Abstract

This paper examines how the U.S.-China strategic rivalry is reshaping the norms and institutions of global trade governance, with a focus on tariffs, currency competition and semiconductor export controls. These cases illustrate the fusion of national security with economic statecraft, reshaping global supply chains and accelerating the emergence of rival technological ecosystems. Drawing on historical context and case study analysis, the study investigates the mechanisms through which state competition alters both the instruments of economic statecraft and the legitimacy of multilateral institutions. The findings suggest that the semiconductors industry underscores the growing fusion of security and trade policy. Tariff disputes indicate weakening confidence in international organisations like the World Trade Organization. These trade conflicts reveal how protectionist measures are weaponised as instruments of geopolitical leverage, undermining the credibility of multilateral arbitration and exposing the fragility of the rules-based trade system. Currency competition displays the influence of the U.S. dollar in geopolitical procedures in the face of the gradual internationalisation of the Chinese renminbi, exposing vulnerabilities in the future dollar-centric system. The paper concludes that these dynamics are driving a shift toward a fragmented, bifurcated order, raising the prospect of alternative governance frameworks that challenge the existing liberal trade regime.

Introduction

Since the end of the Second World War, global trade governance has been structured around liberal economic principles, multilateral institutions and the presumption that economic interdependence would generate stability. Institutions such as the World Trade Organization (WTO), International Monetary Fund (IMF) and the World Bank sought to embed the norms of free trade, nondiscrimination and dispute resolution within a rules-based framework. The United States (U.S.), as the hegemon of the post-war order, acted as both architect and guarantor of these institutions, using its technological leadership, tariff reductions and currency dominance to sustain an integrated global economy. For decades, this system contributed to unprecedented growth and interdependence, enabling global supply chains and lowering transactional costs.

The U.S. dollar became the financial cornerstone of this system, representing 58% of global foreign exchange reserves while serving as the foundation of international trade and the global financial market. Its centrality has been reinforced not only by market trust but also the institutional strength of the United States, including the Federal Reserve, the Treasury and the broader regulatory framework that underpins global confidence in the dollar. Yet, in recent years, China has sought to challenge this dominance by globalising the use of renminbi (RMB) as part of a broader effort to reshape international financial governance. Through initiatives such as the Belt and Road Initiative (BRI), bilateral currency agreements and alternative payment systems such as CIPS, Beijing has attempted to expand the reach of the RMB. Although the RMB currently accounts for just 5% of global foreign exchange reserves, its trajectory reveals an ambition to provide states and firms with alternatives to the US-led order, raising questions about whether the future of global trade and finance will remain anchored to the dollar or gradually shift towards a multipolar currency system.

Semiconductors have become the defining strategic commodity of the 21st century for their centrality to the digital economy, advanced manufacturing, artificial intelligence (AI) and defence. The United States has long dominated the sector through firms such as Intel, Nvidia and Qualcomm, supported by its control of key intellectual property, design tools and fabrication technologies. Taiwan and South Korea, with TSMC and Samsung, further reinforce U.S. influence through their near-monopoly in advanced chip production. China, however, has sought to reduce dependence by investing in firms like SMIC and state-backed funds aimed at self-sufficiency. Yet U.S. export restrictions on lithography, design software and high-performance chips continue to limit Chinese progress, turning semiconductors into both a choke point and an instrument of leverage. This struggle reshapes global trade norms by intertwining economic interdependence with national security.

Tariffs are set term taxes on imports of specified goods or from certain countries. Domestic products can better compete with cheaper international imports if tariffs are levied. Tariffs have become one of the most visible tools of the U.S.-China rivalry, disrupting the WTO’s principles of free trade and rule-based arbitration. The Trump administration imposed tariffs on over $360 billion of Chinese goods, citing intellectual property theft and unfair trade practices, while China retaliated with duties on U.S. exports such as soybeans. Rather than resolving disputes multilaterally, both powers weaponised tariffs in politically sensitive sectors, signalling a shift from liberalisation to protectionism. Even under Biden, most tariffs remain, underscoring their role as structural features of global trade governance and weakening the credibility of WTO norms.

The U.S. dollar remains the dominant global currency, accounting for about 58% of foreign exchange reserves and anchoring global trade and finance through its control of central financial institutions, as illustrated by SWIFT’s management of international transactions. Meanwhile, China has endeavoured to expand the influence of the RMB via the Belt and Road Initiative, bilateral currency agreements and its CIPS payment system. While the RMB represents only about 5% of global reserves, these efforts signal Beijing’s ambition to challenge dollar hegemony and raise the question of whether it can reshape financial norms long defined by the United States.

