Abstract

This article examines how the International Monetary Fund (IMF) promotes economic recovery and long-term financial stability while keeping social equity within countries during recent years (2010-present). The IMF plays a crucial role in supporting nations while they are facing serious economic crises (IMF, 2024). This includes balance of payments issues, sovereign debt crises, inflationary pressures, currency depreciation and declining investor confidence. In these situations, the IMF can restore macroeconomic stability without deepening the crisis by providing financial support, policy advice and reform programmes.

However, IMF-supported policies are often debated because measures that are designed to strengthen fiscal stability generate significant short-term costs (Li, Sy & McMurray, 2015). Policies such as the fiscal consolidation, subsidy reform, monetary tightening and structural adjustment may affect vulnerable populations greatly as these measures can affect employment, public services and income distribution. Therefore, the IMF’s effectiveness should not be measured by economic indicators such as inflation, debt sustainability, exchange rates and market confidence alone. Instead, the criteria for evaluation should include whether the IMF programme protects social equity and does not place the greatest burden on the most vulnerable.

This paper will argue that the IMF can support economic recovery and long-term financial stability through loans, conditional support, debt sustainability analysis, supervision and financial sector advisory. However, such support is most effective when reforms are realistic, designed to suit each country’s specific circumstances and accompanied by social protection measures. Long-term financial stability is most strongly supported when the recovery is not only financially sound but also socially acceptable.

Introduction

Economic crises are often measured by indicators like inflation, debt, exchange rates, unemployment and GDP growth (IMF, 1998). These numbers matter because they show the health of a country’s economy. However, the impact of a crisis extends far beyond these numbers. Behind every economic indicator are individuals whose lives can be significantly affected when the economy becomes unstable. A financial crisis can raise the cost of essentials such as food, fuel, medicine, housing, education and public services. It can also cause job losses, force businesses to close and make it harder for families to cover basic needs.

In a severe crisis, many problems often happen at once. These can include high government debt, loss of investor confidence, bank failures and difficulties for companies trying to secure financing. These problems cause a domino effect. For example, if investors doubt the government’s ability to repay debt, they may stop lending or ask for higher interest rates. This results in debt management being harder. When the currency falls, imported goods become more expensive, which increases inflation. As prices rise, it becomes harder for people to afford daily necessities. In these situations, the IMF plays a key role. The IMF is a global financial institution that helps countries facing serious economic and financial challenges (IMF, 2022). Its main job is to support countries that struggle to pay for imports, repay foreign debt and keep their currency stable when they lack foreign exchange. The IMF provides financial support, policy advice and reform programmes to help stabilise the economy.

IMF support usually comes with conditions. Countries that borrow from the IMF must carry out certain reforms or meet specific economic targets. These conditions are meant to address the main causes of the crisis and provide short-term relief. Common requirements include cutting fiscal deficits, raising tax revenues, reforming subsidies, strengthening central banks, controlling inflation and improving bank regulations. The purpose of these reforms is to restore confidence and create a more stable economy.

IMF programmes are often debated. Supporters say the IMF is necessary because major reforms are needed for a country in crisis to recover (AfricaNews, 2026). If a government has taken on too much debt or mismanaged its economy, financial help alone is not enough. In this view, the IMF guides countries through the tough but necessary changes to restore confidence, control inflation, stabilise the currency and bring back economic growth.

Critics argue that IMF programmes can have large social costs (Nozaki, Clements & Gupta, 2011). Steps like cutting spending, ending subsidies, raising taxes and tightening monetary policy can be hard for the average person. These actions may help reduce deficits or control inflation, but they can also weaken public services, increase unemployment and raise living costs for low-income families. If reforms are not planned carefully, the most vulnerable can be hit the hardest. That is why the IMF’s role should be judged by both economic and social results.

This paper examines how the IMF can help countries recover economically and achieve long-term financial stability while also protecting social fairness. This is important because recovery, stability and fairness are closely connected. Signs of recovery, like lower prices or improved investor confidence, do not mean much if poverty rises or public services decline. When countries face high debt, inflation and instability, it is also hard to protect social welfare. The main challenge is to balance restoring financial stability with protecting public welfare.

