty years after the Asian Financial Crisis’, in Breuer, L.E., Guajardo, J. & Kinda, T. (eds) Realizing Indonesia’s economic potential. Washington, DC: International Monetary Fund. Available at: https://www.elibrary.imf.org/display/book/9781484337141/ch002.xml (Accessed: 16 August 2025).

BBC News (2018) ‘Tunisia protests: Reforms announced amid new rallies’, BBC [Internet]. Available at: https://www.bbc.co.uk/news/world-africa-42679328 (Accessed: 19 August 2025).

Castillo-Ponce, R.A. & Lai, K.S. (2020) ‘On Argentina’s currency crisis of 2018’, Lecturas de Economía, (92), pp. 223–233. Available at: https://www.redalyc.org/journal/1552/155260967009/html/ (Accessed: 17 August 2025).

Gray, G. & Kingsley, T. (2023) ‘U.S. participation in the International Monetary Fund (IMF): A primer’, American Action Forum [Internet]. Available at: https://www.americanactionforum.org/insight/u-s-participation-in-the-international-monetary-fund-imf-a-primer (Accessed: 17 August 2025).

Hausman, T. (2023) ‘Developed countries definition, list & characteristics’, Study.com [Internet]. Available at: https://study.com/academy/lesson/developed-countries-definition-examples.html (Accessed: 16 August 2025).

International Monetary Fund (1998) Indonesia memorandum of economic and financial policies, January 15, 1998 – Letter of intent. Washington, DC: IMF. Available at: https://www.imf.org/external/np/loi/011598.htm (Accessed: 20 August 2025).

International Monetary Fund (2004) Stabilization and structural transformation of the Jordanian economy. Washington, DC: IMF. Available at: https://www.elibrary.imf.org/view/journals/002/2004/121/article-A002-en.xml (Accessed: 17 August 2025).

International Monetary Fund (2015) Press release: IMF Executive Board approves US$2.9 billion extended arrangement under the Extended Fund Facility for Tunisia. Washington, DC: IMF. Available at: https://www.imf.org/en/News/Articles/2015/09/14/01/49/pr16238 (Accessed: 16 August 2025).

International Monetary Fund (2018a) Tunisia: 2017 Article IV consultation and second review under the Extended Fund Facility, and request for waivers of nonobservance of performance criteria, and rephasing of access. Washington, DC: IMF. Available at: https://www.imf.org/en/Publications/CR/Issues/2018/06/12/Tunisia-2017-Article-IV-Consultation-and-Second-Review-Under-the-Extended-Fund-Facility-and-45877 (Accessed: 19 August 2025).

International Monetary Fund (n.d.) What is the IMF? Washington, DC: IMF. Available at: https://www.imf.org/en/About/Factsheets/IMF-at-a-Glance (Accessed: 15 August 2025).

Iriana, R. & Sjöholm, F. (2002) ‘Indonesia’s economic crisis: contagion and fundamentals’, The Developing Economies, 40(2), pp. 135–151. Available at: https://onlinelibrary.wiley.com/doi/abs/10.1111/j.1746-1049.2002.tb01004.x?msockid=0f5604424c0968b33aa5120e4db269d1 (Accessed: 15 August 2025).

Johnson, C. (1998) ‘Economic crisis in East Asia: The IMF and its critics’, Government and Opposition, 33(1), pp. 1–28. Available at: https://www.jstor.org/stable/23601496. (Accessed: 20 August 2025).

Kazel, M. (2025) ‘What is the International Monetary Fund (IMF)?’ Investopedia [Internet]. Available at: https://www.investopedia.com/terms/i/imf.asp (Accessed: 25 August 2025).

Lacouture, M. (2021) ‘Privatizing the commons: Protest and the moral economy of national resources in Jordan’, International Review of Social History, 66(S29), pp. 113–137. Available at: https://www.cambridge.org/core/journals/international-review-of-social-history/article/privatizing-the-commons-protest-and-the-moral-economy-of-national-resources-in-jordan/8F08554C1CD303AAA22F1C94FFD0503B? (Accessed: 25 August 2025).