This study seeks to fill this gap by examining the ways in which the U.S.-China strategic rivalry reshapes the norms and institutions of global trade governance, with a specific focus on tariffs, currency domination and semiconductors. By analysing these three interlinked domains, the study aims to reveal how material competition translates into normative change and institutional reconfiguration. The central objective is to demonstrate that the rivalry is not simply disrupting the global trade order, but is actively forging new patterns of governance that will influence international economic relations well into the future.

Semiconductors

Semiconductors have emerged as the most contested terrain in the U.S.-China strategic rivalry, not only because of their intrinsic technological value but also because of the extent to which they underpin global trade, finance and security systems. Unlike tariffs, which stress-test existing systems, or currency competition, which shifts long-standing foundations, semiconductors represent a transformative disruption to the norms and institutions of global trade governance. The global semiconductor industry has been described as one of the most complex supply chains in existence, requiring transnational cooperation across research, design, raw material processing and advanced manufacturing. At the same time, it is marked by an extreme degree of geographic concentration: the United States dominates intellectual property and chip design, Taiwan and South Korea lead in fabrication, the Netherlands holds a monopoly over extreme ultraviolet lithography machinery, and China represents both the largest consumer market and a rapidly advancing manufacturing base. This asymmetry means that semiconductors function both as the world’s most critical enabling technology and as a flashpoint for systemic rivalry between the two largest economies.

The semiconductor conflict is illustrative of how trade governance is being reshaped. Institutions like the WTO, which were designed to regulate tariffs and traditional goods, have little precedent for governing access to high-tech intellectual property, export restrictions and supply-chain chokepoints. The U.S. has increasingly bypassed multilateral institutions in favour of unilateral and plurilateral strategies to restrict China’s semiconductor ambitions. This was visible in the 2019 placement of Huawei and other Chinese firms on the U.S. Entity List, which barred them from acquiring critical U.S.-made chips and software. Later, the Biden administration expanded these restrictions, introducing sweeping export controls in October 2022 that prohibited the sale of advanced semiconductors and semiconductor manufacturing equipment to Chinese firms. These measures not only constrained China’s domestic capacity to innovate but also directly challenged the WTO’s underlying principle of nondiscrimination in trade, demonstrating that national security and geopolitical rivalry now supersede multilateral rules when it comes to technology.

China, for its part, has responded with a dual strategy of resistance and self-reliance. Initiatives such as “Made in China 2025” and its broader industrial policies funnel billions into the development of domestic semiconductor capabilities. While Chinese firms lag significantly behind in producing cutting-edge logic chips, the government has accelerated investment in mature node production and memory chips, while simultaneously attempting to localise supply chains for raw materials and equipment. This pursuit of “indigenous innovation” reflects a structural departure from the liberal trade order that assumed global interdependence would drive cooperation. Instead, the semiconductor rivalry is forcing a decoupling of supply chains, as both Washington and Beijing reorient their trade strategies toward resilience, redundancy and strategic autonomy (Sutter, 2024).

The implications extend beyond the bilateral relationship. U.S. restrictions are extraterritorial in nature, applying not only to American firms but also to foreign companies that use U.S. technology, such as Taiwan’s TSMC and the Netherlands’ ASML. This creates friction within the global trade system, as allies are pressured into compliance with U.S. security-driven policies, even when such policies conflict with their commercial interests. At the same time, it illustrates a shift in trade governance toward coalition-based rulemaking, as seen in initiatives like the “Chip 4” alliance among the United States, Taiwan, South Korea and Japan (Xing, 2021). These arrangements bypass the WTO framework and instead create exclusive technology blocs, which risk fragmenting the global economy into rival spheres of influence.

Semiconductors also demonstrate how economic rivalry is spilling over into institutional innovation. China has sought to expand alternatives to Western-dominated governance structures by mobilising organisations like the BRICS New Development Bank and by promoting forums such as the Regional Comprehensive Economic Partnership (RCEP). These institutions may lack the enforcement power of the WTO or OECD, but they represent attempts to craft alternative norms of cooperation that reduce dependence on Western supply chains. Meanwhile, U.S. engagement with institutions like the OECD and IMF is increasingly leveraged to emphasise transparency, investment security and restrictions on state subsidies, which are often directed at Chinese industrial policies (Xing, 2021). The semiconductor case thus shows how both powers are leveraging institutional networks to redefine global norms of trade governance in ways that privilege strategic security over free-market orthodoxy.

Perhaps most importantly, semiconductors reveal how strategic rivalry is altering the very conception of globalisation. The traditional model of comparative advantage assumed that countries would specialise in different parts of production and trade freely across borders. Semiconductors once epitomised this logic, with highly specialised nodes of production distributed across East Asia, North America and Europe. The U.S.-China rivalry, however, is replacing interdependence with securitised interdependence, where trade is conditional on political alignment and strategic trust. This represents not merely a disruption of supply chains but a structural reordering of global trade norms, where technology is reclassified as a security-sensitive resource akin to energy or defence equipment.

