Abstract

The digitisation of global finance has transitioned from a phase of user interface improvement to a fundamental restructuring of payment rails and credit assessment architectures. This report investigates the convergence of embedded finance, real-time cross-border payments and artificial intelligence (AI). Specifically, it examines how graph neural networks (GNNs) in fraud detection and algorithmic cash-flow underwriting in credit scoring are enhancing financial inclusion and operational efficiency. However, this technological shift introduces new vectors of systemic risk, including model homogeneity, algorithmic herding behaviour and the opacity of cross-border data flows. By analysing initiatives such as the BIS Innovation Hub’s Project Aurora and Project Nexus, alongside commercial applications by entities like Tala, Nubank and Nova Credit, this report argues that while AI is the only viable mechanism to secure high-velocity payment rails, it necessitates a new macro-prudential framework to manage the risks of synchronised algorithmic failure.

Introduction

The global financial system is undergoing its most significant redesign since the rise of electronic banking. What began as simple digitisation has evolved into a deep restructuring of payment rails, liquidity pathways and credit assessment models. This transformation is driven by the convergence of embedded finance, interoperable cross-border networks and increasingly intelligent computational systems. Financial services are no longer confined to banks but are now integrated into platforms used for shopping, transportation, content creation and decentralised digital interactions. As these ecosystems merge, long-standing assumptions about identity, risk and regulatory oversight are being fundamentally reconsidered.

Artificial intelligence (AI) sits at the centre of this shift. With transactions settling in milliseconds and data volumes growing exponentially, human-centred risk controls are no longer sufficient. Machine learning models – ranging from graph-based anomaly detectors to behavioural scoring engines – now perform core functions such as fraud prevention, credit underwriting and real-time payment verification. AI has effectively moved from the periphery of financial operations to the backbone of global financial integrity.

Yet this rapid adoption introduces structural contradictions. The same models that enhance precision and expand access to credit also create tightly linked algorithmic environments where failures can cascade quickly and invisibly. Cross-border data dependencies, institution-wide model similarity and reliance on a small group of AI and cloud providers raise pressing macro-prudential concerns. What happens when multiple institutions rely on the same flawed model? How do regulators oversee intelligence that operates across jurisdictions and at machine speed?

This paper explores AI’s dual role as both a stabilising force and a new source of systemic vulnerability. By analysing international regulatory guidance, cross-market pilots and emerging high-velocity payment systems, it argues that AI is not simply another technological upgrade but a foundational redesign of global financial infrastructure. Managing the risks of this transformation will require governance frameworks capable of addressing algorithmic interdependence and preventing synchronised failures in an increasingly automated financial world.

1. Digital Banking

The rise in digital banking and its integration into daily financial activities is fundamentally transforming the delivery of banking services by enhancing efficiency, accessibility and overall customer experience.

During the last three decades, the financial services industry has experienced various advancements; one of these being the emergence of digital banking. Digital banking refers to the digitisation of banking services that previously required a branch visit. It can also be defined as the use of online and mobile channels to provide banking services, including money transfers, bill payments and account management.

The COVID-19 pandemic has significantly boosted digital banking adoption since consumers needed to find ways to perform various financial operations while remaining at home. As of 2025, approximately 3.6 billion people worldwide use online banking (Burnett & Kinder, 2025), underscoring the extent to which digital banking has become an integral component of daily financial activities, substantially enhancing the efficiency and accessibility of banking operations.

Digital banking is based upon the combination of digital platforms, advanced software and secure network infrastructures that provide customers with the possibility to manage their finances without visiting a physical branch.

- Web platforms and mobile applications conduct transactions and account management, offering instant transfers and payments along with real-time access to balances and other banking services.

- Artificial intelligence and machine learning are employed with the aim to enhance personalisation, detect fraud and streamline operations.

- Cloud computing assists in data storage, ensuring reliability and scalability of the system.

These technologies are integrated to improve speed, efficiency, security and accessibility of banking services, forming a foundation of digital banking operations.

1.1 Key Advantages and Improvements Over Traditional Banking

Digital banking has offered valuable benefits compared to traditional banking that was in use previously. The main advantage presented was the possibility to perform various banking operations from anywhere in the world (given there is stable internet connection) and at any time. Moreover, digital banking reduced costs by requiring fewer employees and limiting its reliance on physical branches. Digital solutions have facilitated automatic payments that can be performed on behalf of customers without their direct involvement. This has significantly simplified routine transactions since consumers can delegate part of their responsibilities and focus on more meaningful tasks. Consequently, automatic payments not only have reduced the likelihood of missed deadlines or penalties but also enhanced overall financial convenience. Additionally, digital banking is more environmentally sustainable, as it minimises paper usage through digitisation of processes and operations, therefore reducing the financial industry’s contribution to global deforestation. Finally, it facilitates faster cross-border payments, enabling efficient currency conversions and batch payments. Thus, many complexities, inefficiencies and high costs associated with international transactions have been significantly reduced after the emergence of digital banking.