Economic recovery refers to the process through which countries emerge out of the ongoing crisis. This includes stable prices, renewed growth, lower unemployment, better fiscal health and restored confidence. Long-term financial stability means keeping debt at sustainable levels, maintaining stable inflation, having a strong banking system, reliable government policies and enough resilience to handle external shocks so that similar crises do not happen again.

Methodology

DATA SOURCES AND SEARCH STRATEGY

This study adopts a qualitative literature review approach to critically evaluate the role of the IMF in promoting economic recovery while maintaining social equity. This review integrates prior scholarly works that can help evaluate how effective the financial assistance, provision of policy direction and conditional lending programmes of the IMF have been at producing healthy economics and societies. It also examines the ongoing debate surrounding the benefits and implications of economic recovery efforts supported by the IMF.

All of the secondary sources used in this study were obtained from the collection of peer-reviewed academic journals, academic papers and publications produced by credible international organisations. The most prominent sources used in this research were the publications produced by the IMF, World Bank, United Nations (UN), Organisation for Economic Co-Operation and Development (OECD) and other authoritative sources that focus on international finance, macroeconomic policy and social development.

Search terms included combinations of keywords such as “International Monetary Fund”, “IMF conditionality”, “economic recovery”, “financial stability”, “sovereign debt”, “balance of payments crisis”, “structural adjustment”, “fiscal consolidation”, “social protection” and “social equity.”

INCLUSION AND EXCLUSION CRITERIA

The literature was selected based on the following sources:

- Peer-reviewed journal articles;

- Reports and documents published by international organisations (primarily the IMF);

- Academic publications and scholarly working papers (in English);

- Studies directly addressing IMF lending, macroeconomic stabilisation, financial crises, economic recovery, financial stability or the social impacts of IMF programmes.

The following were excluded:

- Articles that were not peer-reviewed;

- Academic studies that lacked sufficient rigour and/or relevance to the research objectives;

- Sources that did not specifically examine the IMF as being responsible for either the stabilisation of the economy and/or the creation of positive social outcomes.

The IMF and Economic Recovery

The common beginnings of economic crises are when a country is no longer able to meet its international financial obligations or maintain confidence in the nation’s currency. As foreign exchange reserves decline, governments may struggle to service external debt, causing currency devaluations, rising inflation, financial instability and increasing unemployment. Without external support, these problems can quickly develop into a severe economic crisis.

The IMF was established in 1944 to promote international monetary cooperation and maintain global financial stability following the Second World War (IMF, 2024). While its original purpose was to oversee the post-war international monetary system, the IMF at present plays a much broader role. They provide direct financial assistance, advisory services and institutional rebuilding support.

THREE TOOLS THE IMF USES TO SUPPORT RECOVERY

The IMF supports economic recovery through three interrelated methods by which they provide financial assistance (IMF, 2024): financial lending, policy advice and capacity development. Rather than applying a single solution, the IMF tailors its advice and assistance to the specific situation of each country.

This assistance generally follows the three phases of the economic recovery process. The first stage is preventive or pre-crisis support. This aims to reduce economic vulnerabilities prior to the emergence of a crisis through policy surveillance and precautionary lending arrangements. The second stage is short-term emergency assistance, where the IMF provides rapid financing during periods of acute economic distress to stabilise economies. The third stage focuses on post-crisis recovery and long-term development, supporting countries to recover from crises and implement wider-ranging economic reforms to achieve longer-term sustainable growth.

CAPACITY BUILDING

Beyond providing financial resources, the IMF places significant emphasis on strengthening national institutions. Weak public institutions are at the root of many recurring economic issues and intrinsic influences, limiting governments’ ability to manage public finances effectively. Through technical assistance and training in tax administration, the IMF provides public financial management, central banking and financial regulation (IMF, 2024). These reforms enable countries to respond more effectively to future economic shocks, while removing fiscal transparency and governance.

HOW MUCH DOES THE IMF ACTUALLY LEND AND WHEN?

The scale of IMF lending reflects the severity of the global economic conditions. Lending commitments typically rise sharply during periods of international financial turmoil and decline when countries regain access to private capital markets and the market stabilises.