The semiconductor struggle is, therefore, not just an industrial contest but a transformative case study in how strategic rivalry reshapes governance. It tests the capacity of existing institutions to handle dual-use technologies, accelerates the creation of new alliances and blocs, and redefines the balance between free trade and national security. As Washington and Beijing continue to escalate their contest for semiconductor dominance, the norms and institutions of global trade governance are being rewritten in ways that extend far beyond chips, with implications for tariffs, currency regimes and the very future of globalisation itself.

Tariffs

Whereas semiconductors represent a transformative disruption to supply chains and technology governance, tariffs stress-test the very foundations of trade liberalisation. Tariffs expose the fragility of the norms of liberalism and the institutions like the World Trade Organization (WTO) that were designed to arbitrate disputes and prevent unilateral escalation. The post-war economic order was built on the assumption that gradual reductions in tariffs would facilitate interdependence, yet in the case of U.S.-China relations, tariffs have become tools of coercion, retaliation and strategic leverage, reshaping both norms and practices within global trade governance.

In the late 19th and early 20th centuries, tariffs became central to both domestic policy and diplomacy as the United States’ industrial sector expanded. The Chinese Exclusion Act of 1882, which restricted Chinese immigration, coincided with one of the first broader efforts by the U.S. to protect its labour markets and industries while simultaneously pursuing access to China’s markets through the Open Door Policy (U.S. St. Dep., Office of the Historian, 1949). While high tariffs bolstered American industries, they limited Chinese exports, particularly in labour-intensive goods like textiles. This balance illustrates how U.S. policy at the time aimed to restrict Chinese labour and products domestically, while still benefitting from Chinese consumers abroad, resulting in a highly advantageous trade balance from their early history. Later in the 1970s, Jimmy Carter normalised relations and reopened the path for trade. China’s eventual entry into the World Trade Organization (WTO) in 2001 marked its integration into the global trading economy. The U.S. then granted China Permanent Normal Trade Relations status in 2000, which drastically lowered tariffs on Chinese goods until recently (Library of Congress, 2025).

The trade war launched in 2018 under the Trump administration marked a decisive turning point. Invoking Section 301 of the Trade Act of 1974, the United States imposed tariffs on over $360 billion worth of Chinese imports, citing unfair trade practices, intellectual property theft and systemic state subsidies. China responded with tariffs on U.S. goods worth approximately $110 billion, targeting politically sensitive sectors such as agriculture to maximise domestic political pressure. This escalation undermined the credibility of WTO dispute settlement mechanisms, as both powers pursued unilateral measures rather than submitting to multilateral arbitration. The WTO, designed to function as a neutral arbiter of tariff disputes, found itself sidelined, illustrating how great-power rivalry can override institutional authority. In doing so, the tariff conflict demonstrated that the liberal rules-based order is not only being challenged by emerging powers but is also being reinterpreted and reshaped by its original architect, the United States.

What makes tariffs particularly significant in this rivalry is their symbolic role in redefining the boundaries between economics and politics. Historically, tariffs were primarily economic instruments designed to protect domestic industries or generate revenue. In the U.S.-China context, however, tariffs have been repurposed as tools of strategic competition, explicitly linked to issues of national security, technological leadership and industrial resilience. The Biden administration, despite its rhetorical commitment to multilateralism, has chosen to maintain and even expand many of the tariffs initiated under Trump, signalling bipartisan consensus in Washington that tariffs now constitute a permanent feature of the rivalry rather than a temporary bargaining chip. This institutionalisation of tariffs as a geopolitical instrument marks a departure from decades of U.S. leadership in tariff reduction and signals a broader shift toward protectionist governance within the global economy.

One of the Trump administration’s main goals of the “reciprocal tariffs” was to pull production from overseas, mainly Asia, back to the U.S. market by increasing taxes on those imports, giving an incentive for American companies to manufacture domestically. They hoped to accelerate the trend of nearshoring; however, evidence from 2025 is mixed. Many experts do not believe in its viability. FDI data show strong momentum into Mexico, consistent with a North American nearshoring thesis, including record Q1 2025 inflows of cash, and United Nations Trade and Development’s (UNCTAD) data showing that North America saw rising inflows in 2024 even as global FDI fell (UNCTAD, 2025; Izaza & Flores, 2025). At the same time, the reshoring index dipped sharply, cautioning that U.S. manufacturing has not yet caught up to cheaper Asian manufacturing. In short, policy is shifting towards nearshoring, but production does not increase as rapidly as policy interacts with costs, logistics and market access (UNCTAD, 2025). The Trump administration had also reduced tariffs during negotiations with China to reduce tensions during two consecutive tariff truce periods lasting between May and November 2025. Rather than the higher tariffs previously applied, this preserves the option to increase them again if talks stall (White House, 2025A). This temporary de-escalation is designed to encourage companies to reshore, without triggering an abrupt shock to inventories. Overall, tariffs are one of the most important tools for the nearshoring and reshoring processes, as they apply pressure for more favourable trade conditions and make domestic products more competitive.