1.2 Security Measures in Digital Banking

Security has become a major concern in mobile banking applications and online services. Digital banking now employs multi-factor authentication, biometric verification and continuous AI-powered monitoring to mitigate crimes and other illegal activities within the financial industry. All transactions are constantly screened for potentially suspicious activity, and those appearing to be fraudulent can be blocked in order to enhance the overall security of the system and assist in preventing unauthorised access or financial losses. In addition, tokenisation is used to further improve security. This technology replaces sensitive information, such as card numbers, with unique tokens so that the actual data remains hidden during transactions. Overall, security is considered a top priority in digital banking, and various technologies are employed to ensure system stability and reliability.

1.3 Impact on the Banking Industry and Competition

The emergence of digital banking has had a substantial impact on the whole financial industry. Firstly, it has put considerable pressure on traditional banks by offering better terms and greater variety of services to customers. As a result, many traditional banks have been forced to develop their own mobile applications and websites to stay competitive. Also, digital banking has resulted in the rise of fintech startups and neobanks (which are digital-only banks) across the globe. Secondly, the level of competition has increased since barriers to entry have become significantly lower, making the financial industry more attractive for new entrants. Thus, consumers have enjoyed a greater variety of suppliers and better deals offered by banks to surpass their competitors. Overall, the financial industry has expanded, reaching previously unserved populations due to remote locations and lack of physical branches in developing countries. Banks have reshaped their major focuses, moving towards digitalisation and client-oriented solutions.

CASE STUDY: NUBANK AND THE “CHALLENGER” MODEL

The disruption caused by digital banking is best exemplified by Nubank in Latin America. Launched in Brazil in 2013 to combat the high fees and bureaucracy of the country’s oligopolistic banking sector, Nubank operates with zero physical branches. By utilising a cloud-native infrastructure (powered by AWS) and a proprietary real-time decision engine, Nubank reduced its operational costs by approximately 85% compared to traditional incumbents. This efficiency allowed them to offer fee-free credit cards and high-yield savings accounts to millions of previously unbanked Brazilians. As of 2024, Nubank serves over 100 million customers across Brazil, Mexico and Colombia. This case demonstrates that digital banking is not merely about convenience for the wealthy; it is a scalability engine that allows financial institutions to service low-income demographics profitably – something traditional brick-and-mortar banks historically failed to do.

1.4 Consumer Adoption Trends

Initially, consumer adoption of digital banking was slow. Many people were sceptical about security and privacy and did not consider this form of banking fully reliable. However, over time, consumers’ attitudes started to change, driven by greater access to information and growing experience with digital banking worldwide. Technological advancements in the field have also led to acceleration in consumer adoption. The introduction of more intuitive interfaces in mobile applications and web pages, faster transaction processing and continuous access to banking services have enhanced the convenience and usability of digital platforms. Trust in digital channels has substantially increased with the implementation of stronger authentication methods, such as biometrics, and real-time fraud monitoring. The COVID-19 pandemic has compelled customers to explore digital banking due to restricted access to physical branches. As a result, digital banking has evolved from an alternative option to a fundamental expectation in modern financial experiences.

1.5 Future of Digital Banking

According to various studies conducted and real-world trends, digital banking is expected to continue developing, expanding its capabilities and service offerings, attracting more customers and increasingly relying on large-scale data. Generally, banking services are anticipated to become invisible for customers through complete integration into their daily lives. Increased possibilities for personalised experience will emerge as banks enhance their analytical capabilities to provide tailored recommendations and context-aware services. Growing interconnection between digital ecosystems will shift banks towards adaptive and autonomous service models, offering solutions adjusted to individual preferences and changing life circumstances. Overall, over the next few decades, digital banking is likely to advance significantly, forming a foundation for future innovations within the financial industry.

2. AI in Fraud detection, Algorithmic Credit Scoring and Financial Inclusion

The integration of AI and data analytics in fraud detection, credit scoring and their collective role in financial inclusion is fundamentally transforming the finance sector in the world’s economy.

2.1 AI in Fraud Detection and Financial Integrity

The fraudulent activities in financial transaction processes are one of the biggest threats that affect business security; the economic losses are enormous and trust in the financial sector is at its lowest. The situation has been compounded by the shift in operation of business to an online basis given the fact that the number and size of financial transactions have increased significantly. It also presents new challenges which are associated with increased difficulty of identification and prevention of fraud-related activities.

AI, machine learning (ML) and blockchain can be recognised as the best solution to combat these problems. AI and ML act as the tools to crunch big data, recognise complex patterns of fraud and adapt to new and constantly changing strategies that are used by fraudsters in a real-time environment. These technologies can thus help organisations enhance their capabilities to uncover fraud and address them quickly. Blockchain integrates a distributed and unalterable record-keeping system that is an added security and transparency as compared to the conventional approaches.

| Aspect | Traditional Fraud Detection | AI-Based Fraud Detection |

| 1. Detection Method | Rule-based (fixed IF-THEN rules) | Machine learning models that learn from data |

| 2. Flexibility | Rigid; needs manual rule updates | Adaptive; models evolve with new fraud patterns |

| 3. Speed | Often batch-based, delayed detection | Real-time or near real-time monitoring |

| 4. Accuracy | High false positives; limited pattern recognition | Higher accuracy; detects complex and emerging patterns |

| 5. Data Usage | Uses basic transactional data only | Uses behavioural, device, network and multi-dimensional data |

Table 1.