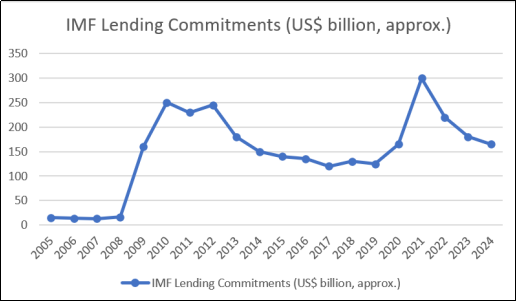

Figure 1 illustrates IMF lending commitments between 2005 and 2024.

Figure 1: IMF lending commitments, 2005–2024 (US$ billion, approximate, compiled from IMF and CRS data).

Two major peaks shown in the chart correspond to the Global Financial Crisis of 2009 and COVID-19. During the Global Financial Crisis, the IMF lending grew from approximately $16 billion in mid-2008 to nearly $250 billion by the end of 2009 (CRS, 2024). This rapid expansion of financial assistance helped many countries stabilise their economies. Without IMF financial assistance, it would have led to more extreme recessions, currency collapse and many countries evidencing sovereign debt defaults.

The COVID-19 pandemic prompted an even larger global response (IMF, 2021). As of early 2021, the IMF had committed over $285 billion to more than 85 countries, while its overall lending capacity reached approximately US$1 trillion. Although lending commitments declined after the peak of the COVID-19 pandemic, this reflected improving access to international capital markets and are not indicative of a reduction in the importance of the IMF. This lending demonstrate the IMF’s function as a global financial safety net, being able to respond to global crises quickly, even under severe economic stress.

IMF CONTRIBUTIONS DURING PANDEMIC

Public finances around the world have been subjected to unprecedented stress because of COVID-19. Governments worldwide incurred substantial new expenditures for healthcare, household income support and attempts to foster an economic recovery. In response, the IMF not only provided emergency financing, but also offered policy recommendations aimed at supporting economic recovery while maintaining fiscal sustainability.

The IMF’s COVID-19 Recovery Contributions report was the introduction of temporary excess profit taxes on firms that earned unusually high profits during the pandemic (IMF, 2020). The IMF argued that such measures could help governments finance pandemic-related expenditures while reducing inequality at the same time, promoting social cohesion. To minimise economic distortions, these taxes were to target economic rents rather than broadly apply to entire industries.

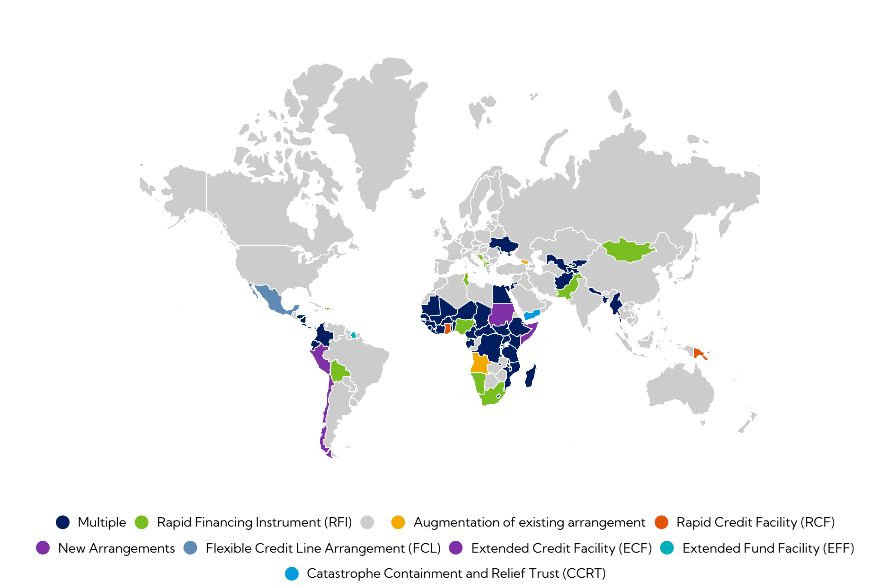

Figure 2 illustrates the global distribution of countries that received IMF financial assistance and debt service relief during the COVID-19 pandemic. It highlights the widespread scale of IMF support, particularly among developing and low-income economies that were most vulnerable to the pandemic’s economic impacts.