Lipscy, P.Y. & Lee, H.N. (2019) ‘The IMF as a biased global insurance mechanism: asymmetrical moral hazard, reserve accumulation, and financial crises’, International Organization, 73(1), pp. 35–64. Available at: https://www.cambridge.org/core/journals/international-organization/article/abs/imf-as-a-biased-global-insurance-mechanism-asymmetrical-moral-hazard-reserve-accumulation-and-financial-crises/E945D3C17534A50EE7D0595E8FB9CD40 (Accessed: 22 August 2025).

Martínez, J.C. (2018) ‘Slow and steady wins the race: How the gradualist approach eliminated Jordanian bread subsidies’, Philosophy, Politics, and Economics Review. Virginia Tech Publishing. Available at: https://pressbooks.lib.vt.edu/pper/chapter/slow-and-steady-wins-the-race-how-the-gradualist-approach-eliminated-jordanian-bread-subsidies/ (Accessed: 19 August 2025).

Novik, V. (2020) ‘The countries most and least affected by the 2008 financial crisis’, Big Economics [Internet]. Available at: https://bigeconomics.org/the-countries-most-and-least-affected-by-the-2008-financial-crisis/ (Accessed: 25 August 2025).

Peterson, S. (1996) ‘Bread riots in Jordan force king to wield an “iron fist”’, Christian Science Monitor [Internet]. Available at: https://www.csmonitor.com/1996/0819/081996.intl.intl.1.html (Accessed: 19 August 2025).

Radelet, S. & Sachs, J. (1998) The onset of the East Asian financial crisis. Cambridge, MA: National Bureau of Economic Research. Available at: https://www.nber.org/papers/w6680 (Accessed: 19 August 2025).

Rocamora, J. (2025) ‘The 1997 financial crisis and Asian progressives’, Transnational Institute. Available at: https://www.tni.org/en/article/the-1997-financial-crisis-and-asian-progressives (Accessed: 19 August 2025).

TAP (2018) ‘Le taux d’inflation atteint un nouveau record de 7,1 %, en février 2018’, TAP [Internet]. Available at: https://www.tap.info.tn/fr/Portail-%C3%A0-la-Une-FR-top/9929470-le-taux-d-inflation. (Accessed: 20 August 2025).

Turner, J. (2024) ‘Why did the global financial crisis of 2007–09 happen?’, Economics Observatory [Internet]. Available at: https://www.economicsobservatory.com/why-did-the-global-financial-crisis-of-2007-09-happen (Accessed: 20 August 2025).

Ufheil-Somers, A. (1996) ‘Bread riots in Jordan’, MERIP [Internet]. Available at: https://merip.org/1996/12/bread-riots-in-jordan (Accessed: 19 August 2025).

UNCTAD (2025) ‘Debt crisis: Developing countries’ external debt hits record $11.4 trillion’, UNCTAD [Internet]. Available at: https://unctad.org/news/debt-crisis-developing-countries-external-debt-hits-record-114-trillion (Accessed: 17 August 2025).

Willmoth, H. (2025) ‘Only one country in the world produces all the food it needs, study finds’, BBC Science Focus [Internet]. Available at: https://www.sciencefocus.com/news/only-one-country-produces-food-it-needs-self-sufficient (Accessed: 19 August 2025).

Woods, N. (2024) ‘Stranded? The IMF in a world of rising economic nationalism’, Oxford Review of Economic Policy, 40(2), pp. 329–348. Available at: https://academic.oup.com/oxrep/article/40/2/329/7691470 (Accessed: 15 August 2025).

World Academy of Sciences (2025) ‘Least developed countries (LDCs)’, World Academy of Sciences [Internet]. Available at: https://twas.org/least-developed-countries-ldcs (Accessed: 18 August 2025).

World Bank (2004) Jordan – Poverty assessment (Vol. 2 of 2). Available at: http://documents.worldbank.org/curated/en/194491468047051364 (Accessed: 11 September 2025).

YouTube (2025) ‘IMF financial operations: Overview’, IMF [Video]. Available at: https://www.youtube.com/watch?v=f0CPO2osWOM (Accessed: 19 August 2025).

{kind=link}