Another goal of the White House was to use tariffs as leverage in negotiations: tariffs would be increased or decreased to pressure countries into agreeing to more favourable market access, subsidies or technology transfer (USTR, 2025). The administration presented the truce period as a concession to get a better trade agreement, while still maintaining the possibility of reinstating higher tariff rates (White House, 2025B). While the U.S. was imposing tariffs on China, they applied retaliatory tariffs on agricultural purchases, which also served as leverage. Reports in late August 2025 highlighted the renewed discussion of removing soybean and agricultural tariffs in Washington-Beijing negotiations, along with other long-standing tariffs that the Trump administration is looking to eliminate. The “tariffs as an accelerator” strategy aligns with the Trump administration’s belief that international organisations, such as the WTO, were too slow due to their lengthy and sometimes ineffective processes, and couldn’t pressure other countries to make advantageous deals with the United States.

China’s response has also reshaped the global trade landscape. While retaliatory tariffs hit U.S. exporters hard, particularly in the agricultural sector, Beijing simultaneously sought to diversify its trade relationships by deepening ties with partners in Asia, Africa and Europe. Agreements such as the Regional Comprehensive Economic Partnership (RCEP) and expanding Belt and Road Initiative (BRI) networks were designed to mitigate dependency on the U.S. market, embedding China more deeply into regional trade governance frameworks. In this sense, tariffs did not only generate bilateral friction but also incentivised systemic realignment, where alternative trade blocs emerged as partial substitutes for a fractured global trading order. The tariff conflict thus catalysed institutional pluralism, with both Washington and Beijing seeking to reshape the rules of trade through competing coalitions and frameworks.

The extraterritorial effects of tariff escalation are equally profound. Global supply chains, which had been optimised under WTO-era rules, were forced to adjust to the unpredictability of tariff shocks. Firms responded by relocating production bases, diversifying sourcing or engaging in “tariff engineering” to avoid punitive duties. This erosion of predictability undermined one of the central pillars of global trade governance: the assumption of stability and transparency in market access. By introducing systemic uncertainty, tariffs compelled both states and corporations to prioritise flexibility and resilience over efficiency, thereby altering the normative expectations of global commerce.

At the institutional level, the tariff conflict exposed the limitations of the WTO’s ability to discipline great powers. Although the WTO ruled against U.S. tariffs on Chinese goods in 2020, Washington effectively ignored the decision, claiming that existing rules were inadequate to address Beijing’s state-led economic model. This refusal to comply highlighted a structural gap in global trade governance: the inability of multilateral institutions to enforce norms when major powers view compliance as incompatible with strategic interests. As a result, tariffs have accelerated a shift toward unilateral and plurilateral governance, where coalitions of states set their own rules rather than relying on universal institutions.

Most critically, tariffs demonstrate how the U.S.-China rivalry has redefined the normative legitimacy of trade protectionism. For decades, protectionism was viewed as a deviation from global norms, to be gradually eliminated through liberalisation. Today, however, tariffs are increasingly normalised as legitimate instruments of national security and geopolitical competition. This normalisation has broader systemic consequences: it signals to other states that unilateral protectionist measures are permissible, thereby weakening the universality of WTO rules and encouraging emulation by middle powers. The tariff conflict thus not only reshapes bilateral relations but also transforms the collective expectations of how trade governance operates in a multipolar world.

The evolution of tariffs in the U.S.-China rivalry is therefore not just a question of economic cost or trade diversion. It reflects a deeper transformation in global trade governance, where norms of liberalisation are supplanted by norms of strategic protectionism, and where institutions once tasked with ensuring free trade are increasingly bypassed by unilateral or bloc-based arrangements. Much like semiconductors, tariffs demonstrate that the rivalry is not simply disrupting the existing order – it is actively rewriting the rules, introducing a governance framework where coercion, security and political leverage are central to trade relations. As tariffs continue to be wielded not as temporary measures but as embedded instruments of rivalry, they reveal the extent to which global trade governance has shifted from cooperative liberalism to competitive fragmentation.

Domination of the U.S. Dollar

HISTORICAL CONTEXT

To understand how the U.S.-China rivalry reshaped global trade governance, it is necessary to revisit the historical foundations of the U.S. dollar’s dominance. In the aftermath of World War II, the United States emerged as the unrivalled economic power, holding nearly two-thirds of the world’s monetary gold stock (Bordo & Eichengreen, 1993). With this concentration of wealth, the United States spearheaded the creation of the Bretton Woods System in 1944, designed to ensure stable global economic conditions after the war. Under this arrangement, most currencies were fixed to the U.S. dollar, which was in turn convertible into gold. The framework reduced exchange rate volatility, stabilised trade and encouraged investment across borders.