Figure 2: Countries receiving financial assistance and debt service relief from the International Monetary Fund (Sigel, 2021).

While financial assistance addresses immediate crises, policy reforms and capacity building seek to strengthen economies against future shocks and lay the foundations for long-term financial stability.

Case Studies

1. Greece

Problem: In June 2009, Greece had a major sovereign debt crisis stemming from excessive borrowing, poor fiscal discipline and erosion of confidence from investors (Peterson Institute for International Economics, 2020). Greece also was essentially shut out of international capital markets making it unable to finance its debt or have public spending without external assistance.

Context: The crisis arose from the fallout of the global financial instability and has revealed many of the economic problems in Greece, including high levels of public debt, inefficient collection of taxes and significant fiscal deficits. As a result of the collapse of confidence in markets, Greek borrowing costs skyrocketed, requiring Greece to seek international support.

Intervention: Since 2010, Greece participated in multiple euro-area and IMF-supported bailout packages to provide Greece with the emergency funding it was going to need to help avoid default and imposed strict terms of conditions to accomplish fiscal consolidation, structural reform and restore Greece’s competitiveness.

Measures Taken: Greece’s adjustment packages contained life-changing requirements for the country, such as reducing public sector wages and pensions, tax reforms and implementing structural reforms to achieve fiscal sustainability. While these measures ultimately stabilised Greece’s debt dynamics and restored market credibility, the process was achieved at immense social cost.

Outcomes: While the fiscal position in Greece improved and the overall deficit was reduced, the adjustment had severe economic and social consequences, such as an unemployment rate of over 25%, high rates of youth unemployment and many skilled people emigrating to other countries. Greece finished its last bailout programme in 2018.

Significance: The case of Greece shows how various types of policy conditionality imposed by the IMF will affect a country’s sovereign debt crisis, as both the source of emergency funds and the place where policy conditionality is enforced against a country. This experience illustrates that programmes supported by the IMF can restore a country’s macroeconomic stability and access to the capital markets but also create long-lasting economic and social effects.

2. Pakistan

Problem: Foundational dependency on the International Monetary Fund as an economic resource has been a long-standing fixture of Pakistan’s financial system, and the country sought assistance from the IMF with a Stand-By Arrangement (SBA) in 2023 and an Extended Fund Facility (EFF) in 2024 (EconomicLens, 2025).

Context: Loans provided by the IMF have primarily resulted in infrastructure changes such as energy sector reforms, a broadened tax base and the replenishment of foreign exchange reserves.

Intervention: IMF loans have provided support for energy sector reforms, the broadening of the tax base and the replenishment of foreign exchange reserves.

Outcomes: Early evidence indicates an increase in foreign exchange reserves, as well as stable currency markets. However, both inflation and increasing prices remain significant obstacles to lower income households and exemplify the fact that macroeconomic stabilisation does not always correspond to household welfare.

Significance: The case example demonstrates that repeated IMF engagement can provide a mechanism to stabilise a country’s external position and enhance financial confidence, but also shows the limitations of macroeconomic stabilisation when rising prices and the cost of living persist in low-income households.

3. Sri Lanka

Problem: A recent example of the evolution of the IMF’s approach can be seen in Sri Lanka. The country experienced its most severe economic collapse since independence in 2022. The government defaulted on external debt for the first time after almost exhausting its foreign reserves. Additionally, large-scale protests occurred in response to the lack of fuel and medicines, which created the catalyst that ultimately transformed the government (Ministry of Finance, 2025).

Context: The IMF approved a US$3 billion 48-month Extended Fund Facility programme in March 2023. This programme was intentionally constructed to build on a pre-existing debt restructuring. This required an agreement between Sri Lanka, bilateral creditors, such as China, Japan and India, and private bondholders before any significant financing could be made. The “restructure first” sequence was developed in response to past critiques that the IMF had previously participated in financing countries with unsustainable debt prior to resolving the underlying debt overhanging issues.