As illustrated in Table 1, the limitations of rule-based systems necessitated an AI-based fraud detection system, the most important being the detection method.

Traditional if-then rule was heavily criticised because of three main reasons:

- Could not detect new fraud patterns;

- High false positives (genuine customers flagged);

- The accumulation of excessive rules created system latency and operational inefficiency.

However, with the introduction of AI and ML models, it can learn from its own mistakes and improve in real time.

Thus, it is safe to say that AI and ML, with its adaptive nature, high accuracy, use of three-dimensional data and real time monitoring speed, can lead to better transparency, make the system accountable and lead to a significant mitigation to corruption and illicit activities in the financial sector.

2.2 Algorithmic Credit Scoring

Traditional credit scoring techniques, which rely on credit history and conventional metrics of financial capabilities, exclude a large part of the population from emerging economies. This exclusion is partly because the pool of borrowers and smaller businesses do not have credit histories, which are imperative to mainstream credit scoring methods.

On this account, many such consumers within these markets are classified broadly as “unbanked” or “underbanked” and, therefore, unable to tap more appropriate and conventional channels of credit and financial services. This exclusion is socially and economically detrimental for an individual to create economic opportunities and for an economy and financial sector to develop.

That is why the application of artificial intelligence can be considered the solution to this challenge. AI thus has capabilities of better and broader credit risk assessment through analysis of other forms of data. Other data, including mobile phone utilisation, social networking sites, utility bills, etc., which are not financial in this particularistic sense, can be utilised as proxies to get a decent dependability on the person’s creditworthiness. These complex phenomena reflect important differences in the business environments and consumer finance. New machine learning methods can process these to build more effective credit scoring systems for emerging economies.

CASE STUDY: TALA AND MOBILE DATA SCORING

A prominent example of this innovation is Tala, a fintech company operating in emerging markets such as Kenya, the Philippines, India and Mexico. Tala addresses the “credit invisible” population by utilising an Android app that analyses behavioural data from the user’s smartphone with their permission. Instead of looking at a bank history, Tala’s AI algorithms examine over 10,000 data points, such as the regularity of calls to family members (which correlates with social stability), the consistency of utility bill payments via SMS and even the daily routes taken by the user. By processing these alternative metrics, Tala has successfully dispensed over $4 billion in micro-loans to millions of customers who previously had no formal credit score, proving that behavioural consistency can effectively predict repayment reliability.

Figure 1: Leveraging AI for Credit Scoring (Kothandapani, 2022).

ADVANTAGES OF ALGORITHMIC CREDIT SCORING

- This system can provide a vast segment of people with an opportunity to receive credit and increase credit possibilities for those who cannot prove their solvency by usual methods. This inclusiveness can help many small players to engage more robustly and contribute more effectively to the markets and, hence, growth.

- Credit assessments will have higher accuracy through more advanced AI models, thus lowering default risks and the general efficiency of lending. In turn, it can build more stability and increase the profitability of lending activities for financial organisations.

However, some issues arise from adopting AI in the credit scoring system. The first one is as every algorithm has its data sources, it can strengthen existing prejudice that should be eliminated, or it can trigger new prejudice in AI, which is unethical. This importance must assume a sound and flexible legal infrastructure to regulate the applicability of AI in the financial industry while safeguarding consumers’ interests and personal information. Moreover, the input and output assets must be optimised for the AI tools, which may be costly in terms of IT infrastructure in resource-scarce environments.

Ultimately, the advantages of algorithmic credit scoring outweigh the disadvantages. Thus, AI-driven scoring is an essential evolution in an era where financial fraud is rampant and the underbanked population remains vast.

2.3 AI and ML as Tools for Financial Inclusion

Beyond credit scoring, AI serves as a multifaceted engine for broader financial inclusion. Two key technologies driving this change are machine learning and natural language processing (NLP).

- Machine learning reduces the “cost to serve” for banks. By automating risk assessment and back-office operations, ML makes it profitable for institutions to serve low-income customers with small account balances, a segment previously considered unviable.

- Natural language processing breaks down literacy and language barriers. NLP-powered chatbots and voice assistants allow users in rural or developing regions to interact with financial services using local dialects and natural speech, rather than complex written forms.

In conclusion, AI technologies hold the potential to expand access to financial services and empower individuals and communities to achieve greater financial security and prosperity. However, it is essential to ensure that AI solutions are developed and deployed in an ethical and responsible manner, with appropriate safeguards in place to protect consumer privacy and mitigate potential biases. By harnessing the power of AI, policymakers, financial institutions and other stakeholders can work towards building more inclusive and resilient financial systems that benefit everyone.