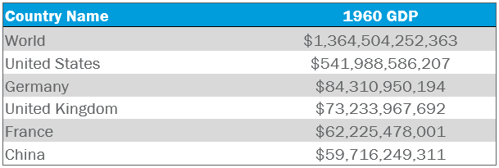

The Bretton Woods institution – the World Bank and the International Monetary Fund (IMF) – extended this system beyond monetary policy. The IMF provided liquidity support and surveillance to stabilise exchange rates, while the World Bank financed post-war reconstruction and development. These institutions not only embedded the U.S. dollar as the backbone of international finance but also projected American influence into global governance. By 1960, the United States accounted for nearly half of world GDP (see Table 1), a striking measure of its ascendancy.

Table 1: Country GDP in 1960 (Bordo & Eichengreen, 1993).

Yet the system’s rigidity revealed weaknesses. As more countries accumulated dollars, U.S. gold reserves thinned, undermining convertibility. In 1971, President Nixon ended the dollar’s link to gold, with fixed exchange rates removed altogether in 1973. The collapse demonstrated how American dominance was simultaneously stabilising and constraining, a reflection of hegemonic stability theory. The dollar’s primacy, while fostering growth, limited monetary flexibility elsewhere and concentrated power in Washington.

THE U.S.’ STRATEGIC USE OF THE DOLLAR

The dollar’s dominance has persisted far beyond Bretton Woods, increasingly serving as a strategic instrument of American power. Its use in sanctions, technological restrictions and financial messaging systems highlights how economic primacy intersects with geopolitics.

Following Russia’s invasion of Ukraine in 2022, the United States, European Union and allies deployed dollar-based sanctions to support Ukraine. These sanctions immobilised €300 billion of Russian Central Bank reserves, directly constraining Moscow’s war financing. Russia’s economy subsequently contracted: GDP declined by 2.1% in 2022, with a further 2.5% fall in 2023, while monthly oil revenues dropped by as much as 41.7% compared to the previous year (Council of the European Union, 2023). Such figures underline the capacity of dollar-centric sanctions to erode both economic and geopolitical power by targeting revenue streams and international trade flows.

The dollar also underpins U.S. leverage in technology governance. In 2019, Washington imposed restrictions on Huawei, cutting its access to semiconductors, essential for 5G devices. This measure extended beyond corporate rivalry, as the U.S. persuaded European allies to block Huawei’s participation in their networks, citing security concerns. The result was a significant slowdown in China’s technological ascent, consolidating U.S. influence over global innovation and digital infrastructure.

Finally, U.S. dominance extends through financial messaging networks. The Society for Worldwide Interbank Financial Telecommunication (SWIFT) processes most global transactions, many denominated in dollars. As Wade (2024) observes, this institutional leverage grants Washington a gatekeeping role over international finance. Such control enhances the dollar’s utility as an instrument of statecraft, discouraging alternatives and reinforcing dependence on US-centred systems.

CHINA’S RMB INTERNATIONALISATION STRATEGY

Confronted with these constraints, China has embarked on a deliberate strategy to internationalise the RMB. This effort spans infrastructure projects, bilateral trade agreements, institutional reforms and reserve currency recognition.

The Belt and Road Initiative, launched in 2013, epitomises this strategy. Extending across 147 countries, the BRI invests in railways, pipelines and digital infrastructure, including 5G networks (McBride, Berman & Chatzky, 2023). These projects, often financed in RMB, expand its use in global trade while binding recipient states closer to China. Unlike World Bank loans, which emphasise regulatory standards and ESG compliance, the BRI offers fewer conditions, increasing its appeal to developing economies (World Bank Group, 2022). In turn, the RMB gained traction as a functional alternative in international commerce.

Bilateral trade agreements further strengthen this trajectory. In 2023, China and Brazil agreed to settle trade in RMB and reals, bypassing the dollar; Argentina soon after announced it would pay for imports from China in RMB (Von Beschwitz, 2024). Such arrangements, though still modest in scale, demonstrate China’s success in normalising non-dollar settlements.

China also built institutional frameworks to complement this expansion. The Cross-Border Interbank Payment System (CIPS) facilitates RMB transactions, offering an alternative to SWIFT. The IMF’s 2015 decision to include the RMB in the Special Drawing Rights basket marked recognition of its “freely usable” status (Lagarde, 2016). Nonetheless, limitations remain: the RMB accounts for less than 5% of SWIFT payment denominations and only 2% of international reserves, while CIPS volumes remain a fraction of SWIFT (Hofman, 2025). These constraints temper expectations of rapid displacement of the dollar, but they underscore China’s steady push toward currency diversification.