Intervention: Aswesuma is the government programme introduced in Sri Lanka to give low-income and high-risk families money through social welfare (Padmakanthi, 2023), replacing the old Samurdhi programme. Aswesuma started when Sri Lanka was going through an economic crisis and is part of a larger set of changes the country is making to its economy, which is also supported by the IMF. The overall goal of Aswesuma is to solely give money to the people who need it, and therefore reduce the amount of money the government puts into giving people poorly-targeted subsidies. Every month, families that are eligible for Aswesuma receive a cash transfer. The actual cash transfer amount varies by category. Eligibility for Aswesuma is based on a country-wide assessment of each family’s income, assets, living conditions and other socio-economic measures.

The programme is important because it intends to use targeted cash transfers instead of broad subsidies. As part of the new IMF-assisted reforms in Sri Lanka, Aswesuma will help prevent losing high-risk families during the period of budget savings and will also result in a more efficient social safety net system in Sri Lanka. Consequently, this demonstrates a shift toward integrated social protection. An explicit commitment to social protection was included as part of the programme, which included an expansion to the existing Aswesuma welfare transfer scheme, as well as setting social spending floors to protect health and education budgets even when other areas of spending are reduced. Finally, a revenue-based fiscal consolidation approach was used. This includes raising taxes on higher earners and corporations with the intent to create a broad-based approach to share the burden of adjustment. In 2024 and 2025, all external debt restructuring agreements had been reached, CPI inflation rates were off their peak level in 2022 and the Sri Lankan economy was experiencing a modest rebound.

Significance: By all measures, poverty levels remain significantly above pre-crisis levels and the benefits of the economic recovery will not be felt uniformly among all income groups. Sri Lanka’s experience demonstrates the limits to the adaptation of the IMF through the sequencing of debt relief before austerity and building social floors into programme design. While macroeconomic indicators point to an initial recovery, these gains have not yet fully translated into improved living conditions for those most affected by the 2022 economic crisis. As such, the early signs of progress are encouraging, but their effects on poverty reduction and household welfare will take time to materialise at the national level.

Long-Term Stability: Beyond the Crisis Moment

While providing emergency assistance is one of the IMF’s primary responsibilities, its broader objective concerns the long-term goal of promoting economic and financial stability through a commitment to the fiscal discipline of countries. Rather than simply resolving immediate crises, the IMF works to reduce the likelihood and severity of future economic shocks. They do this by promoting sound fiscal management, enhancing central bank independence and maintaining adequate foreign exchange rate reserves. The IMF aims to minimise the frequency and severity of future crises.

Following the 2008 Global Financial Crisis (Schinasi, 2005), the IMF has significantly increased its focus on conducting surveillance of the financial sector and stress-testing financial institutions. As a part of its Article IV consultations (IMF, 2024), the IMF regularly evaluates member countries’ economic performance and identifies potential vulnerabilities before they develop into full-scale crises. This preventive approach enables governments to address emerging risks early and improve long-term financial stability.

BUILDING IN SOCIAL EQUITY

Historically, the IMF has been criticised for emphasising financial targets over social consequences. Greece illustrated this point clearly. In response to these criticisms, the IMF has increasingly included social protection measures into its lending programmes to ensure that economic reforms are more inclusive.

The table below shows the measures to make economic reforms more socially inclusive. These measures are designed to protect vulnerable populations, reduce inequality and promote social equity by ensuring that the costs of the economic adjustments are not disproportionately borne by low-income households.

| Policy Instrument | Purpose | Expected Outcome |

|

Social spending floors |

Protect health and education budgets from cuts |

Reduced vulnerability for low-income households |

|

Targeted cash transfers |

Direct support for the poorest households |

Lower poverty rates during adjustment |

|

Progressive taxation |

Spread the fiscal burden more fairly |

Reduced inequality |

|

Employment programmes |

Support labour market participation |

Higher employment, smoother transition |

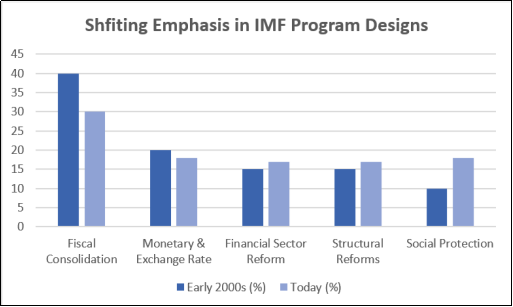

Figure 3 illustrates how the priorities within IMF-supported programmes have evolved since the early 2000s. Whereas earlier programmes focused primarily on fiscal consolidation, more recent programmes place greater emphasis on protecting social spending, supporting vulnerable groups and promoting inclusive growth alongside macroeconomic stability.