3. Embedded Finance, AI and Real‑Time Cross‑Border Payments

The landscape of global banking is undergoing a paradigm shift from traditional, siloed banking interfaces to “embedded finance” – the seamless integration of financial services into non-financial platforms. This phenomenon is rapidly moving banking into the background of everyday life; consumers now book rides, order groceries and manage freelance work through platforms that handle complex payment flows invisibly. According to recent industry analysis by Bain & Company, the embedded finance market is projected to facilitate over $7 trillion in transaction value by 2026. However, as these platforms increasingly operate on a global scale, they face a critical infrastructure challenge: the reliance on real‑time cross‑border rails to settle transactions between workers, merchants and consumers in different jurisdictions.

The expectation for the digital economy is immediacy. If a ride-hailing app pays a driver instantly in New York, a gig-worker in Manila expects the same speed from a US-based platform. Yet, the traditional cross-border payment architecture – reliant on a complex web of correspondent banks – often operates on T+2 settlement cycles with opaque fees. This latency creates a fundamental friction point for embedded finance. To bridge the gap between user expectations of instantaneity and the realities of international settlement, artificial intelligence has emerged as the critical orchestration layer. AI is no longer just an add-on; it is the central nervous system required to manage risk checks, routing decisions and liquidity forecasting in milliseconds, ensuring that compliance and security do not become bottlenecks for the user experience.

3.1 AI in Real‑Time Cross‑Border Infrastructure and Interoperability

To understand the necessity of AI, one must first examine the inefficiencies of the legacy model. The traditional correspondent banking system relies on Nostro and Vostro accounts – accounts that banks hold with one another to facilitate settlement in foreign currencies. This system is capital inefficient, trapping billions of dollars in “pre-funded” liquidity, and operates largely on serial message processing. For an embedded finance platform, this means a payment might pass through three or four intermediary banks, each deducting a fee and adding a time delay.

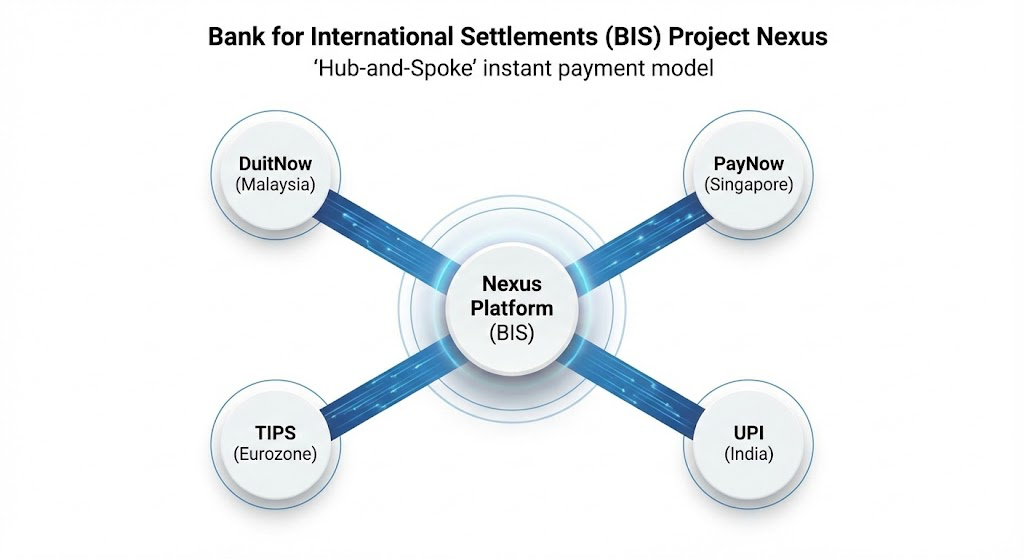

The solution lies in linking domestic Instant Payment Systems (IPS) globally. Project Nexus, a flagship initiative by the Bank for International Settlements (BIS) Innovation Hub, exemplifies this architectural shift. Rather than building bilateral links between every country, Nexus offers a standardised “hub-and-spoke” connectivity model. This allows domestic systems – such as Malaysia’s DuitNow, Singapore’s PayNow and eventually the Eurozone’s TIPS – to interoperate seamlessly.

Figure 2: BIS Project Nexus “Hub-and-Spoke” Model (Google Gemini, 2025).

Within this high-speed architecture, AI serves two critical functions:

- Intelligent Routing and Liquidity Management: AI algorithms analyse volatility in FX markets and liquidity positions across different currency corridors in real-time. They can predict the optimal route for a payment to minimise cost and latency, much like a GPS navigates traffic.

- ISO 20022 Data Enrichment: The global shift to the ISO 20022 messaging standard provides richer, structured data for every transaction. Unlike older formats, which often truncated remittance information, ISO 20022 carries detailed data fields. AI models trained on this granular data can perform “pre-validation”, predicting with high accuracy whether a payment will fail due to incorrect formatting or sanctions screening before it is sent. This drastically reduces the “failed payment” rate, which currently plagues roughly 5% of all cross-border transactions, ensuring the seamless experience embedded finance users demand.

3.2 AI for Financial Integrity in Fragmented Markets

While embedded finance accelerates capital flow, it introduces significant “speed risks” regarding financial crime. In a cross-border context, data silos allow criminals to exploit gaps between jurisdictions. A money laundering scheme might involve “smurfing” (breaking large sums into small, inconspicuous amounts) across accounts in three different countries. In the legacy system, a bank in Country A only sees the initial transfer, and a bank in Country B only sees the receipt, meaning neither spots the criminal pattern.