THE EMERGING MULTIPOLAR CURRENCY ORDER

The U.S. dollar remains entrenched, representing 58% of global foreign exchange reserves (Standard Chartered, 2025). Its liquidity, stability and institutional backing provide resilience unmatched by any competitor. Yet the cumulative impact of sanctions, financial weaponisation and diversification efforts has sparked momentum toward de-dollarisation.

The Ukraine war accelerated this trend. Russia and its partners turned increasingly to the RMB, doubling its share of trade finance payments from 4% to 8% by late 2023 (Gopinath, 2024). Simultaneously, the rise of bilateral settlements and the growth of CIPS transactions signalled a willingness by states to bypass dollar channels. These shifts hint at the gradual emergence of a multipolar currency system.

A multipolar order could bring significant benefits for smaller states. Diversifying reserves across multiple currencies would reduce exposure to the political and economic risks associated with U.S. dominance, while enhancing policy autonomy. At the same time, it could stabilise financial markets by dispersing systemic vulnerabilities. Yet such a transformation would also challenge existing institutions like the IMF and World Bank, which rely heavily on the dollar as their foundation. To adapt, they would require deep reforms in governance and operational frameworks, balancing multiple centres of financial power.

The rivalry between the U.S. dollar and China’s RMB reflects a contest not only over monetary dominance but over the structure of global governance itself. The U.S., building on its post-war ascendancy, continues to wield the dollar as both an economic foundation and a geopolitical instrument. China, through initiatives like the BRI, bilateral agreements and institutional innovation, has made incremental progress toward RMB internationalisation. While the dollar remains dominant, the steady rise of alternatives points to the possibility of a multipolar currency order. Whether this order materialises will depend on the resilience of existing institutions and the willingness of states to embrace financial diversification, signalling a potential transformation in the future of global economic governance.

Conclusion

The findings of this study suggest that the U.S.-China economic rivalry is no longer confined to isolated disputes but reflects a structural reordering of the global economy. Across trade, currency and semiconductors, competition has become both systemic and strategic, with each domain reinforcing the other. Tariff conflicts revealed how national governments are willing to sacrifice efficiency for leverage; currency tensions showed the limits of dollar dominance and the tentative risk of alternatives; and semiconductor restrictions illustrated the profound security stakes embedded in economic policy. Taken together, these dynamics underscore a key takeaway: the global economic system is shifting toward greater politicisation, where markets and technology are no longer neutral spaces but arenas of power contestation. The interdependence once assumed to guarantee stability now creates vulnerabilities that states seek to manage through protection, control and rivalry.

Although a growing body of scholarship has examined U.S.-China competition on trade, technology and finance, the literature remains fragmented in two important respects. Firstly, most analyses treat tariffs, currency and semiconductors in isolation, without sufficiently interrogating how they interact as independent sites of governance transformation. Secondly, existing research often emphasises policy outcomes, such as trade diversion or exchange rate stability, while paying less attention to how the rivalry is reconstituting the normative and institutional fabric of global trade governance itself. In short, while we know much more about what the rivalry produced in economic terms, we know less about how it reshapes the rules, standards and expectations that underpin the system. This gap is especially pressing given that norms, once altered, can structure the behaviour of states and markets for decades.

Future research must therefore examine not only the outcomes of this rivalry but also the mechanisms that might sustain cooperation in an increasingly fragmented landscape. What is clear, however, is that the struggle between competition and interdependence will define the architecture of global economic governance in the 21st century.

Bibliography

Arslanalp, S., Eichengreen, B. & Simpson-Bell, C. (2024) Dollar Dominance in the International Reserve System: An Update, International Monetary Fund Blog [online]. Available at: https://www.imf.org/en/Blogs/Articles/2024/06/11/dollar-dominance-in-the-international-reserve-system-an-update.

Baldwin, R. (2019) The Great Convergence: Information Technology and the New Globalization, Harvard University Press.

Bogage, J. & Davies, E.. (2025) Ruling on Trump’s Tariffs is a major setback for the White House, The Washington Post [online]. Available at: https://www.washingtonpost.com/politics/2025/08/30/trump-tariff-policy-in-jeopardy/.

Booker, S., Conner, A. & Wessel, D. (2024) Why do the US and its allies want to seize Russian reserves to aid Ukraine?, Brookings Institution [online]. Available at: https://www.brookings.edu/articles/why-do-the-u-s-and-its-allies-want-to-seize-russian-reserves-to-aid-ukraine.

Bordo, M. D. & Eichengreen, B. (1993) A Retrospective on the Bretton Woods System: Lessons for International Monetary Reform, University of Chicago Press.

Bown, C.P. & Irwin, D.A. (2018) Trump’s Assault on the Global Trading System, Foreign Affairs [online]. Available at: https://www.foreignaffairs.com/china/trumps-assault-global-trading-system-tariff.