Figure 3: Illustrative shift in emphasis across IMF programme design elements (qualitative weighting, not an official IMF metric).

Social Impacts

The social impacts of the IMF-supported programmes remain as one of the most widely debated aspects of the organisation (Pettinger, 2024). While the IMF programmes aim to restore macroeconomic stability and rebuild investor confidence, the conditions attached to its loans can create significant short-term challenges for vulnerable populations. One of the most common features of IMF programmes is fiscal consolidation, often referred to as austerity (PFM, 2023). Fiscal consolidation measures, such as reducing public spending, are intended to strengthen public finances but may also raise living costs and reduce access to essential public services. Therefore, governments receiving IMF assistance may be required to reduce public spending, reform welfare systems or remove subsidies. These measures can lead to cuts in healthcare, education and social protection programmes. As a result, low-income households may experience increased financial hardship, reduced access to public services and declining living standards (Biglaiser & McGauvran, 2022).

The case studies from above – Greece, Pakistan and Sri Lanka – illustrate this balance between economic recovery and social equity. During Greece’s sovereign debt crises, IMFs assistance helped prevent a financial collapse. However, austerity measures led to cuts in public sector wages and government spending, contributing to higher unemployment and widespread public protests (IMF, 2024). Similarly, Pakistan’s IMF-supported programmes in 2023 and 2024 required fiscal reforms and subsidy reductions in order to stabilise the economy. However, these measures increased the financial burden on households, adding to the high inflation. Additionally, in Sri Lanka, the IMF supported debt restructuring following the country’s 2022 economic collapse (IMF, 2022). While these reforms were necessary to restore financial stability, the crisis resulted in severe shortages of necessities, highlighting the significant social costs of economic adjustment.

In response to criticism, the IMF has incorporated social protection provisions into its financing initiatives (PFM, 2023). Recent initiatives include social spending floors to protect healthcare and education budgets, targeted cash transfers for low-income families and tax policies that promote equitable treatment. These initiatives seek to maintain economic stability while reducing the negative social effects of fiscal shifts. The IMF’s realisation that long-term economic recovery required both financial stability and protection for marginalised groups is reflected in this change. However, the IMF continues to face major difficulties when it comes to striking a balance between social justice and fiscal discipline.

Criticism That Still Sticks

Despite these adaptations, the IMF remains one of the more contested institutions in global economic governance.

Critics argue that the IMF lending programmes focus more on global economic stabilisation over social equality. Among the most frequently cited criticisms are the use of austerity measures (typically reducing government expenditure and increasing tax collection), which can lead to slowed economic growth and a lower standard of living for the general public (Ostry, Loungani & Furceri, 2016). These measures disproportionately affect the poorest members of a society. Another criticism of IMF lending programmes is related to conditionality, as loan agreements often require governments to implement specific policies as part of the loan process (Kentikelenis, Stubbs & King, 2016).

However, supporters argue that these conditions are intended to address an underlying cause of economic crises and promote long-term stability (Stiglitz, 2002). Structural reforms can improve fiscal discipline, in addition to strengthening public finances, making the economies more resilient towards future shocks. An example of this is South Korea. Following the 1997 Asian Financial Crisis, South Korea implemented IMF-supported reforms that encouraged more responsible fiscal management. Although the reforms were initially unpopular, it contributed to fostering greater public awareness of the importance of sustainable economic management. This demonstrates that whilst IMF programmes often involve difficult short-term consequences, they can also support lasting institutional and economic benefits.

Another major criticism of IMF lending programmes are the concerns about national sovereignty. When outside organisations influence a country’s domestic policies, it undermines the country’s ability to control its own economic decisions. IMF programmes can create significant social costs (e.g., increased unemployment and inequality) for citizens over the course of an economic adjustment period, and this strain may be especially difficult for households who are already experiencing financial challenges.