To counter this, AI utilises graph neural networks (GNNs) to analyse the payment network holistically rather than as isolated transfers. Project Aurora, another pivotal BIS initiative, demonstrated the power of this approach. Project Aurora explored how graph-based models could identify hidden money-laundering structures by treating accounts as “nodes” and payment flows as “links”. By analysing the topology of these connections, the AI can detect complex “mule networks” that traditional rule-based systems miss. In testing, these graph-based models identified approximately twice the number of potential laundering networks compared to standard methods.

However, sharing transaction data across borders triggers complex privacy regulations, such as the GDPR in Europe. To solve this, Project Aurora utilised privacy-enhancing technologies (PETs), specifically federated learning. This approach allows AI models to be trained locally within each institution’s secure environment. Instead of sharing raw customer data (which remains private), the banks share only the updated model parameters (the mathematical learnings). The central AI model aggregates these learnings to become smarter without ever “seeing” the underlying sensitive data. For embedded finance providers, this is a breakthrough: it allows them to plug into a global, AI-driven monitoring framework that preserves user privacy while robustly defending the integrity of the financial system.

3.3 Cross-Border Data Portability and “Credit Passports”

A major limitation in the current global embedded finance ecosystem is the lack of credit history portability. In a globalised economy, labour is mobile; millions of potential borrowers are migrants, international students or cross-border freelancers. When these individuals move to a new country, they often face “thin file” status. Traditional credit bureaus in the host country cannot access their financial history from their home country, effectively resetting their creditworthiness to zero. This information asymmetry forces lenders to treat high-quality borrowers as high-risk, charging exorbitant interest rates or denying service entirely.

AI is bridging this gap through cross-border data portability, creating what are effectively “credit passports”. Unlike the “alternative data” discussed in previous sections (which utilises mobile behaviour), this approach uses AI to translate and standardise existing formal financial data across borders.

Two prominent examples highlight this mechanism:

- Mifundo (Europe): In the European Union, cross-border lending has historically been low due to fragmented data. The fintech Mifundo is building a data layer that standardises credit data across EU member states. Using AI to normalise different scoring methodologies (e.g., how a default is recorded in Germany vs Estonia), it presents lenders with a unified view. They report that this transparency can reduce credit risk for banks by up to a factor of seven, unlocking capital for mobile citizens.

- Nova Credit (Global): On a global scale, Nova Credit has built integrations with major credit bureaus in countries like India, Mexico and the UK. Their “credit passport” technology translates this foreign data into a format that US lenders (like American Express and JPMorgan Chase) can ingest directly into their underwriting models.

In these instances, AI acts as a translation layer, allowing creditworthiness to travel with the user. This capability is fundamental to the mature operation of global embedded finance platforms. It ensures that a software engineer moving from Bangalore to San Francisco can access a credit card or apartment lease immediately upon arrival, integrating them into the financial system of their new home instantly. By enabling this data portability, AI does not just improve banking efficiency; it supports global labour mobility and economic integration.

Thus, the intersection of embedded finance and AI is reshaping the infrastructure of global commerce. By replacing the rigid, slow and siloed legacy systems with agile, AI-driven interoperability, the financial sector is moving toward a future where payments and credit are borderless. From the liquidity management of Project Nexus to the privacy-preserving fraud detection of Project Aurora and the credit mobility of Nova Credit, AI is the engine making financial globalisation a practical reality for the individual user.

4. Risk of AI on Global Financial Institutions

Artificial intelligence has become widely regarded as a phenomenon in the financial world, causing impactful transformations for bankers and causing shockwaves in its ability to transform global financial markets. Artificial intelligence is being utilised in major operations, user interactions and the assessments of danger and risks for a wide degree of people and companies including fintechs and bankers (Aldasoro et al., 2024). These technologies are implemented completely on the premise that they improve efficiency to a large degree and provide a wide array of new services (World Economics Forum, 2025). Looking deeper, it’s interesting to see the large level of dependence that giant financial institutions across the globe have on this and the way that AI reshapes the risk landscape for these financial institutions. This section critically examines the various risks (systemic, operational and governance) that AI imposes on the global financial ecosystem using large banks of data, research and findings (Bank of England, 2025).

4.1 The Systemic Risks Stemming from AI

When we’re looking at systemic risks, we’re looking at how a failure in one part or section of the system can lead to a chain reaction being triggered, potentially causing the failure of the entire system and negative downturns in economic growth and the GDP. One of the key concerns highlighted when focusing on the systemic risks that AI poses is the increased dependence of the financial sector on shared artificial intelligence platforms, data sources that are homogenous and third-party vendors (Financial Stability Board, 2024; Aldasoro et al., 2024). A warning was floated from the financial stability board that market concentration among AI could turn technical failures or cyberattacks that happen internally into widespread obstacles and disruption to the financial market, further progressing as financial institutions globally become exposed to the similar, correlated weaknesses in these systems that are external (Financial Stability Board, 2025).