Bown, C.P. (2019) US–China Trade War Tariffs: An Up-to-Date Chart, Peterson Institute for International Economics [online]. Available at: https://www.piie.com/research/piie-charts/2019/us-china-trade-war-tariffs-date-chart.

Bradsher, K. (2025) China Halts Critical Exports as Trade War Intensifies, The New York Times [online]. Available at: https://www.nytimes.com/2025/04/13/business/china-rare-earths-exports.html.

Canterbury Consulting (2025) The Reign of the U.S. Dollar: Exploring Its Past, Present, and Future, Canterbury Consulting, white paper. Available at: https://www.canterburyconsulting.com/insights/the-reign-of-the-us-dollar-exploring-its-past-present-and-future.

Congress (2022) U.S. Restrictions on Huawei Technologies: National Security, Foreign Policy, and Economic Interests, Congress Reports, R47012 [online]. Available at: https://www.congress.gov/crs-product/R47012.

Conner, A. & Wessel, D. (2025) What is the status of Russia’s frozen sovereign assets? Brookings Institute [online]. Available at: https://www.brookings.edu/articles/what-is-the-status-of-russias-frozen-sovereign-assets.

Council of the European Union (2023) Impact of sanctions on the Russian economy, European Council [online]. Available at: https://www.consilium.europa.eu/en/infographics/impact-sanctions-russian-economy.

Council on Foreign Relations (2025) The Contentious U.S.–China Trade Relationship, CFR [online]. Available at: https://www.cfr.org/backgrounder/contentious-us-china-trade-relationship.

Eichengreen, B. (2011) Exorbitant Privilege: The Rise and Fall of the Dollar and the Future of the International Monetary System, Oxford University Press.

Farrell, H. & Newman, A. (2019) Weaponized Interdependence, International Security, 44(1), pp. 42–79.

Gopinath, G. (2024) Geopolitics and its impact on global trade and the dollar, International Monetary Fund [Speech]. Available at: https://www.imf.org/en/News/Articles/2024/05/07/sp-geopolitics-impact-global-trade-and-dollar-gita-gopinath.

Hofman, B. & Petry, J. (2025) Internationalization of the RMB: Status, Options and Risks, CKN. Available at: https://www.chinakennisnetwerk.nl/sites/ckn/files/2025-04/CKN%20Report%20Internationalization%20of%20the%20RMB.pdf.

Huang, Y. (2017) Capitalism with Chinese Characteristics: Entrepreneurship and the State, Cambridge University Press.

Izaza, J.C. & Flores, M. (2025) Foreign Direct Investment in Mexico Breaks Record Amid Global Economic Headwinds, Perez Correa Gonzale [online]. Available at: https://pcga.mx/en/ideas/foreign-direct-investment-mexico/.

Lagarde, C. (2016) IMF Launches New SDR Basket Including Chinese Renminbi, Determines New Currency Amounts, International Monetary Fund [Speech]. Available at: https://www.imf.org/en/News/Articles/2016/09/30/AM16-PR16440-IMF-Launches-New-SDR-Basket-Including-Chinese-Renminbi.

International Monetary Fund (2023) IMF Data Portal, IMF [online]. Available at: https://data.imf.org/?sk=E6A5F467-C14B-4AA8-9F6D-5A09EC4E62A4.

Junck, R.D., Seve, M., vom Kolke, M.A. et al. (2025) EU Targets Russia’s Energy, Financial and Defense Sectors in 18th Sanctions Package, Skadden [online]. Available at: https://www.skadden.com/insights/publications/2025/07/eu-targets-russias-energy-financial-and-defense.

Kennedy, S. (2018) Made in China 2025, Center for Strategic and International Studies [online]. Available at: https://www.csis.org/analysis/made-china-2025.

Kissinger, H. (2011) On China, Penguin Random House.

Krugman, P. (2019) Trump Is Losing His Trade Wars, The New York Times [online]. Available at: https://www.nytimes.com/2019/07/04/opinion/trump-trade-wars.html.

McBride, J., Berman, N. & Chatzky, A. (2023) China’s Massive Belt and Road Initiative, Council on Foreign Relations [online]. Available at: https://www.cfr.org/backgrounder/chinas-massive-belt-and-road-initiative.

Monteiro, N.P. (2021) The Return of Bipolarity in World Politics: China, the United States, and Geostructural Realism, Columbia University Press.

Naughton, B. (2018) The State Strikes Back: The End of Economic Reform in China?, Peterson Institute for International Economics.

Organization for Economic Co-operation and Development (2025) OECD Supply Chain Resilience Review, OECD [online]. Available at: https://www.oecd.org/en/publications/2025/06/oecd-supply-chain-resilience-review_9930d256.html.

Office of the United States Trade Representative (2018) Update Concerning China’s Acts, Policies and Practices Related to Technology Transfer, Intellectual Property, and Innovation, Executive Office of the United States of America [online]. Available at: https://ustr.gov/sites/default/files/enforcement/301Investigations/301%20Report%20Update.pdf.