Last, there are also concerns about governance within the IMF itself, particularly because the country’s decision-making power is largely determined by the share of its funding. Generally, countries that provide more significant amounts of financial resources to the IMF have a higher degree of power and control over the IMF’s operating procedures and policies. The consequences of the financial contribution structure raise fundamental questions regarding equality and equitable representation within the context of the global economic system.

The issues raised above illustrate the ongoing debate on how IMF lending programmes seek to strike a balance between the pursuit of financial stability and the consideration of social and political consequences.

Evaluating the Effectiveness

Based on macroeconomic performance (inflation control, exchange rate stability, rebuilding reserves, restoring investor confidence), IMF programmes have a strong probability of being successful (IMF, 2024). This can be seen through the contributions of the IMF to Sri Lanka’s debt restructuring. However, just because macroeconomic stabilisation occurs does not mean that the average person’s life will improve. The disparity between the two will largely depend on the quality of governance in-country, the way reforms are implemented and if social protection is truly built into the programme rather than being an add-on.

The candid assessment is that the IMF performs its function as stabiliser, not as a cure. The IMF can prevent the collapse of a country’s currency, rebuild foreign reserves and buy some time for a government. However, it is primarily reliant on government policies: how to tax citizens, who to protect and how gradually to builds the institutions necessary to avoid a financially damaging subsequent crisis. This is to determine if that “time” will be converted into a more equitable, sustainable economy. Sri Lanka’s ongoing recovery (IMF, 2025) will likely be the best live indicator of whether the newer, socially conscious IMF model will produce equitable results, rather than just financial remedies.

The Future of the IMF

As economic crises become more complex, the role of the IMF continues to evolve. In the past, IMF programmes mainly focused on restoring macroeconomic stability through fiscal adjustment and financial reforms. Today, there is increasing recognition that economic recovery should also consider long-term resilience and social outcomes. Future IMF programmes are expected to place greater emphasis on protecting vulnerable groups while maintaining financial discipline. This may include stronger social spending floors, more targeted support measures and reforms tailored to each country’s specific economic and social conditions rather than a standard approach.

In addition, the IMF is likely to expand its involvement in areas such as sovereign debt restructuring, financial sector resilience and responding to global challenges, including climate-related shocks, pandemics and disruptions in international markets. These changes reflect a broader understanding that stable economies depend not only on balanced budgets and low inflation, but also on the ability of societies to adapt and recover sustainably. The future success of the IMF will therefore depend not only on whether countries return to economic growth, but also on whether recovery improves living standards and creates long-term social and financial stability

Conclusion

This paper has examined how the IMF promotes economic recovery and long-term financial stability while addressing social equality in crisis-affected countries since 2010. The analysis of this paper shows how the IMF plays a central role in stabilising economies through emergency lending and policy advising, particularly during major disturbances such as the 2008 Global Financial Crisis, the COVID-19 pandemic and the sovereign debt crises. These interventions help restore investor confidence, stabilise currencies and prevent escalation of economic crises.

Case studies of Greece, Pakistan and Sri Lanka demonstrate how the IMF-supported programmes can create significant short-term social costs. Particularly, when fiscal consolidation and structural reforms lead to reduced public spending or higher living costs due to inflation. These outcomes highlight the tension between achieving macroeconomic stability while protecting vulnerable populations.

Despite these challenges, recent reforms indicate growing emphasis on social equity. The instituting social spending floors and stronger protection of essential public services reflect an effort of inclusivity. While these measures do not eliminate related social challenges, it suggests the IMF is attempting to balance the fiscal discipline alongside social dimensions.

Overall, these results suggest that the IMF has become more responsive to the social dimension in the cost of economic recovery. Significant challenges remain in ensuring that stability is achieved without disproportionally affecting lower-income groups. The effectiveness of the IMF intervention, therefore, depends not only on restoring financial stability, but also on whether recovery processes are both economically and socially inclusive.

Bibliography

Biglaiser, G. & McGauvran, R.J. (2022) The effects of IMF loan conditions on poverty in the developing world, Journal of International Relations and Development, 25(3), pp.806–833.