Figure 3: Systemic Risks of Artificial Intelligence (Google Gemini, 2025).

An example of the systemic risks of AI in this field is if an algorithmic trading platform powered by artificial intelligence failed or malfunctioned, leading to sudden liquidity shocks and stock crashes which could swiftly spread globally due to the ease and efficiency of connection worldwide (Danielsson et al., 2021). High frequency trading powered by AI can also lead to unexpected swings in prices and cause distortions in stock, housing and overall asset pricing, resulting in large alterations to the market stability (Danielsson et al., 2021).

Additionally, when we start to see AI being incorporated into other parts of the financial market, including fraud detection models and credit scoring, there is an increased risk of herding where AI is so largely involved in multiple industries, one attack can cause a drastic impact. This is where we can determine that even though the level of connectedness between various fields as a result of AI is useful, it also increases the risk of problems in a specific industry causing a domino effect and leading to a global crisis (Bank of England, 2025).

4.2 The Data and Algorithmic Risks from AI

It is also important to consider the data and algorithmic risks of an AI-powered financial sector. These include the use of data to create algorithms, as well as privacy violations (World Economic Forum, 2025; Aldasoro et al., 2024).

A variety of data sources can contribute to decision making when artificial intelligence is involved, creating a range of complex problems. As AI is trained on datasets, its outputs can replicate current biases in society, potentially leading to unfair verdicts in the financial market such as loan denial or discriminatory insurance pricing. A prominent example occurred with the Apple Card in 2019, where the credit limit algorithm allegedly offered significantly lower limits to women compared to men with similar credit profiles. This highlights the risk of “proxy discrimination” where algorithms find hidden correlations, leading to unfair outcomes. Therefore, a major focus of organisations must be diverse and high-quality data that represents a range of backgrounds, and AI models must be continuously monitored in case of negative outcomes (Aldasoro et al., 2024).

Data privacy can also bring its own challenges. The centralisation of customer, transaction and behavioural data in AI systems poses significant risks in cybersecurity. This is where cracks in the system, like third-party openings, poor encryption and lapses in internal controls, can cause significant intrusions and even lead to a complete loss of public trust in the financial system.

4.3 Opacity and Explainability Risks

A critical challenge in AI adoption is “black box” opacity. This section examines the black box phenomenon, where human operators struggle to interpret the internal decision-making processes of AI (Maple et al., 2024; World Economic Forum, 2025).

When we look into current AI models with generative or deep learning techniques, we observe how complex decisions are made without explanation. The opacity that arises as a result of this makes it difficult for both external regulators and internal regulators to understand the reasoning behind an AI’s output. If the logic of an AI model cannot be explained, there is an increased risk of financial institutions failing to notice errors and emerging risks, lowering their ability to respond swiftly to untoward conditions (Financial Stability Board, 2024).

The Bank of England chooses to keep in mind that the use of smart, complex artificial intelligence systems brings certain challenges in transparency and oversight, risking the potential for collusion, manipulation and even forms of market abuse (Bank of England, 2025). Financial institutions are asked to have proper documentation on the architecture of their AI models to ensure the transparency of decision making and to help develop tools to aid human decision makers and external regulators in understanding AI outputs (Maple et al., 2024; Aldasoro et al., 2024).

4.4 Cybersecurity and Concentration Risks

When institutions have increased dependence on a smaller pool of AI platforms and various shared platforms, there is an increased risk of market concentration (Aldasoro et al., 2024; Financial Stability Board, 2024). The vulnerabilities in the systems of one company or in critical algorithms could put whole financial markets at risk (World Economic Forum, 2025). The concentration of this not only poses risk during technical incidents but may also lead to competition and innovation being stifled.

This is largely demonstrated in international studies where there may be coordinated attacks to compromise credit scoring systems and various high-level financial processes, such as loan eligibility (Financial Stability Board, 2024; Danielsson, 2021). These attacks on trading models can cause rapid shocks and changes in the market, which may result in rapid selling off and asset freezes across multiple financial markets or the financial market as a whole (Danielsson, 2021). This emphasises the need for investment in proper cybersecurity in this industry, as well as sophisticated levels of high level, multi-layered risk management. It’s also evident that financial institutions should ensure these systems are regularly tested for issues to understand workpoints (European Financial Services Round Table, 2025; Bank of England, 2025).

Figure 4: Concentration Risks (Google Gemini, 2025).

According to 2024 industry reports, financial firms faced a 25% surge in advanced cyberattacks compared to the previous year. Furthermore, reports indicate that nearly 97% of the largest US banks suffered breaches linked to third-party vendors, validating the fear of concentrated supplier risk.

4.5 The Risks of AI in Regulation, Ethics and Governance

The section focuses on three key risks in regulation, ethics and governance: regulatory risks are where changes in regulation may affect a business negatively as a result of AI; ethics risks involve harm to an organisation as a result of a violation in ethical values or standards (Bank of England, 2025; Aldasoro et al., 2024); and governance risks refer to the negative consequences that may occur due to poor internal systems and procedures that govern the management and direction of an organisation.