Office of the United States Trade Representative (2020) Section 301 Investigations: Tariff Actions, USTR [online]. Available at: https://ustr.gov/issue-areas/enforcement/section-301-investigations/tariff-actions.

Prescott, F.C., Fine, H.A. & Cassidy, V.H. (eds) (1949) Foreign Relations of the United States, 1949, The Far East: China, Volume IX, U.S. Office of the Historian.

Silver, L., Huang, C. & Clancy, L. (2023) China’s Approach to Foreign Policy Gets Largely Negative Reviews in 24-Country Survey, Pew Research Center [online]. Available at: https://www.pewresearch.org/global/2023/07/27/views-of-china/.

Rodrik, D. (2017) Straight Talk on Trade: Ideas for a Sane World Economy, Princeton University Press.

Rudd, K. (2022) The Avoidable War: The Dangers of a Catastrophic Conflict between the US and Xi Jinping’s China, Hachette Book Group.

Shambaugh, D. (2020) Where Great Powers Meet: America and China in Southeast Asia, Oxford University Press.

Standard Chartered (2025) Global Market Outlook, Standard Chartered [online]. Available at: https://www.sc.com/je/market-outlook/global-market-outlook-20-6-2025/.

Sutter, K.M. (2024) Made in China 2025 and Industrial Policies, Congress (IF10964). Available at: https://www.congress.gov/crs-product/IF10964.

Toussaint, E. (2024) Domination of the United States on the World Bank, Committee for the Abolition of Illegitimate Debt [online]. Available at: https://www.cadtm.org/Domination-of-the-United-States-on-the-World-Bank.

United States, Executive Office of the President (2025) Regulating Imports with a Reciprocal Tariff to Rectify Trade Practices that Contribute to Large and Persistent Annual United States Goods Trade Deficits, Washington, D.C.: Executive Office of the President of the United States [online]. Available at: https://www.whitehouse.gov/presidential-actions/2025/04/regulating-imports-with-a-reciprocal-tariff-to-rectify-trade-practices-that-contribute-to-large-and-persistent-annual-united-states-goods-trade-deficits/.

United States. Executive Office of the President (2025) Further Modifying Reciprocal Tariff Rates to Reflect Ongoing Discussions With the People’s Republic of China, Washington, D.C.: Executive Office of the President of the United States [online]. Available at: https://www.whitehouse.gov/presidential-actions/2025/08/further-modifying-reciprocal-tariff-rates-to-reflect-ongoing-discussions-with-the-peoples-republic-of-china/.

United States Congress (2022) H.R.4346 – CHIPS and Science Act, Congress [online]. Available at: https://www.congress.gov/bill/117th-congress/house-bill/4346.

United Nations Trade and Development (2025) Global foreign direct investment falls for the second consecutive year, posing acute challenges to developing countries, UN Trade and Development [online]. Available at: https://unctad.org/news/global-foreign-direct-investment-falls-second-consecutive-year-posing-acute-challenges.

Von Beschwitz, B. (2024) Internationalization of the Chinese renminbi: progress and outlook, FEDS Notes [online]. Available at: https://www.federalreserve.gov/econres/notes/feds-notes/internationalization-of-the-chinese-renminbi-progress-and-outlook-20240830.html.

World Trade Organization (2019) DS543: United States — Tariff Measures on Certain Goods from China, WTO [online]. Available at: https://www.wto.org/english/tratop_e/dispu_e/cases_e/ds543_e.htm.

World Trade Organization (2020) WTO Panel Report on US–China Tariffs, WTO [online]. Available at: https://www.wto.org/english/news_e/news20_e/dsb_27jan20_e.htm.

World Trade Organization (2025) Tariffs, WTO [online]. Available at: https://www.wto.org/english/tratop_e/tariffs_e/tariffs_e.htm.

World Bank Group (2022) Infrastructure Finance, World Bank Group [online]. Available at: https://www.worldbank.org/en/topic/financialsector/brief/infrastructure-finance.

Xi, J. (2017) Report to the 19th National Congress of the Communist Party of China, Xinhua [online]. Available at: http://www.xinhuanet.com/english/download/Xi_Jinping’s_report_at_19th_CPC_National_Congress.pdf.

Xing, Y. (2021) China and the Semiconductor Industry, Asian Economic Policy Review, 21(3), pp.55–79.

Yergin, D. (2020) The New Map: Energy, Climate, and the Clash of Nations, Penguin Random House.

Zhang, C. (2020) China and Global Supply Chains in the Era of COVID-19, Journal of Chinese Political Science, 25(3), pp.1–19.

Zhang, W. (2017) China, the WTO, and the Global Trading System, Cambridge University Press.

{kind=link}