Balasundharam, V., Basdevant, O., Benicio, D., Ceber, A., Kim, Y., Mazzone, L., Selim, H. & Yang, Y. (2023) Fiscal consolidation: What can we learn from the past?, IMF PFM Blog [online]. <https://blog-pfm.imf.org/en/pfmblog/2023/05/08/fiscal-consolidation-what-can-we-learn-from-the-past>

Congressional Research Service (2022) The International Monetary Fund: Background and Issues for Congress, CRS Reports [online].

Congressional Research Service (2024) Annual Report Fiscal Year 2024, CRS [pdf] <https://www.loc.gov/crsinfo/about/CRS-Annual-Report-FY2024.pdf>

EconomicLens (2025) Pakistan’s Debt Emergency: IMF Bailouts, Fiscal Stress & the Road to Recovery, EconomicLens [online]. <https://economiclens.org/pakistans-debt-emergency-imf-bailouts-fiscal-stress-the-road-to-recovery/>

Ferri, G. (2003) Joseph E. Stiglitz (2002) Globalization and Its Discontents, Economic Notes, 32(1).

International Monetary Fund (n.d.) About the IMF, IMF [online]. <https://www.imf.org/en/about>

International Monetary Fund (n.d.) Greece and the IMF, IMF [online]. <https://www.imf.org/en/countries/grc>

International Monetary Fund (2025) IMF Lending, IMF [online]. <https://www.imf.org/en/about/factsheets/imf-lending>

International Monetary Fund (2026) IMF Executive Board Completes the Combined Fifth and Sixth Reviews Under the Extended Fund Facility for Sri Lanka, IMF [online]. <https://www.imf.org/en/news/articles/2026/05/27/pr26172-sri-lanka-imf-completes-combined-5th-and-6th-reviews-under-eff>

Kentikelenis, A.E., Stubbs, T.H. & King, L.P. (2016) IMF conditionality and development policy space, 1985–2014, Review of International Political Economy, 23(4), pp.543–582.

Klemm, A., Hebous, S., Michielse, G. & Nersesyan, N. (2021) COVID-19 Recovery Contributions, International Monetary Fund [pdf]. <https://www.imf.org/-/media/files/publications/covid19-special-notes/en-special-series-on-covid19-recovery-contributions.pdf>

Li, L., Sy, M. & McMurray, A. (2015) Insights into the IMF bailout debate: A review and research agenda., Journal of Policy Modeling, 37(6), pp.891–914.

Meghir, C., Vayanos, D. & Vettas, N. (2010) The economic crisis in Greece: A time of reform and opportunity, Research Gate [online]. <https://www.researchgate.net/publication/225083468_The_economic_crisis_in_Greece_A_time_of_reform_and_opportunity>

Nozaki, M., Clements, B.J. & Gupta, S. (2011) What Happens to Social Spending in IMF-Supported Programs?, IMF Staff Discussion Notes, 015.

Ostry, J.D., Loungani, P. & Furceri, D. (2016) Neoliberalism: Oversold? Finance & Development, 53(2), pp.38–41.

Oyinloye, A. (2026) Can the IMF help Africa break the debt cycle? {Business Africa}, Africanews [online]. <https://www.africanews.com/2026/06/25/can-the-imf-help-africa-break-the-debt-cycle-business-africa/>

Padmakanthi, N.P. (2023) Sustainable way to eradicate poverty through social protection: The case of Sri Lanka, Social Sciences, 12(7), 384.

Peterson Institute for International Economics (2020) Case Study: The Greek Debt Crisis, PIIE [pdf]. <https://www.piie.com/sites/default/files/documents/greek-debt-crisis.pdf>

Schinasi, G.J. (2005) Safeguarding Financial Stability: Theory and Practice (Washington, DC: International Monetary Fund).

Sigel, M. (2021) Tracking Sovereign Adoption of Bitcoin: A Potential Tipping Point?, VanEck [online]. <https://www.vaneck.com/us/en/blogs/digital-assets/matthew-sigel-tracking-sovereign-adoption-of-bitcoin-a-potential-tipping-point/>

{kind=link}