The implementation of AI in finance has largely been very swift, causing oversight in existing frameworks and gaps in the accountability and documentation of various processes taking place. Internal financial institutions and external regulators may have a hard time keeping up with evolving models; this is further exacerbated by the influx of generative AI and reinforcement learning approaches. This is where the SUERF policy brief comes into play, providing a clear framework of recommendations such as:

- Assigning clear roles and responsibilities for AI monitoring in the organisation.

- Ensuring regular audits and external review of artificial intelligence systems.

- Providing channels for customers to challenge AI-based decisions.

- Coordinating internationally to ensure this does not become an issue.

There has also been a request for further research on the topic, calling for regulators to focus on traditional policy objectives, creating new mandates around data privacy, algorithmic bias and the various economic impacts of AI-driven automation. It is largely recommended that these policy makers test their systems for various scenarios (Aldasoro et al., 2024).

5. Main Results

Based on the qualitative synthesis of industry reports and case studies, this research identifies six primary findings regarding the integration of AI in global finance:

- AI dramatically enhances fraud detection. Machine learning and network-based models (such as graph neural networks) detect complex fraud patterns in real time. These systems significantly outperform traditional rule-based methods, strengthening financial integrity against sophisticated money laundering networks.

- Algorithmic scoring expands financial inclusion. By analysing alternative data (e.g., mobile usage and utility payments) and cash-flow behaviour, AI enables accurate credit assessments for the “unbanked” and migrant populations. This approach, exemplified by firms like Tala, reduces default risks while democratising access to capital.

- Digital banking is the gateway to access. With over 3.6 billion users globally, digital banking has transitioned from a convenience to a necessity. The shift to API-first and cloud-based platforms has reduced operational costs and widened financial access to previously underserved regions.

- Real-time cross-border payments are scalable but fragile. Initiatives like the BIS Project Nexus demonstrate that AI can enable scalable interoperability between national payment systems. However, the requirement for millisecond-level screening introduces new operational vulnerabilities and cyber risks.

- Emergence of new systemic risks. The sector’s heavy reliance on a concentrated group of shared AI models and cloud providers increases “correlation risk”. This creates the potential for algorithmic herding, where simultaneous model failures could destabilise the broader market.

- The “black box” governance challenge. Data quality issues and model opacity remain critical barriers. AI systems risk perpetuating historical biases, and their complexity limits auditability. This necessitates a shift toward “macro-prudential” regulation that focuses on transparency and explainability.

Conclusion

The global financial system is undergoing a structural shift in which artificial intelligence has moved from the periphery of operations to the core of how trust, risk and creditworthiness are managed across borders. AI‑powered fraud detection and algorithmic credit scoring now underpin the growth of digital banking, embedded finance and real‑time cross‑border payment rails. At the micro level, these systems deliver tangible gains: they enable millisecond‑level screening on high‑velocity networks, detect complex fraud patterns that human and rules‑based systems routinely miss, and open new avenues for financial inclusion by extending credit and payment access to customers, merchants and regions historically ignored by traditional banking models.

Yet these same technologies also reconfigure systemic risk in ways that existing prudential frameworks are not fully prepared to address. Embedded finance blurs the boundaries between banks, fintechs, big techs and non‑financial platforms, creating a dense ecosystem of interconnected services that rely on shared data, common AI tooling, and concentrated cloud and infrastructure providers. As institutions converge on similar models, datasets and vendors, the financial system drifts toward algorithmic monoculture: correlated model errors, synchronised risk responses and large‑scale algorithmic herding become not just possible but likely in periods of stress. In such a landscape, what appears as micro‑prudential improvement (e.g., more accurate fraud filters and sharper risk scores) can paradoxically increase macro‑systemic fragility.

Data quality, embedded bias and model opacity further deepen this tension. If the data that fuels AI systems mirror historical exclusion or geopolitical imbalance, and if the resulting models operate as opaque black boxes, the outcomes are both unfair and potentially destabilising. Bias in algorithmic credit scoring can scale into structural exclusion of particular regions, demographics or cross‑border flows, while opaque fraud models can silently reshape transaction patterns and liquidity routes. Combined with real‑time payment architectures that leave little room for manual oversight, these properties create tightly coupled, high‑speed systems in which small design flaws or shocks can propagate quickly across institutions and jurisdictions.

The central challenge, therefore, is not whether AI should be integrated into global finance, but how to govern this integration so that its stabilising features outweigh its destabilising potential. Meeting this challenge requires a distinctly macro‑prudential approach to AI. Regulators and policymakers must look beyond individual model performance to focus on model convergence, infrastructure concentration and cross‑border dependencies. They will need to promote diversity in modelling approaches and data sources, mandate robust transparency and auditability standards, and design stress tests that explicitly account for AI‑driven behavioural dynamics under stress scenarios. At the infrastructure level, resilience demands redundancy in cloud and service providers, well‑defined failover strategies and coordinated incident response mechanisms spanning borders and institutional types.

If these governance, technical and regulatory safeguards are put in place, AI can function not as an opaque and fragile backbone for embedded finance, but as a disciplined, adaptive infrastructure that strengthens the integrity of cross‑border financial flows. The future of AI‑driven digital banking and embedded finance will be decided not only by computational advances, but by whether global institutions choose to design for diversity, transparency and resilience rather than speed and efficiency alone. Done well, AI can anchor a more inclusive, efficient and robust global financial system; done poorly, it risks becoming a tightly coupled, algorithmic substrate through which localised errors and biases scale into systemic crises. The task ahead is to deliberately choose the former path.

Bibliography

Aldasoro, I., Gambacorta, L., Korinek, A., Shreeti, V., Stein, M. (2024) Financial intelligence: opportunities and risks of AI in finance, SUERF The European Money and Finance Forum [online]. <https://www.suerf.org/publications/suerf-policy-notes-and-briefs/financial-intelligence-opportunities-and-risks-of-ai-in-finance/>

Bank for International Settlements (2023) Project Aurora: the power of data, technology and collaboration to combat money laundering across institutions and borders, BIS [online]. <https://www.bis.org/about/bisih/topics/fmis/aurora.htm>

Bank for International Settlements (2024a) Project Nexus: enabling instant cross-border payments, BIS [online]. <https://www.bis.org/about/bisih/topics/fmis/nexus.htm>

Bank for International Settlements (2024b) Project Nexus: enabling instant cross-border payments, BIS Other Publications No. 86 [pdf]. <https://www.bis.org/publ/othp86.pdf>

Bank of England (2025) Financial Stability in Focus: Artificial intelligence in the financial system, Bank of England [online]. <https://www.bankofengland.co.uk/financial-stability-in-focus/2025/april-2025>

Burnett, S. & Kinder, K. (2025) Online Banking Usage Statistics 2025: Adoption, User Insights, and Security Innovations, CoinLaw [online]. <https://coinlaw.io/online-banking-usage-statistics/>

Danielsson, J., Macrae, R. & Uthemann, A. (2022) Artificial intelligence and systemic risk, Journal of Banking and Finance, 140, 106290.

Decta (2024) Pros and Cons of Digital Banks vs Traditional Banks, Decta [online]. <https://www.decta.com/company/media/pros-and-cons-of-digital-banks-vs-traditional-banks>

European Commission (2024) Verified and Passportable Financial Identity, EU-CREDIT-AI, CORDIS 101188940 [online]. <https://cordis.europa.eu/project/id/101188940>

European Financial Services Round Table (2025) EFR White Paper on Security Risks in Artificial Intelligence for Finance, EFR [pdf]. <https://www.efr.be/media/qj0fvgjk/159-2-efr-white-paper-on-ai-security-risk-april-2025.pdf>

Financial Stability Board (2024) The Financial Stability Implications of Artificial Intelligence, FSB [pdf]. <https://www.fsb.org/uploads/P14112024.pdf>

Hall, I. (2023) BIS-led cross-border instant payments project progresses, Global Government Fintech [online]. <https://www.globalgovernmentfintech.com/project-nexus-cross-border-instant-payments-project-progresses/>

Kothandapani, H.P. (2022) Leveraging AI for credit scoring and financial inclusion in emerging markets, World Journal of Advanced Research and Reviews, 15(3), pp. 526-539.

KPMG (2019) The Future of Digital Banking, KPMG [pdf]. <https://assets.kpmg.com/content/dam/kpmg/ua/pdf/2019/09/future-of-digital-banking-in-2030-cba.pd.pdf>

Kristjansson, G. (2023) Charting a New Course Against FinCrime: BIS Innovation Hub and Lucinity Successfully Conclude Project Aurora, Lucinity [online]. <https://lucinity.com/blog/project-aurora>

Kshetri, N. (2021) The Role of Artificial Intelligence in Promoting Financial Inclusion in Developing Countries, Journal of Global Information Technology Management, 24(1), pp. 1-6.

Maple, C., Szpruch, L., Epiphaniou, G., Staykova, K., Singh, S., Penwarden, W., Wen, Y., Wang, Z., Hariharan, J. & Avramovic, P. (2024) The AI Revolution: Opportunities and Challenges for the Financial Sector, arXiv: 2308.16538.

Meniga (n.d.) Traditional Banking Vs. Digital Banking: Key Differences, Meniga [online]. <https://www.meniga.com/guides/traditional-banking-vs-digital-banking/>

Rahman Akash, T., Reza, J., Merrett, L. & Arefin Sourav, S. (2024) Fortifying Financial Integrity: Advanced Fraud Detection Techniques for Business Security, World Journal of Advanced Research and Reviews, 24(3), pp. 1032-1041.

Velazquez, E. (2025) Responsible cross-border lending: why banks must act now, Mifundo [online]. <https://www.mifundo.com/news/responsible-cross-border-lending-why-banks-must-act-now>

World Economic Forum (2025) Artificial Intelligence in Financial Services, WEF [White Paper]. <https://reports.weforum.org/docs/WEF_Artificial_Intelligence_in_Financial_Services_2025.pdf>

Research Integrity Statement: Grammarly and Google Gemini were utilised to support proofreading and linguistic refinement. These tools were not used for generating original academic content or research analysis but only for grammar correction and clarity improvements.

{kind=link}